01 — At a Glance

The Conglomerate That Dares to Do Everything Except Profit

- Q3 FY26 Revenue₹2,006 Cr

- Q3 FY26 PAT₹-161 Cr

- 9M FY26 Revenue₹5,834 Cr

- 9M FY26 Growth+12% YoY

- Current Price₹28.0

- 52-Week High / Low₹69.7 / ₹24.4

- P/E RatioN/A (Loss)

- Book Value₹7.48

- Promoter Holding74.8%

- Dividend Yield0.00%

The Opening Act: RattanIndia lost ₹162 crore in Q3 FY26 — but only ₹13 crore before notional MTM losses on investments in Rattan Power. Cocoblu e-commerce is carrying the load with ₹5,707 crore in 9M revenue (+13% YoY). Revolt Motors hit 50,000 units sold lifetime and hired Hardik Pandya as brand ambassador. And NeoSky is delivering drones to the Indian Army that can kill you while simultaneously recording it on TikTok. Everything is growing. Nothing is profitable. Classic startup arithmetic.

02 — Introduction

The Conglomerate That Exists in Beta Testing

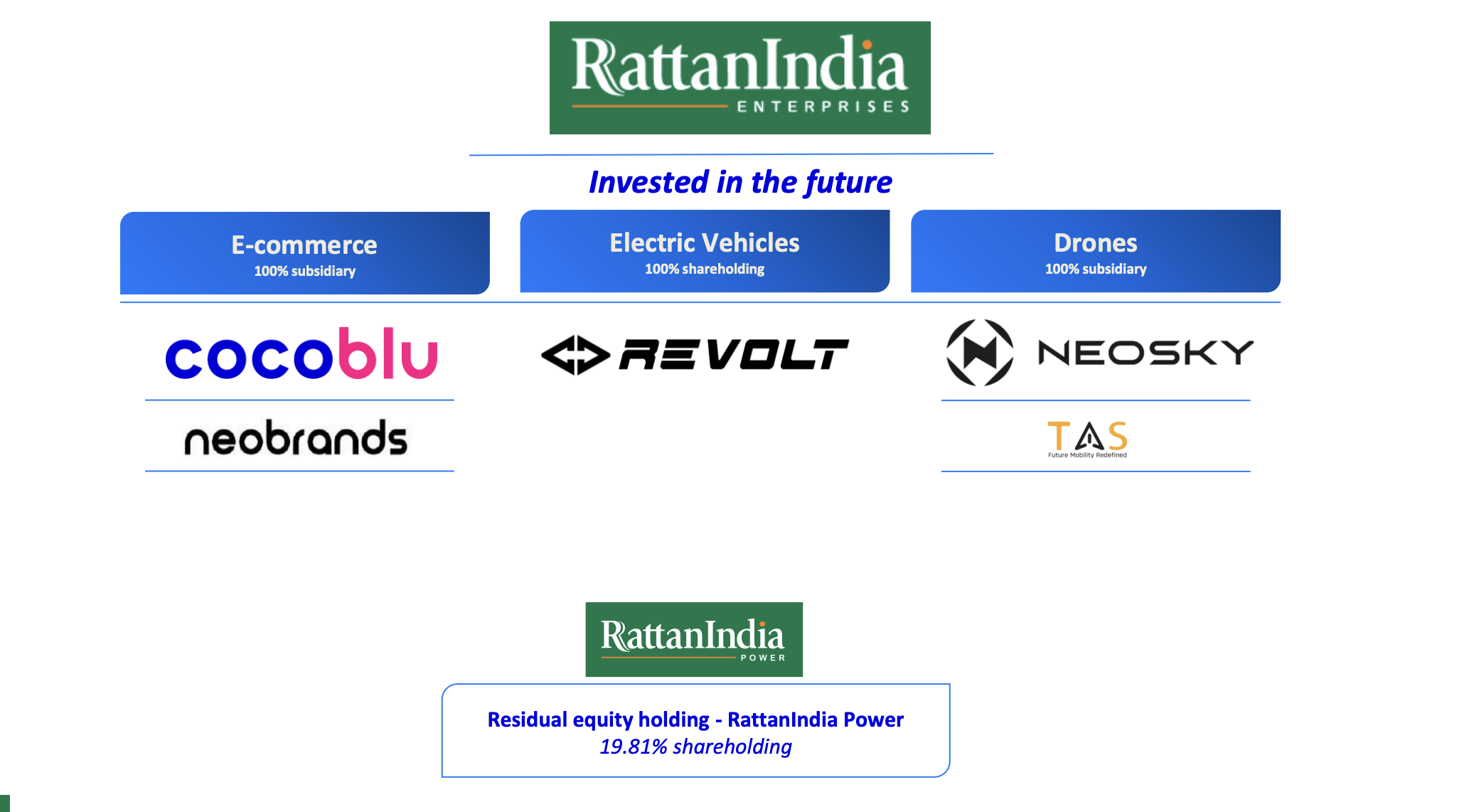

Rajiv Rattan built an empire. Not the kind that mints money. The kind that mints ideas. E-commerce? Check. Electric motorcycles? Absolutely. Drones that the Army wants? Of course. Fintech? Already done. Fashion brands nobody knew they needed? Fyltr, Kaari, Inkd, Pump’d, Neomate, Akkord, Kalaanj — one for every mood swing.

