1. At a Glance – The One-Paragraph Roast That Hurts a Little

₹74.7 crore market cap. ₹21.2 stock price. A business that claims to sell spiritual books but actually juggles movies, animated mythology, song albums, TV serials, radio shows, and even FMCG under the brand Krishna Sai. If confusion were an asset class, Orient Tradelink would be large-cap. The latest quarter (Sep 2025) clocked ₹2.95 crore in sales and ₹0.39 crore in profit, yet the stock trades at a face-melting 356x P/E. Return over 3 months is +10.1%, return over 1 year is -38.8%, and promoter holding has shrunk to a symbolic 0.25%—basically a cameo appearance. ROCE at 7.42% politely exists, OPM at -3.78% sulks in the corner, and other income casually props up profits like that one friend who always pays the bill. This is not a boring company. This is a spiritually confused, financially adventurous one. Curious already? Good. You should be.

2. Introduction – Once Upon a Balance Sheet

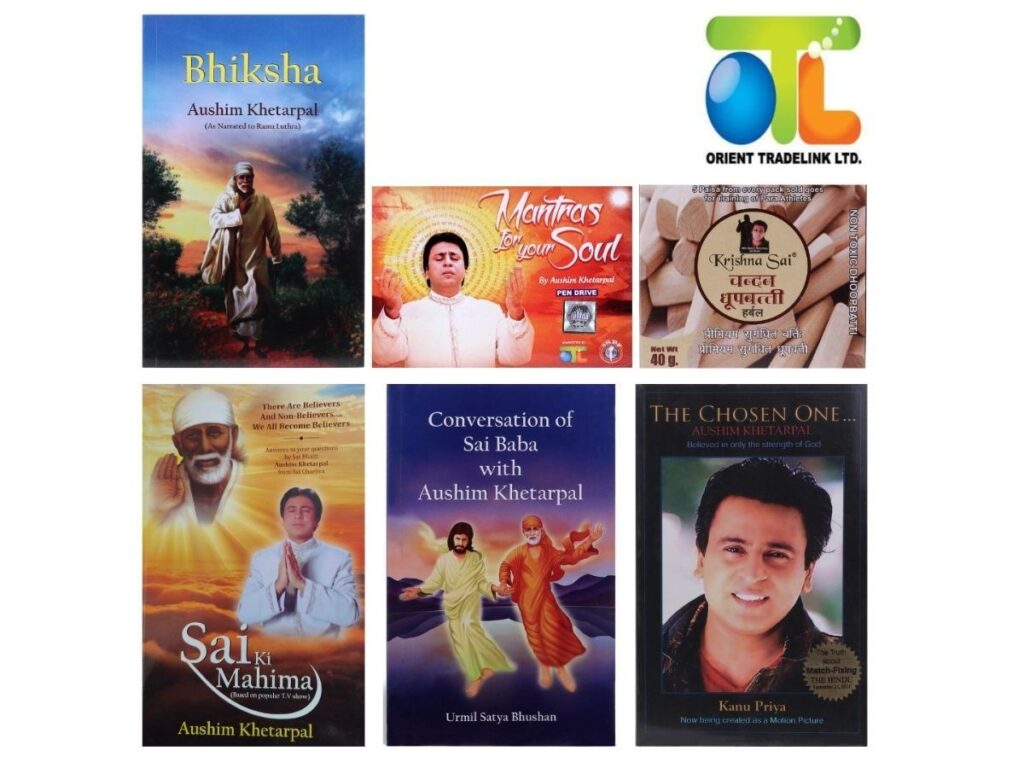

Orient Tradelink Ltd was incorporated in 1994, back when “content” meant cassette tapes and Doordarshan. Officially, it sells spiritual books. Unofficially, it behaves like a content buffet—movies, animated movies, television serials, song albums, radio shows, audio-visual rights, mythology mantras, FMCG products, and the occasional corporate action that keeps auditors awake at night.

This is one of those companies where reading the business description feels like scrolling Netflix categories at 2 a.m. You don’t know what you’re watching, but something keeps you hooked. The firm has offline and online sales rights for audio-visual inventory in the mantra and mythology genre. Think devotional meets distribution meets “let’s also try FMCG, why not?”

Financially, the company is small, volatile, and dramatic. Quarterly numbers swing like a mythological pendulum—profits appear, disappear, reappear, and occasionally go negative, all while the stock market assigns it a valuation that suggests divine intervention.

So the big question: is this a misunderstood micro-media house with optionality, or a financial soap opera with too many episodes and no clear season finale? Let’s open the scriptures—also known as the financial statements—and find out.

3. Business Model – WTF Do They Even Do?

Explaining Orient Tradelink’s business model to a lazy but smart investor is like explaining Indian mythology to someone who’s only watched Marvel movies.

At its core, the company deals in content creation, production, and marketing—movies, animated films, TV serials, song albums, and radio shows. The dominant theme? Mantras, mythology, and spiritual narratives. This content is monetised through sales, licensing, and marketing rights, both online and offline.

Then comes the plot twist: FMCG. Under the brand Krishna Sai, the company runs a fast-moving consumer goods business. What exactly is sold isn’t elaborated in financial detail, but the intent is clear—diversify revenue streams beyond pure content.

Revenue concentration is heavy. In FY22, about 90% of revenue came from sale of products, with the remaining ~10% from other income. Translation: operating business exists, but other income still plays a suspiciously important supporting role.

The company has also been actively signing content and publishing deals, including:

A six-book publishing deal with Story Mirror Infotech Pvt Ltd (September 2022).

An 11-year music and digital deal with Time Audio and Music Companies of Bollywood (May 2022).

So the model is not fake. It’s just… scattered. Content, devotion, FMCG, publishing, music, warrants, preferential allotments—Orient Tradelink doesn’t believe in putting all its eggs in one basket. It believes in buying every basket in the market.

Does this diversification create optionality or operational chaos? Hold that thought.

Result Type Lock: The latest official heading is Quarterly Results, so EPS is treated as quarterly and annualised by multiplying by four.

Quarterly Performance Table (₹ crore)

Metric

Latest Qtr (Sep 2025)

Same Qtr LY (Sep 2024)

Prev Qtr (Jun 2025)

YoY %

QoQ %

Revenue

2.95

3.07

4.79

-3.91%

-38.41%

EBITDA (Operating Profit)

-0.68

1.08

0.78

-162.96%

-187.18%

PAT

0.39

0.54

0.46

-27.78%

-15.22%

EPS (₹)

0.20

0.22

0.29

-9.09%

-31.03%

Annualised EPS: ₹0.20 × 4 = ₹0.80

Witty commentary time. Revenue dipped both YoY and QoQ, EBITDA turned negative like a villain arc, and PAT survived mainly because depreciation and other income did their magic. This is not a smooth compounding story; it’s more like quarterly cliff-jumping with a parachute stitched from “Other Income”.

Question for you: would you trust a company where profits exist but operating profit plays hide-and-seek?

5. Valuation Discussion – When Numbers Start Praying

Method 1: P/E Valuation

Annualised EPS: ₹0.80

Current Price: ₹21.2

Implied P/E: ~26.5x (market actually prices trailing earnings much higher)

Using a conservative multiple range of 15x–25x for small media companies:

Fair value range: ₹12 – ₹20

Method 2: EV / EBITDA

EV: ₹79.4 crore

TTM EBITDA: Negative (-₹0.60 crore)

Result: This method refuses to cooperate. EV/EBITDA is