The market used to think of IKIO as “the Philips lighting guys.” If you’re still holding that outdated view, you’re reading the wrong balance sheet. The latest Q4 FY26 numbers just dropped, and they aren’t just a result; they are a declaration of war on the “single-client” stigma. While the legacy home lighting business is being treated like a secondary vertical, the “Other Business” segment—refrigeration lighting, RV solutions, and the high-octane hearables/wearables space—has grown into a monster that now commands 71% of total quarterly revenue.

The most violent move on the P&L isn’t the 47% jump in revenue; it’s the Net Profit, which rocketed from a measly loss of ₹0.7 crore in the same quarter last year to a sturdy ₹17.5 crore. This is operating leverage in its purest, most aggressive form. The company’s heavy front-ended investments in its new Noida facility (Block I) are finally starting to sweat, and with Block II commissioning targeted for Q1 FY27, the management is effectively doubling down on its bet that India can beat China at the high-end EMS game.

1. At a Glance – The Rebirth of an EMS Giant

IKIO Technologies is currently undergoing a structural transformation that most companies only dream of. They have successfully pivoted from being a captive manufacturer for a single global lighting giant into a diversified electronics powerhouse.

In FY26, the company clocked ₹595 crore in sales, a 23% growth that hides the real story inside the segments. The legacy home lighting business is actually shrinking in terms of contribution, while the “Other” segment grew at a blistering 72% YoY in Q4 alone. This isn’t just luck; it’s a calculated move into higher-margin, specialized electronics like IPS controllers for commercial refrigeration and ABS pipes for Recreational Vehicles (RVs) in the US.

The narrative for the next 12 months is simple: Capacity vs. Utilization. They’ve built the “Taj Mahal” of manufacturing in Noida with over 5 lakh sq. ft. of space. Block I is already humming. Block II, which will house the high-growth hearables and wearables division (think earbuds and smartwatches for top-tier brands), is slated to go live by June 2026.

If they can fill this capacity as fast as they claim—management expects 60% utilization on Day 1 for hearables—the current P/E of 34.8 might actually start looking cheap. The company is debt-light, promoter-heavy, and sitting on a pile of growth triggers that include a 4.5% PLI benefit kicking in next year. This is no longer a “lighting” stock; it’s a high-precision technology play.

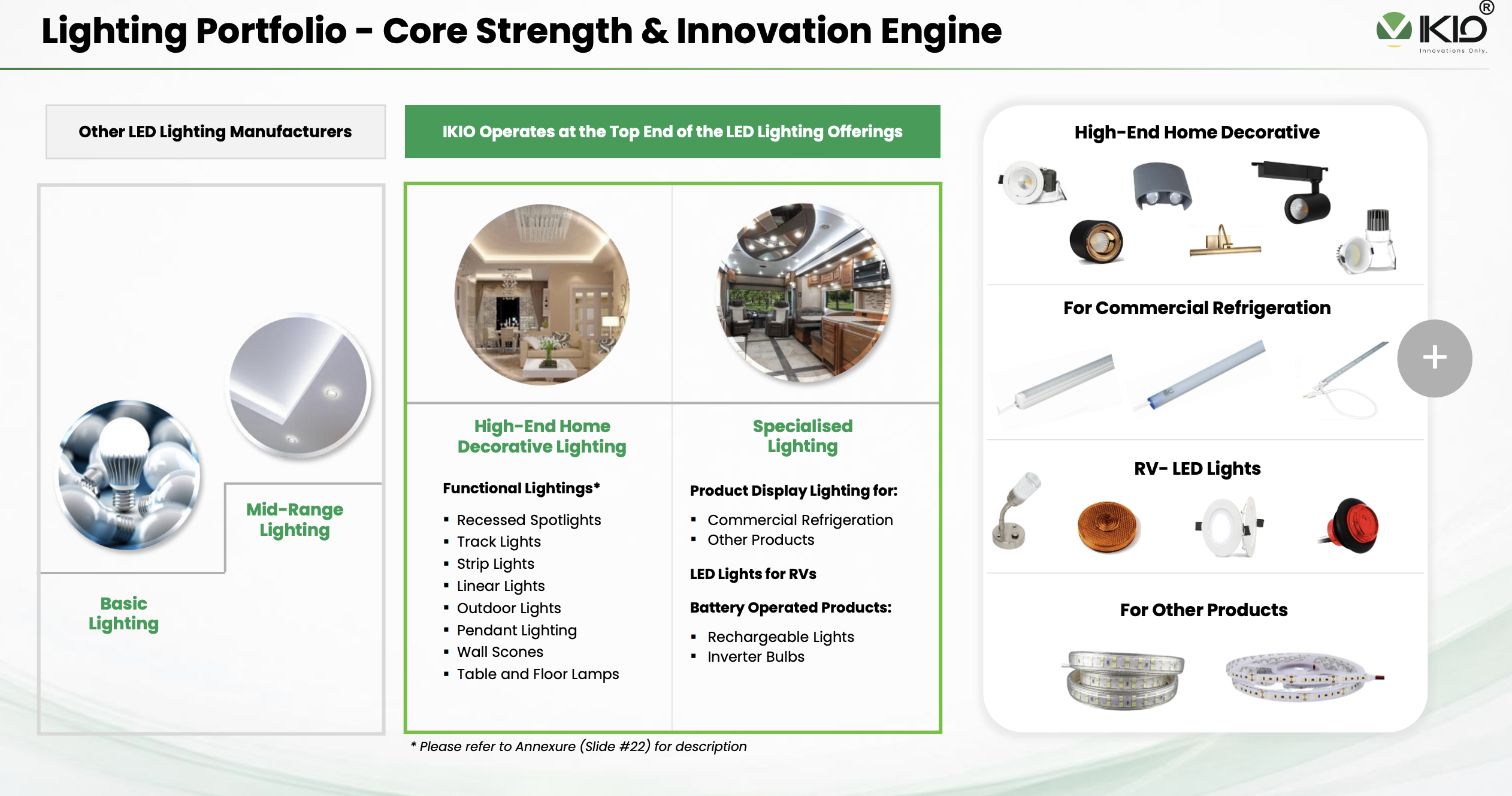

2. Introduction: Breaking the Shackles of the Past

For years, the bear case against IKIO was “Customer Concentration.” If Signify (Philips) sneezed, IKIO caught pneumonia. But look at the H1 FY26 split: 70% of revenue now comes from diversified segments. They have successfully onboarded brands like Panasonic, Honeywell, and Novateur, reducing the “Philips dependency” to a manageable level.

The company operates as an Original Design Manufacturer (ODM). This is a crucial distinction. They don’t just “assemble” stuff like a low-rent workshop; they design the circuitry, the thermal management, and the aesthetics. This “Design-First” approach allows them to command gross margins of 40-45%, a rarity in the cut-throat EMS world where 10-15% is the norm.

Geographically, they are playing a smart game of musical chairs. When US tariffs made exports tricky, they pivoted to the Middle East. Revenue from outside India grew 53% YoY in FY26, proving that their quality is accepted in global markets. They aren’t just selling