1. At a Glance

V-Guard Industries is currently a massive contradiction in the Indian consumer durable space. On one hand, you have a legacy brand that essentially taught India why they need a voltage stabilizer; on the other, you have a management team desperately trying to pivot into a pan-India lifestyle brand through the high-stakes acquisition of Sunflame. The latest numbers for Q4 FY26 tell a tale of aggressive revenue recovery—up 14.1% YoY to ₹1,755 crore—but the underlying stress is palpable.

The company is walking a tightrope between top-line expansion and margin preservation. While the Consolidated PAT for the quarter jumped 23% to ₹112 crore, the full-year picture is far more sobering. FY26 was a year of “seasonal vagaries,” a polite corporate term for “a weak summer killed our cooling sales.” If you look closely, the Consolidated PAT for the full year actually dipped by 1.7% to ₹308 crore.

Wait, it gets messier. There was a one-time exceptional hit of ₹22.11 crore related to new labor codes for gratuity and leave encashment. Without this, the growth would have looked slightly more respectable, but the “Exceptional” tag doesn’t hide the fact that core profitability is under siege by commodity inflation. Copper, the lifeline of their electricals business, has been a nightmare, with management admitting to a 40% price surge in a single year.

Investors are watching a classic south-to-north migration. For the first time, non-South markets are breathing down the neck of their home turf, contributing 46.3% of Q4 revenues. However, this expansion comes at a cost—marketing spends, aggressive pricing to fight established North Indian players, and the friction of integrating Sunflame’s kitchen business, which saw a 9.9% revenue decline in the December quarter before showing a faint pulse in Q4.

Are they a tech-forward electrical giant or a legacy firm trying to buy its way into relevance? The Kochi Innovation Campus and the new ₹50 crore battery plant in Hyderabad suggest they want to be the former, but the heavy dependence on summer intensity remains their Achilles’ heel.

2. Introduction

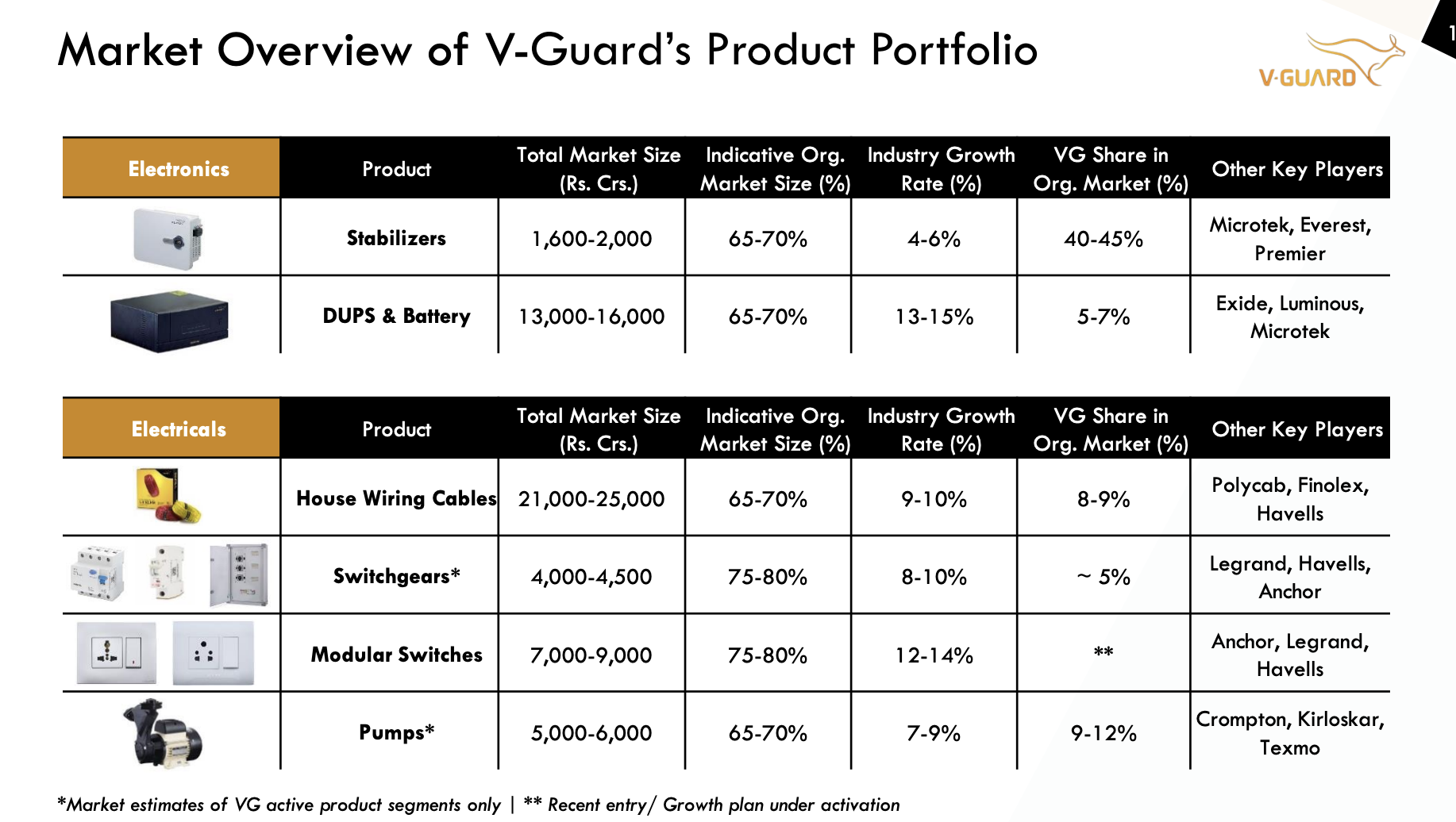

V-Guard is no longer just “the stabilizer company.” From its humble roots in 1977 Kochi, it has metastasized into a multi-product behemoth. It now operates across three main silos: Electronics, Electricals, and Consumer Durables.

The strategy is simple but dangerous: move from being a seasonal player (stabilizers/coolers) to a perennial one (wires/kitchen appliances). The acquisition of Sunflame was meant to be the masterstroke for the “Non-South” expansion. But as the FY26 data shows, integration is rarely a smooth ride.

The company is currently battling two fronts. First, the internal struggle to shift manufacturing in-house (currently at 65%, targeting 75%) to protect margins. Second, the external battle against a “violent” commodity market. Management’s refusal to “chase volumes” at the cost of profitability is a bold stance, but in a price-sensitive market like India, that’s a risky game of chicken with competitors.

3. Business Model – WTF Do They Even Do?

Think of V-Guard as the “Insurance Policy” of the Indian household. They started by protecting your TV and Fridge from the erratic Indian power grid. Now, they want to own the wires inside your walls, the fan on your ceiling, and