General information and entertainment, not investment advice. The author is not a SEBI-registered adviser or research analyst. No recommendation, no promised returns. Markets carry risk including loss of capital. Figures may not be current. Consult a registered adviser before acting.

1. At a Glance

Regaal Resources doubled its crushing capacity to 1,650 TPD on May 26, 2026—nine days after closing FY26 results. Revenue grew 23.9% to ₹1,134 Cr. Profit after tax grew 16.6% to ₹556 Cr. The listed wet-milling company remains dependent on a single product (native maize starch, 45.5% of revenue) while creditor interests swelled to ₹614 Cr against a market cap of ₹850 Cr.

Capacity is doubled; profitability trails. That’s the tension.

The margin compressed 30 basis points year-over-year as trading activity (cost of goods sold, buying and reselling maize) expanded. Return on equity fell to 11.5% from 20.3% in FY25. Return on capital employed, 10.7% against peer medians of 14–18%.

Regaal sold an IPO into a market already pricing vigor and landed at ₹82.5 nine months later. Prices referenced are not live; this analysis uses ₹82.5 as a reference point.

Wisdom: Capacity growth that outruns return on capital is always a story worth skepticism.

2. Introduction

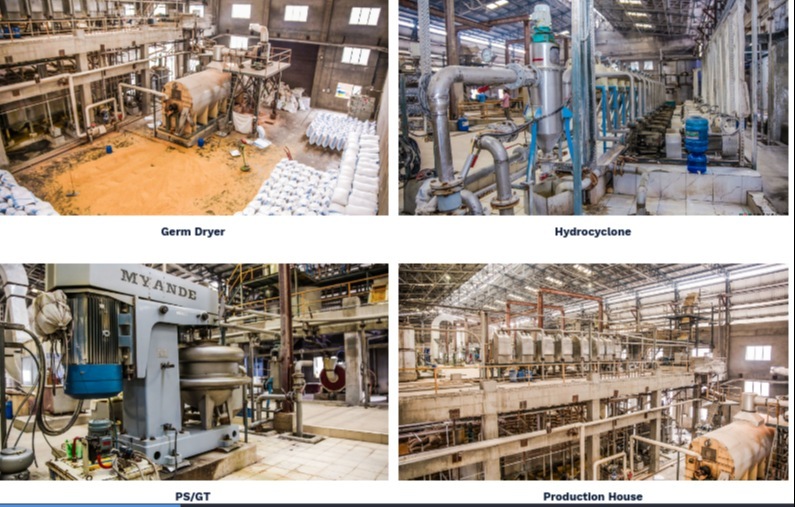

Regaal Resources Limited was founded in 2016 and began production in 2018—eight years and nine months of operating history as of June 2026. It has since grown from 180 TPD (tonnes per day) of crushing capacity to 1,650 TPD, a 9x expansion in less than a decade, placing it among India’s fastest-growing wet-milling operators.

The company went public on NSE and BSE on August 20, 2025, listing at ₹102. It raised ₹306 Cr via IPO: ₹210 Cr fresh issue (for repayment of borrowings and general corporate purposes) and ₹96 Cr from promoter share sale. The new capacity expansions announced in May 2026—including a 180 TPD liquid glucose (LG) plant and a 50 TPD maltodextrin powder (MDP) facility—were commissioned just 40 days after statutory filings closed.

Anil Kishorepuria, founder and CMD, holds 25.39% personally; his family and linked entities (BFL, SRM private) control 71.3% of shares. Promoter shareholding increased 87 basis points in Q4, a small vote of confidence or a signal that the public float is still settling.

The company has faced tax demands totaling ₹149 Cr (GST and income tax) since January 2026, plus ₹8.88 Cr already paid to the GST authority; corporate governance penalties from ROC totaling ₹3.3 Cr have been imposed for delayed director appointments and valuation omissions in their IPO documents.

3. Business Model: WTF Do They Even Do?

Regaal buys maize (corn) in bulk, mills it into a slurry, and separates that slurry into products: starch, gluten, germ, fiber, steep liquor, and co-products. This is wet milling. It is not new. Wet-milled maize starch is industrial plumbing: it goes into paper coatings, food gelling, adhesive binders, and textile sizing.

Native maize starch accounts for 45.5% of FY26 contract price revenue (₹517 Cr of the mix). Modified starch (dextrin, edible starch) is 0.5%. Co-products (gluten, germ, fiber) are 20.6%. Value-added products (icing sugar, custard powder, baking powder, maize flour) moved from 0.5% to 2.7% of revenue over three years—scaling but still marginal. Trading and others (bought-and-resold maize, minimal margin) were 30.7%, a segment that expands and contracts with raw-material procurement cycles.

