General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

Revenue crossed ₹1,000 crore for the first time in FY26, reaching ₹1,068 crore—a 26.5% jump. Net profit climbed ₹111 crore, up 35.1% from the year before. Yet the stock price at ₹895 sits near its March 2026 close, leaving the P/E at 20.3x against a peer band of 20–80x. Working capital days jumped from 37 to 98, an alarm bell buried under the revenue cheer.

The cash pile now ₹531 crore in investments—the company spends more time managing money than making it. The order book grew, but margins compressed. A business with momentum, yes. A business with friction, also yes.

Question: Does crossing the ₹1,000 Cr line change anything, or is this just the law of large numbers at play?

2. Introduction

India Nippon Electricals has been plugging ignition systems into two-wheelers since 1984, when Lucas-TVS and a Japanese partner (MAHLE) decided India’s motorcycle market needed better spark. For decades it was a quiet supplier play—TVS, Bajaj, Hero, Suzuki knew the name. The stock didn’t.

In 2023, Lucas Indian Service consolidated ownership, acquiring stakes from the Japanese partners and pushing its holding to 70.32%. The message: family wants full control. Since then the company has hustled: new EV products, aftermarket push, a Borg Warner ECU licensing deal in motion. The product portfolio reads like a tech roadmap—not just ignition anymore, but sensors, controllers, and electric vehicle brains.

Financials have obliged. FY24 saw ₹724 crore revenue. FY25 added ₹121 crore. FY26 added another ₹224 crore. The two-wheeler boom, rural demand, and a supply constraint in competitors’ magnets have all tilted the field. But velocity comes with a cost: working capital discipline.

