Ganesha Ecosphere FY26: A Story of Regulated Resurrections and Trashed Greenfield Dreams

Section 1 — At a Glance

The fiscal year ended March 31, 2026, was a masterclass in why structural growth stories should never be evaluated on a linear axis. Ganesha Ecosphere Ltd reported a consolidated revenue from operations of ₹1,481.66 crore for FY26. This represents a pedestrian top-line growth of 1.10% compared to the ₹1,465.54 crore generated in FY25. However, this flattish annual trajectory masks a dramatic operational fracture. The first nine months of the fiscal year were severely crippled by regulatory uncertainty. This completely halted buying velocity across the sustainable packaging supply chain. The fourth quarter, by contrast, delivered a historic volume breakout. Consolidated revenue surged 18.68% sequentially to ₹423.94 crore.

While the volume engine re-ignited, the financial cost of surviving a nine-month regulatory ice age was painfully evident in the full-year profitability metrics. Full-year consolidated Profit After Tax (PAT) collapsed by 62.95% to ₹38.21 crore. This is down from ₹103.12 crore in the previous fiscal year.

The primary stress point remains the legacy textile recycling segments, which face acute structural margin compression. Conversely, the higher-margin food-grade recycled Polyethylene Terephthalate (rPET) granules business is seeing strong demand. This demand is heavily driven by strict regulatory mandates. The market is currently grappling with a classic small-cap dilemma. It must balance visible, compliance-driven long-term demand against immediate margin pressure in raw material inputs.

In asset-heavy recycling models, regulatory clarity acts as the ultimate arbiter of capital efficiency. Without it, capacity expansion simply builds low-yielding steel.

The core narrative has now shifted from an aggressive regional capacity build-out to rapid domestic asset optimization.

Section 2 — Introduction

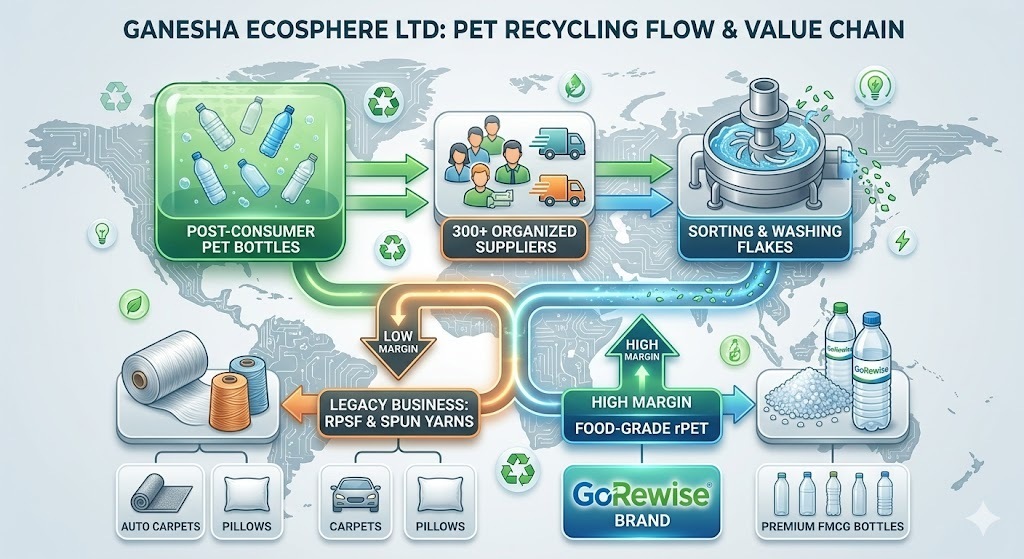

Ganesha Ecosphere has spent more than three decades building a circular economy infrastructure. The company has transformed itself from a traditional synthetic textile manufacturer into India’s largest collector and recycler of post-consumer PET bottle waste.

Operating a nationwide sourcing network of over 300 organized suppliers, the group processes approximately 450 tons of plastic waste daily. This vast raw material pipeline feeds six production plants across North and South India, as well as a processing hub in Nepal.

The corporate growth strategy recently shifted toward a clean technology portfolio under the “GoRewise” brand. This brand specializes in premium textile-grade and FSSAI-approved food-grade rPET granules. However, entering highly regulated food-contact packaging requires navigating complex global supply chains and erratic regulatory timelines. This complexity was fully visible during the volatile execution cycle of FY26.

Section 3 — Business Model: WTF Do They Even Do?

The core business model relies on turning garbage into high-value manufacturing inputs. Ganesha Ecosphere acts as a garbage vacuum cleaner. It sucks up over 16% to 18% of India’s total PET bottle waste. This translates to recycling over 8 billion discarded bottles annually.

The collection infrastructure gathers dirty bottles, which are then sorted, shredded, and aggressively scrubbed into clean rPET flakes. From there, the company splits its production into two very different segments:

The Legacy Fiber Engine: Converting flakes into Recycled Polyester Staple Fibre (RPSF) and spun yarns. These products are sold to spinning mills and technical textile clients for low-margin applications like car carpets and pillow stuffing.

The GoRewise Compliance Play: Utilizing super-clean technologies to turn flakes into food-grade rPET granules. These are sold directly to Fast-Moving Consumer Goods (FMCG) majors for premium bottle packaging.

The financial challenge here is that while the GoRewise segment benefits from strong regulatory support, the legacy fiber business remains vulnerable to shifting global commodity prices.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trajectory

Metric

Q4 FY26

Q3 FY26

Q4 FY25

YoY (%)

QoQ (%)

Revenue

423.94

357.22

344.38

23.10%

18.68%

EBITDA

52.29

30.73

47.06

11.11%

70.16%

PAT

23.21

4.75

21.60

7.45%

388.63%

EPS (Reported)

8.66

1.77

8.52

1.64%

389.27%

The sequential jump in Q4 FY26 profits looks spectacular. However, a closer look shows this was largely a relief rally. It came after a very difficult Q3 period, where PAT dropped to just ₹4.75 crore due to severe supply chain bottlenecks.

What is Management Promising in the Coming Quarters?

During the May 2026 earnings call, the CFO explicitly guided for an absolute consolidated EBITDA range of ₹225 crore to ₹250 crore for FY27. Management noted that their primary focus is stabilizing conversion margins rather than chasing volatile raw material prices. The CEO stated:

“The supply pipeline across the downstream value chain is completely empty due to continuous destocking. With the regulatory smoke cleared, we expect a strong volume ramp-up across our premium rPET lines.”

Management also reported that their high-margin recycled filament yarn has successfully qualified with a major