3i Infotech Q3 FY26: ₹172 Cr Revenue, ₹2.1 Cr PAT, 4.9x P/E — Turnaround Tech or Value Trap in Disguise?

1. At a Glance – The Comeback Kid With Court Cases

3i Infotech is currently trading at ₹13.9 with a market cap of ₹289 crore. The stock is down 17.9% in 3 months and 38% in one year — investors clearly didn’t send Diwali sweets.

Yet here’s the plot twist.

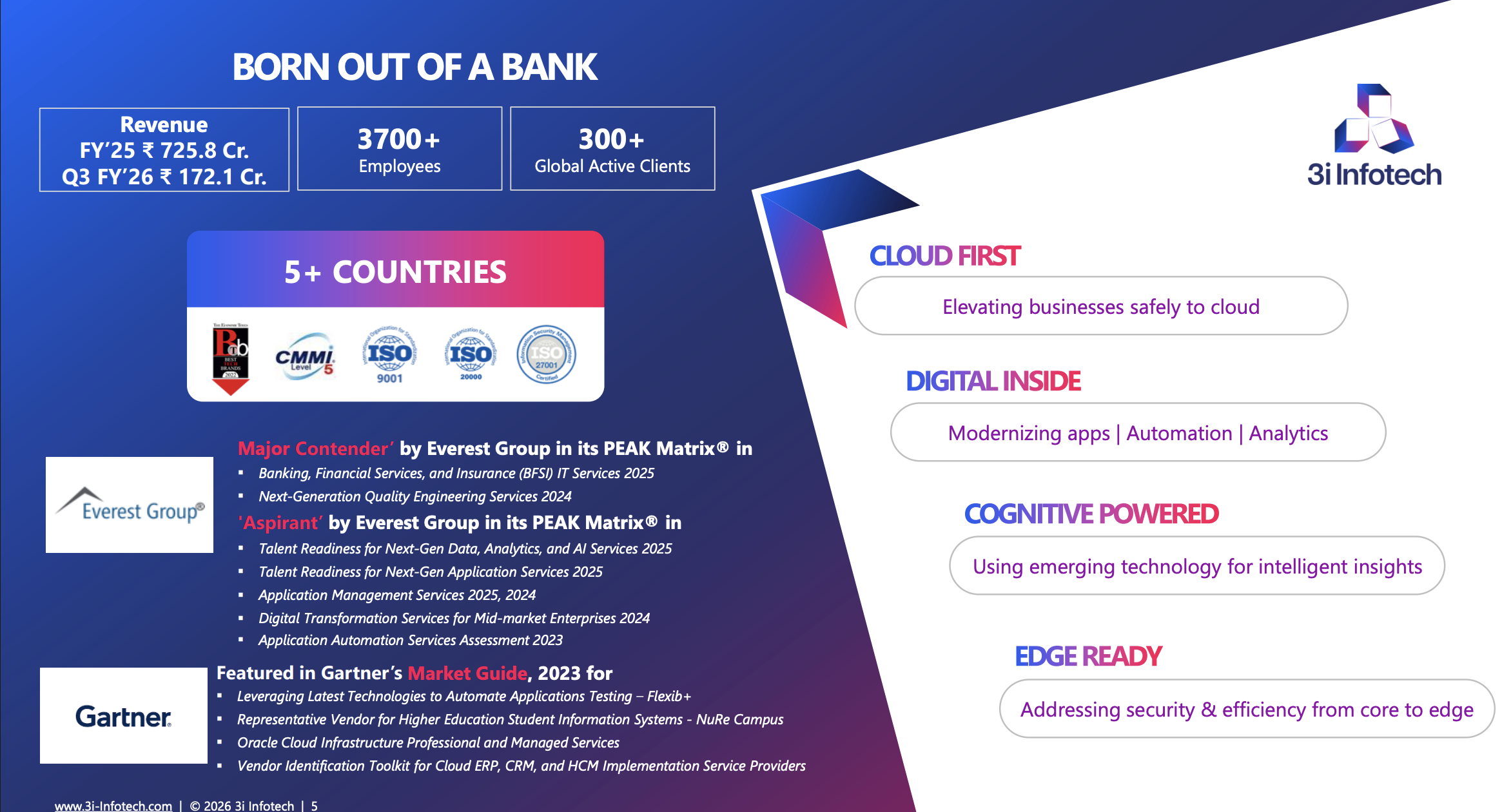

Q3 FY26 revenue came in at ₹172.1 crore, EBITDA at ₹11.4 crore, and PAT at ₹2.1 crore (after ₹3.4 crore exceptional impact). Annualised EPS based on Q3 (average of Q1, Q2, Q3 × 4 rule applied) comes to ₹1.81.

At current price, P/E works out to roughly 7.7x on annualised earnings. Screener shows 4.94x based on trailing numbers.

Debt is down to ₹35 crore. Price-to-book is 0.89. ROE stands at 8.28%.

And then… there’s a ₹128 crore fraud complaint, arbitration with RailTel, auditor qualification on receivables, and a rights issue of ₹64.1 crore.

So what is this company?

A digital transformation specialist? A restructuring survivor? Or a Netflix crime documentary in progress?

Let’s investigate.

2. Introduction – Born From a Bank, Raised in Chaos

3i Infotech was born out of ICICI Bank in 1993. It IPO’d in 2005. It did global acquisitions. It crossed ₹1,000 crore revenue.

Then debt restructuring happened. Then business sale happened. Then rights issue happened.

If corporate life had a rollercoaster emoji, this would be it.

In FY23, the company sold its software products business and retained services. So today’s 3i Infotech is a services-focused IT company operating across AAA (Application–Automation–Analytics), Infrastructure Services, and Digital BPS.

But this isn’t your typical TCS-style compounding machine.