RattanIndia Enterprises is what happens when a billionaire asks: “What if we built five startups at once?” The answer: you get ₹3,876 crore market cap, 74.8% promoter holding, losses in Q3, and a strategy document that reads like a HODL investor’s fever dream.

In Q3 FY26, they lost ₹162 crore. But if you strip out the unrealised notional loss of ₹189 crore (MTM on Rattan Power shares), the core PBT was actually ₹13 crore positive. So basically, they broke even, except for a number that makes them look broke. In India, that passes as creative accounting.

The 9M FY26 revenue hit ₹5,834 crore, up 12% YoY. Cocoblu Retail alone crossed ₹5,707 crore in 9M with 4.5 orders every second (do the math: 1.5 lakh orders daily; at this rate, Cocoblu is moving faster than the Indian railways). Revolt Motors just rolled out its 50,000th motorcycle. And Hardik Pandya — yes, that Hardik Pandya — joined Revolt in Feb 2026 as brand ambassador. If star power could charge batteries, Revolt would never need an inverter again.

The Concall Confession (Feb 2026): Management described Q3 as hitting “highest ever revenue in nearly two decades for Q4 CY25” — wait, that’s Castrol’s line. RattanIndia’s story is more honest: “We’re growing, we’re burning cash, and we’re placing bets on five moonshots simultaneously. One of them will moon. Maybe.”

03 — Business Model: What Do They Actually Do?

Everything. Absolutely Everything.

RattanIndia is a holding company that operates four wildly different businesses. Imagine your uncle who dabbles in share trading, real estate, YouTube, crypto, and wellness coaching simultaneously. Except your uncle has ₹5,834 crore in annual revenue. And promoter backing. And access to venture capital.

Cocoblu Retail (E-Commerce) — The crown jewel. Started in 2021. Reached ₹5,507 crore revenue in 2 years. (For context: it took Amazon 12 years and Flipkart 10 years to reach ₹5,500 crore.) Partnered with 259 Amazon fulfilment centres, 303 dark stores, 1,500+ active vendors. Handles 4.5 orders per second. Consistent 4.7-star rating. Now expanding globally — just partnered with Noon, the Saudi Arabian e-commerce giant, to enter the Middle East. The business model: take 20-30% commission, leverage Amazon’s infrastructure, let vendors do the sourcing, and collect rent on the transaction flow.

Revolt Motors (Electric Two-Wheelers) — 100% acquired in Jan 2023. Five models: RV1, RV1+, RV BlazeX, RV400 BRZ, RV400. Price range: ₹99,999 to ₹1,39,950. 70% market share in EV motorcycles in 2025. Total Cost of Ownership vs. petrol bikes: 60% cheaper over 5 years. 219 dealerships across 197 cities by Q3 FY26 (up from 186 in 9M FY25). 50,000 units sold lifetime. Monthly running cost advantage of 50% vs. petrol. The strategy: price aggressively, dominate the EV 2W space before traditional OEMs wake up, and now hire Hardik Pandya to make sure nobody can ignore you.

NeoSky Drones (Aerospace & Defence) — Delivered optic fibre drones to the Indian Army. Weaponized drones with grenade-dropping mechanisms to DRDO. GPR-integrated drones for landmine detection. DGCA-approved pilot training. Basically, if the Indian military needs something that flies and doesn’t ask questions, NeoSky is the startup they call. Market size: ₹1.66 lakh crore by FY28 (drone market in India).

House of Gen Z Brands — Fyltr (smart casual), Pump’d (athleisure), Inkd (denim), Kaari (ethnic premium), Kalaanj (ethnic economy), Akkord (musical instruments), Neomate (stationery). All on Amazon. ASP ranges from ₹160 to ₹1,699. The logic: Gen Z doesn’t trust traditional retail; Amazon does the selling; we do the sourcing. Margins? Undisclosed. Profitability? Ask us in 2027.

