1. At a Glance – The 50-Year-Old Electrician That Just Switched to Turbo Mode ⚡

Power & Instrumentation (Gujarat) Ltd (PIGL) is currently priced at ₹104, sitting with a modest market cap of ₹201 Cr. The stock has been punished hard — down 31.5% in 3 months and 43.9% in 1 year. Ouch.

But here’s the plot twist.

Q3 FY26 consolidated revenue jumped to ₹48.89 Cr (+43% YoY) and net profit came in at ₹3.57 Cr, while the company secured ₹124.17 Cr worth of fresh orders in the quarter alone. That’s more than half its annual revenue pipeline in just 90 days.

Current P/E stands at 14.8, compared to industry PE of 24.9.

ROCE: 19.8%.

ROE: 14.5%.

Debt-to-equity: 0.18 — not scary.

Order book (ongoing works): ₹450+ Cr.

So here’s the real question:

Is the market ignoring a 50-year-old EPC veteran entering 400kV and busduct segments… or is this just another small-cap EPC stock that looks great in presentations?

Let’s open the toolbox.

2. Introduction – The Electrician Who Electrified Airports Before It Was Cool

Founded in 1975, PIGL has survived five decades in India’s infrastructure circus. That alone deserves a medal.

They started as a proprietary firm, became private, then listed on NSE Emerge in 2018, and migrated to the main board in 2023. That migration is like moving from local train to Vande Bharat — expectations automatically increase.

This is not a random contractor installing ceiling fans.

They have:

- Completed 35+ airport projects

- Electrified 100,000+ BPL households

- Laid 20,000+ km of HT & LT lines

- Entered the 400 kV Extra High Voltage segment in 2025

Now that’s serious electrical muscle.

In Q3 FY26, management highlighted disciplined execution and improving operational efficiency. Revenue visibility looks strong thanks to large RDSS electrification contracts and industrial projects.

But let’s not get carried away by PowerPoint slides.

EPC companies are famous for one thing — impressive order books and thin margins.

So the question becomes:

Can PIGL convert its ₹450+ Cr ongoing work into consistent cash flows without burning working capital?

Because in EPC, revenue is theory. Cash is reality.

3. Business Model – WTF Do They Even Do?

Think of PIGL as the “power wiring backbone” of infrastructure projects.

They provide EPC (Engineering, Procurement & Construction) solutions in electrical contracting. That includes:

- 132-11 KV indoor & outdoor substations

- Transformers & power distribution panels

- Diesel generator sets

- UPS systems

- Specialized lighting

- Building management systems

- Electrification of airports, hospitals, telecom infra

Their revenue mix (FY23):

- Sale of Products: 83%

- Sale of Services: 17%

So largely execution-driven.

Clients include heavyweights like:

- ISRO

- ONGC

- SEBI

- Vodafone

- Ford

- Airport Authority of India

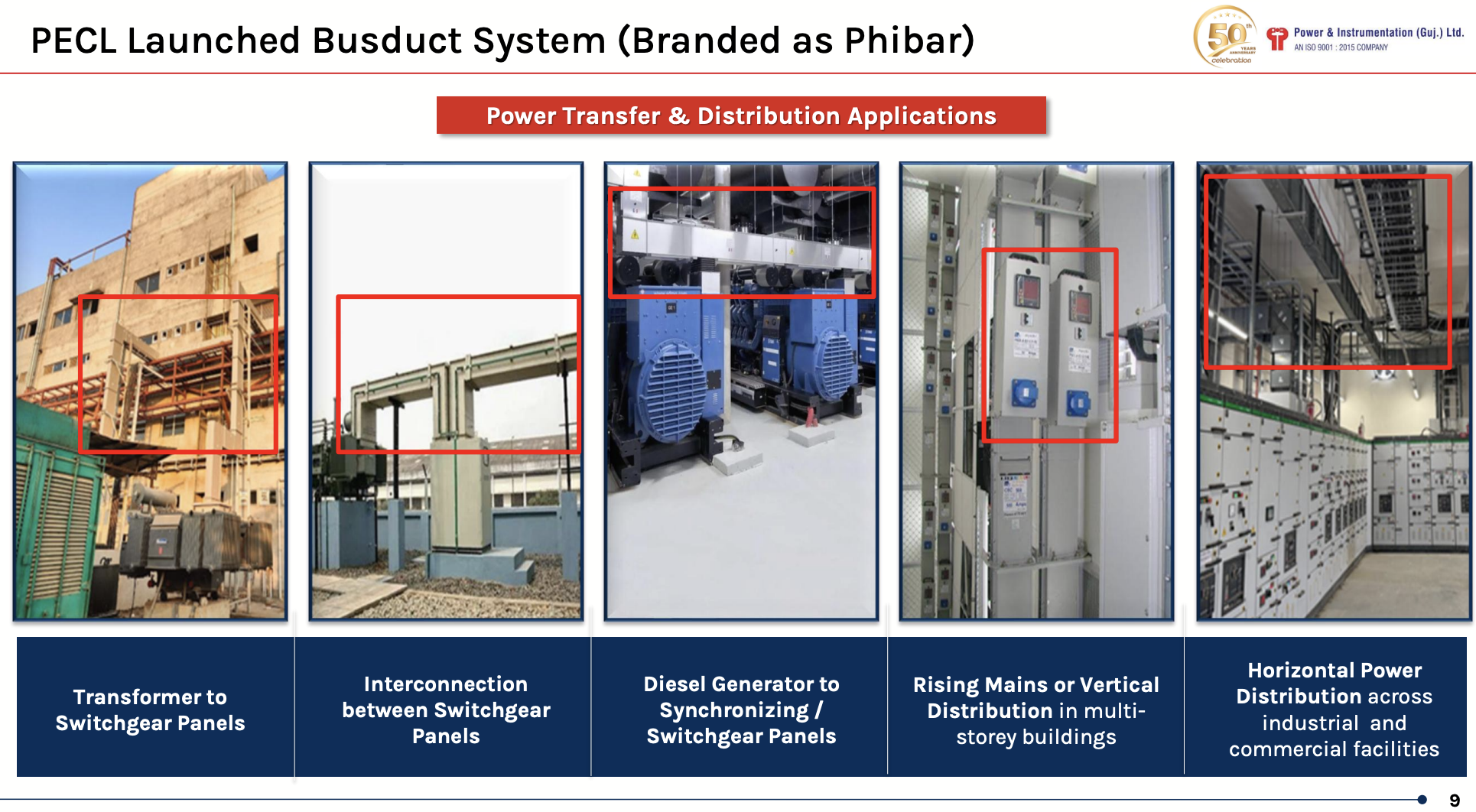

They’ve recently acquired 51.06% stake in PECL, entering the busduct system segment (branded “Phibar”). Busducts are modern alternatives to heavy cabling — compact, scalable, efficient.

Now here’s the detective question:

Is this diversification into busduct manufacturing going to expand margins… or dilute focus?

Because contracting is low-margin. Manufacturing can improve profitability — if executed well.

The next few years will reveal whether PECL becomes a margin booster or just another subsidiary absorbing capital.

4. Financials Overview – Numbers Don’t Lie, But They Do Whisper

Result Type Detected: Quarterly Results (Q3 FY26)

So we annualise using Q3 logic:

Annualised EPS = Average of