Rossell Techsys (ROSSTECH) has effectively ceased being a “demerged story” and has transformed into a high-velocity execution machine. The FY26 numbers aren’t just an improvement; they represent a structural reset of the company’s operating scale. With Revenue hitting ₹485 Crore (up from ₹259 Crore) and Profit Before Tax surging to ₹28.47 Crore (up from ₹10.71 Crore), the company has officially entered its “scale inflection” phase.

1. At a Glance – The Dangerous Speed of Growth

Rossell Techsys is currently playing a high-stakes game in the Aerospace, Defense, and Semiconductor verticals. While the headline numbers look spectacular, a deeper dive into the balance sheet reveals a company sprinting so fast it is burning through cash to keep the engine running.

The most provocative number isn’t the 87% Revenue growth; it’s the inventory pile-up and the debt required to fund it. The company is sitting on ₹313 Crore of inventory to support a ₹485 Crore sales run rate. That is massive. They are essentially pre-buying their future growth, betting heavily on their strategic agreements worth ₹3,000 Crore.

Management has pivoted from “Build-to-Print” to “Scale-at-all-costs.” They’ve just locked in a 2.1 Lakh sq. ft. facility expansion via lease because they are literally running out of floor space to execute orders. This is a classic “good problem” that carries the risk of “bad execution” if the global supply chain hiccups.

The Red Flags you can’t ignore:

- Borrowings have jumped to ₹409 Crore (from ₹240 Crore in FY25).

- Cash Flow from Operations is deep in the red at -₹83 Crore.

- Inventory Days are 380, which, while improving, still means cash is locked in boxes on shelves for over a year.

Investors are currently paying a P/E of 149x. This is priced for perfection. Any delay in the semiconductor ramp or a slowdown in Boeing’s shipsets could lead to a painful re-rating. Is the management’s “Production Maturity” story strong enough to justify this valuation?

2. Introduction

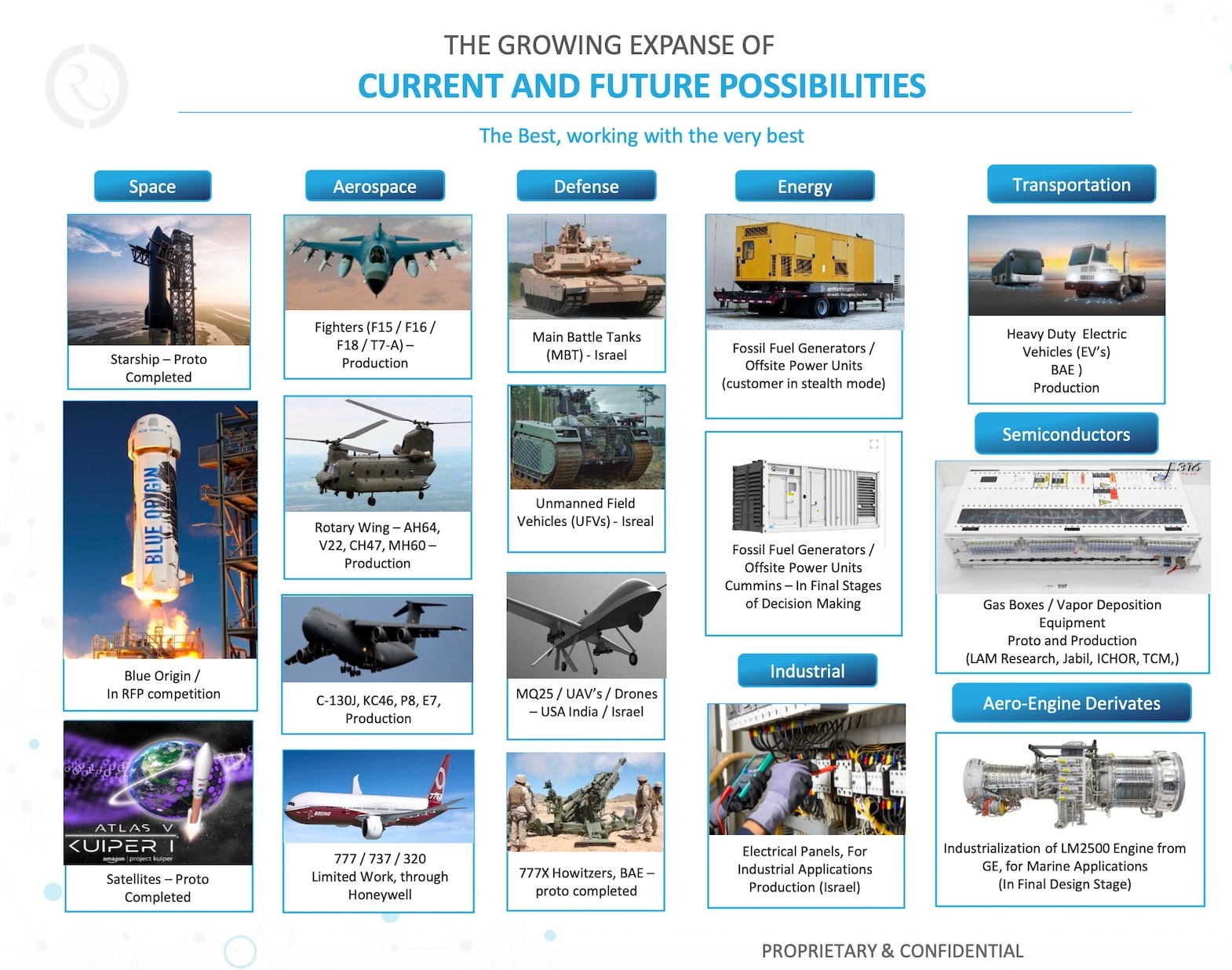

Rossell Techsys Ltd (RTL) is no longer the “small aerospace division” of Rossell India. Since its listing in FY24, it has aggressively repositioned itself as a key supplier to global Tier-1 OEMs like Boeing, Lockheed Martin, and Honeywell.

The company specializes in Electrical Wiring and Interconnect Systems (EWIS) and Electrical Panel Assemblies (EPA). Basically, they provide the “nervous system” for fighter jets, helicopters, and now, semiconductor manufacturing equipment.

The story in FY26 is about diversification. Historically, Boeing was the sun around which Rossell orbited (contributing 90% of revenue in FY22). Today, that concentration is down to 40%, with the Semiconductor and Space segments scaling rapidly.

They operate out of Bangalore with a Delaware-registered C-Corp subsidiary in the USA, giving them a strategic foothold in the world’s largest defense market. The company is currently transitioning from a pure defense player to a high-tech manufacturing conglomerate.

3. Business Model – WTF Do They Even Do?

Imagine a Boeing AH-64 Apache attack helicopter. It has miles of complex wiring and hundreds of circuit panels. Rossell doesn’t build the helicopter; they build the wiring harnesses and panels that make sure the pilot’s commands actually reach the rotors and weapons.

The Segments:

- EWIS & EPA: The bread and butter. High-reliability wiring for military platforms.

- Semiconductors: The new shiny toy. They provide wire harnesses for the machines that make chips. This is a high-margin, quick-turnaround business.

- Space: Supplying harnesses for satellites.

- MRO (Maintenance, Repair, Overhaul): Fixing the stuff they (and others) made.

They operate on two models: Build-to-Print (you give us the drawing, we make it) and Build-to-Spec (you