Rattan Power (Residual Holding) — A 1,350 MW thermal power plant in Amravati, Maharashtra. Divested from 22.07% to 19.81% shareholding in 2024. Still running profitably at 79% PLF. Generates ₹226 crore EBITDA quarterly. Why still hold 19.81%? Because you never sell an asset that prints cash. You just hold it and let the stock market remind you why you’re still rich.

The CEO of Cocoblu, Mouli Venkataraman, is an IIT Madras + IIM Lucknow alumnus with retail experience from Cloudtail, Asian Paints, and Nokia. Translation: he knows how to scale fast. Cocoblu’s 35% growth in 9M FY26 vs. peer e-commerce companies (Swiggy, Meesho, FSN E-Commerce) that are either unprofitable or niche is the data that matters. Everyone else is a delivery app or a niche marketplace. Cocoblu is becoming Amazon’s logistics arm with a 30% commission structure.

💬 Which of these five businesses would you bet on actually turning profitable within 24 months? Cast your vote in the comments. (Cocoblu is not an option — everyone knows that one.)

04 — Financials Overview

Q3 FY26: The Numbers You Were Warned About

Result type: Quarterly Results (Q3 = Dec 2025) | Q3 FY26 EPS: ₹-1.17 | Annualised EPS (Q3×4): ₹-4.68 | TTM EPS: ₹-2.97

| Metric (₹ Cr) |

Q3 FY26

Dec 2025 |

Q3 FY25

Dec 2024 |

Q2 FY26

Sep 2025 |

YoY % |

QoQ % |

| Revenue | 2,006 | 1,921 | 2,124 | +4.4% | -5.6% |

| Operating Profit | -155 | -165 | -436 | +6.0% | +64.5% |

| OPM % | -8% | -9% | -21% | +100 bps | +1300 bps |

| PAT | -162 | -170 | -397 | +4.7% | +59.2% |

| EPS (₹) | -1.17 | -1.23 | -2.87 | +4.9% | +59.2% |

The Asterisk Notes: Q3 loss of ₹162 crore includes ₹189 crore in unrealised notional losses (MTM on Rattan Power shares). Strip that out, and core PBT is ₹13 crore positive. So the company is technically profitable if you ignore the number that makes it look unprofitable — which is exactly how every loss-making startup argues with their investors. The improvement in OPM from -21% (Q2) to -8% (Q3) is real though. Cocoblu is carrying the P&L on its shoulders. Cocoblu’s Q3 contribution was the only reason they didn’t post a ₹400+ crore loss across the board.

05 — Valuation: Fair Value Range

What’s This Chaotic Conglomerate Actually Worth?

Method 1: Sum of the Parts (SOTP)

Cocoblu trading at 3-4x revenue = ₹17,000-22,000 Cr valuation. Revolt Motors (pre-IPO startups in auto trade at 5-8x revenue) = ₹2,000-3,000 Cr. NeoSky (early defence tech, super high multiples) = ₹500-1,000 Cr. House of Gen Z Brands = ₹300-500 Cr. Rattan Power at 10x EBITDA = ₹2,260 Cr. Add it up: ₹22,000-28,000 Cr. Subtract holding company discount (20%): ₹17,600-22,400 Cr.

Per Share: ₹128 – ₹163

Method 2: Comparable Valuation

Eternal (luxury goods) trades at 1012x P/E (essentially a meme valuation). Swiggy trades at 0x (unprofitable). FSN E-Commerce trades at 459x. Meesho is unprofitable. CartTrade at 39.57x. RattanIndia is unprofitable but growing. Apply a 0.8x–1.2x multiplier to sector medians if profitable = not applicable here.

Using EV/Sales multiples instead (since earnings are negative):

Per Share: ₹32 – ₹48

Method 3: Risk-Adjusted Growth Play

9M FY26 revenue is ₹5,834 crore. If we assume 15% CAGR for the next 3 years (conservative for a multi-segment startup portfolio), TTM annualized = ₹7,779 crore by FY27. At 2.5x–3.5x EV/Sales (appropriate for high-growth tech conglomerates with losses), = ₹19,448-27,227 Cr EV. Current debt is ₹1,110 crore, cash is negligible.

Per Share: ₹122 – ₹156

Fair Min: ₹32

CMP: ₹28 | Bear Case: ₹32

Fair Max: ₹163

CMP ₹28

Bear Case ₹32

⚠️ EduInvesting Fair Value Range: ₹32 – ₹163. Current price ₹28 is below even the bear case because markets hate loss-making companies, regardless of growth. This range assumes Cocoblu continues growing 15%+ and Revolt reaches profitability by FY27–28. This fair value range is for educational purposes only and is not investment advice.

06 — What’s Cooking: News, Triggers & Drama

The Plot Keeps Thickening