Customers sit in paper (27%), animal feed (13%), food manufacturing (7.5%), and miscellaneous industrial (16.5%), leaving 36% dispersed. The top 10 customers account for 39.4% of revenue (down from 55% in FY23)—concentration is declining, which some call diversification and others call loss of volume.

The company has 345 unique customers as of Mar 2026 and added 134 new ones in FY26. Repeat customers number 211. Distribution has shifted: dealer channel share grew to 65.5% by FY26 (from 42.7% in FY23), while direct-to-manufacturer sales fell from 55% to 31%.

Regaal has a Zero Liquid Discharge (ZLD) water recycling unit—a cost center that governments favor. It has 65,000 MT of maize silo storage, 15.8 MW of captive co-generation power (80.85% of power needs in FY26 from self-generation), and location 110 km from Gulabbagh mandi, one of India’s largest maize trading hubs. The facility sits in Bihar, one of India’s top three maize-producing states. Proximity to Nepal and Bangladesh borders enables exports.

The model is asset-heavy, input-cost-sensitive, and dependent on industrial-end demand, which means it moves with paper mill utilization, pharma demand, and packaged food volumes. It is not a consumer brand. It has no direct pull; it is sold on margin to customers’ customer ecosystems.

4. Financials Overview

Figures are consolidated, in ₹ crore. Result type: Yearly (FY20–FY26). Basis: Consolidated.

Metric

FY25

FY26

YoY

Revenue

915.16

1,134.17

+23.9%

EBITDA

112.79

126.57

+12.2%

PAT

47.67

55.56

+16.6%

EPS (₹)

5.80

5.41

-6.8%

EBITDA margin compressed from 12.3% to 11.2% (down 110 bps). PAT margin fell from 5.2% to 4.9% (down 30 bps). Revenue growth of 23.9% did not translate to proportional profit growth because procurement expanded faster than pricing power. Raw material and change in inventory consumed 71.6% of revenue in FY26 vs. 73.3% in FY25—a 170 bps improvement, but offset by expansion in other manufacturing expenses and a ₹140 Cr “Other Expenses” item in the filing (likely one-time or reclassified items).

Q4 FY26 sales were ₹245 Cr, down 5.4% quarter-on-quarter, a seasonal dip. PAT was ₹16.5 Cr, yielding a quarterly EPS of ₹1.61 (annualised to ₹6.44, which matches neither the trailing nor the full-year figure—the company’s diluted EPS disclosure accounts for bonus and split effects). Operating profit (EBITDA) in Q4 stood at ₹33 Cr, a margin of 13.3%, the strongest quarterly margin of the year, suggesting seasonal strength in Q4 realizations.

The management commentary noted that Q4 margins expanded due to “lower trading activity” and “better realizations across the company’s core product portfolio.” In plain English: fewer low-margin trading deals and higher prices for core products in March 2026. Whether that sticks into FY27 is an open question.

5. Valuation Discussion: Fair Value Range (Educational Only)

What follows is a walkthrough of how three valuation methods work, using this company’s numbers as the example — not a target, not a forecast, not advice.

Method 1 (P/E multiple): Annualised EPS for FY26 is ₹5.41. Regaal trades at ₹82.5, implying a P/E of 15.2x. The peer band for maize-starch and agro-processing companies ranges from 12–24x (median 16.7x). At a peer median multiple of 16.7x, the arithmetic produces ₹5.41 × 16.7 = ₹90.4 Cr; at a conservative band of 12–20x, the range is ₹64.9 – ₹108.2.

Method 2 (EV/EBITDA): FY26 EBITDA was ₹126.6 Cr. Total debt was ₹614.5 Cr; cash was ₹151.4 Cr; net debt ₹463 Cr (excluding IPO proceeds as of March 2026, the presentation notes unused funds). Enterprise value at current market cap and net debt: (850 + 463 = 1,313 Cr). Current EV/EBITDA is 10.4x. Peer median EV/EBITDA across the set is 12.5–15x. At 13x EBITDA and net debt of ₹463 Cr, the arithmetic produces (126.6 × 13) – 463 = ₹1,185.8 – 463 = ₹722.8 Cr equity value, or ₹70.3 per share on 10.3 Cr shares.

Method 3 (simplified DCF – illustrative): A 5-year forward EBITDA growth at 15% annually (in line with FY23–FY26 CAGR of 12%, slightly optimistic) produces FY30 EBITDA of ₹256 Cr. Terminal EBITDA multiple of 10x (conservative) gives ₹2,560 Cr. Discounted at 10% WACC, five-year NPV approximates ₹1,590 Cr enterprise value. Less net debt of ₹463 Cr = ₹1,127 Cr equity, or ₹109.6 per share.

These figures show how the methods work and are not a valuation, a target, or advice.