3. Business Model: WTF Do They Even Do?

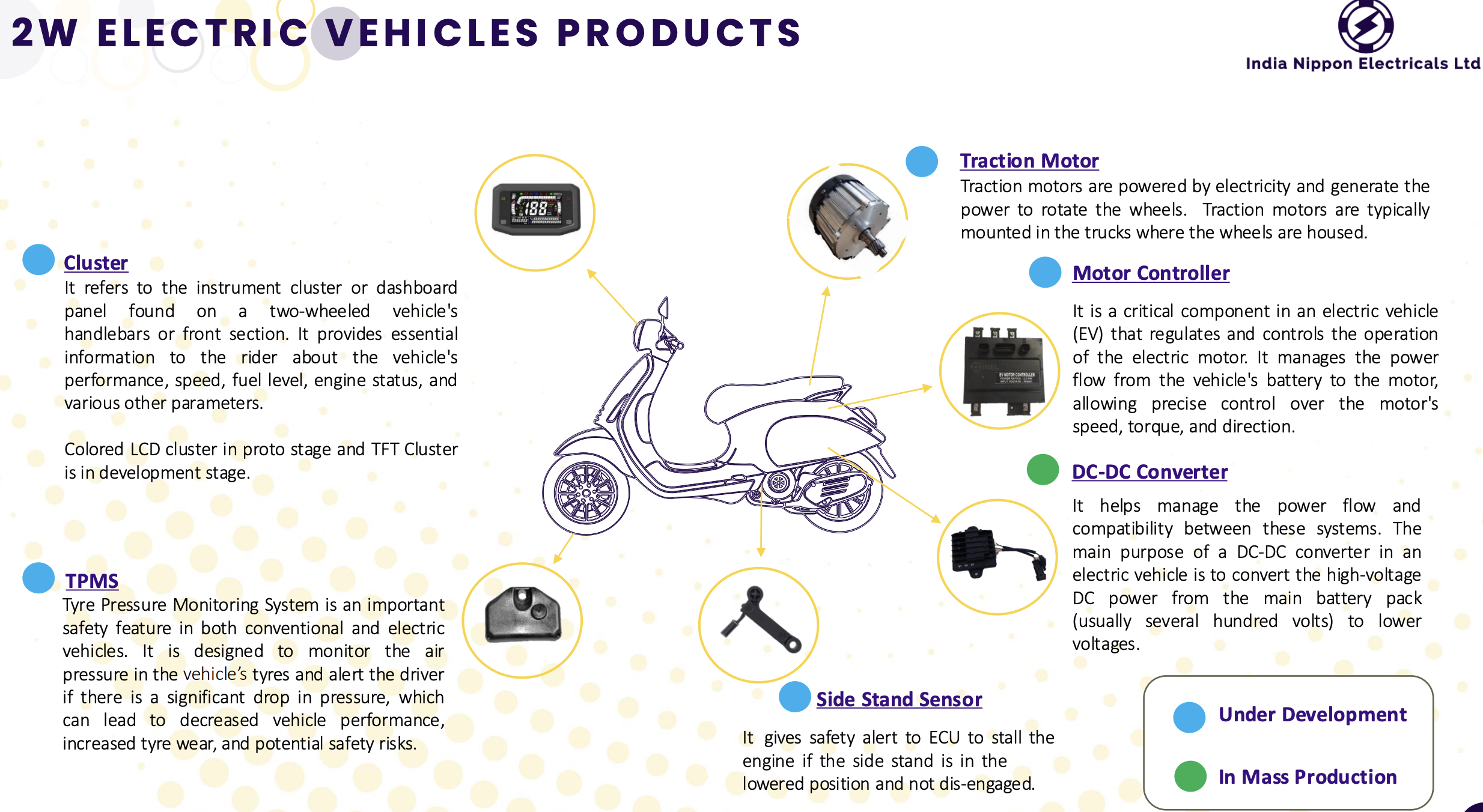

Two-wheelers are 85% of the revenue cake. Three-wheelers chip in 6%. General-purpose engine parts round it out at 9%. The company makes electronic ignition systems that replace the old mechanical systems—the kind that guaranteed no start on a humid Thursday. Today’s version manages the air-fuel mixture with precision, which is why every OEM wants it.

The product range has broadened. Controllers (ECUs) regulate engine and transmission logic. Sensors monitor pressure, temperature, position. Aftermarket teams push replacement ignition sets into the dusty supply chains of rural India and exports. The real gold, management hopes, is in EV technology—the company opened a tech center in Tamil Nadu to design motor controllers and DC-DC converters for electric two and three-wheelers. A licensing deal with Borg Warner for Electronic Fuel Injection ECUs signals the company is trying to own the software stack.

Geography remains skewed: 92% of revenue from India, 8% exports. But exports now touch USA, Italy, Japan, Thailand, Vietnam, Africa—the spread is widening. Key customer concentration is high (top customers ≈ 42% of revenue over five years), a structural risk that nobody mentions out loud.

Manufacturing lives in three plants: Hosur and Puducherry in Tamil Nadu, Rewari in Haryana. In FY26, the company commissioned a new production line for Flywheel Magneto systems at Rewari and kicked off SoP (Start of Production) for high-end motorcycles at Hosur. Capex was ₹42 crore, a 10-year high. The company is building to scale.

4. Financials Overview

Figures are consolidated, in ₹ crore.

Metric

FY24

FY25

FY26

YoY %

Revenue

724.1

844.8

1,068.5

+26.5%

EBITDA

66.4

95.2

122.2

+28.4%

Net Profit

59.3

82.3

111.2

+35.1%

EPS (Annualised)

26.21

36.37

49.14

+35.1%

Q4 FY26 alone: Revenue ₹299.5 crore (up 28% YoY), Net Profit ₹39.8 crore (up 47.4% YoY). The exceptional item—land compensation from Haryana government, ₹152 crore—is a one-time gift. Strip that out, and Q4’s PAT is ₹25 crore, still healthy but less dramatic.

EBITDA margins expanded from 8.8% in FY23 to 11.4% in FY26—steady, unhurried progress. PAT margins went from 7.3% to 10.4%, which is respectable for a supplier business. The path shows operational leverage, though inflation in raw materials and fuel (the concalls mention Middle East tensions