Hindustan Foods Q4 & FY26: A ₹4,251 Cr Monolith Disguised as a Humble Subcontractor

At a Glance

Hindustan Foods Limited closed its financial year 2026 by hammering home its largest-ever full-year and quarterly performance. Annual revenue from operations reached ₹4,251.04 crore, representing a 19.26% expansion over the previous financial year. The bottom-line metrics kept pace, with net profit surging 35.93% to land at ₹149.03 crore for FY26. This rapid expansion was structurally supported by an aggressive capital expenditure cycle, culminating in a record ₹780 crore in annual project wins and a gross asset block that scaled to ₹1,800 crore.

While top-line trajectories and volumetric growth signals reflect healthy end-market demand across fast-moving consumer goods, footwear, and consumer wellness, the company’s financial mechanics revealed pockets of operational drag. Aggressive diversification into labor-intensive shared-manufacturing verticals has fundamentally elongated the working capital engine, dragging down structural cash flow conversion. Simultaneously, asset utilization metrics remain compressed as newly commissioned greenfield installations navigate multi-quarter operational stabilization periods. When capital deployment aggressively outpaces instantaneous cash generation, a business transforms its balance sheet from a localized cash generator into a leveraged bet on future utilization ramp-ups. Investors are left assessing whether the company can successfully optimize returns across its expanded base or if it will find its capital efficiency permanently structurally diluted.

Introduction

Hindustan Foods Limited functions as the industrial backbone behind some of India’s most visible brand portfolios. Operating under the corporate umbrella of the Vanity Case Group, the company has engineered a structural pivot from its historic origins. It began as a specialized, single-brand joint venture between GlaxoSmithKline and the Dempo group, established exclusively to manufacture the nutritional food formulation ‘Farex’. Hamstrung by the operational vulnerabilities of dependency on a lone consumer brand, the entity endured multiple years of chronic financial losses.

The inflection point arrived in 2013 following its acquisition by Vanity Case India Private Limited, which took a definitive 74.45% controlling stake. New management fundamentally overhauled the corporate architecture, discarding the singular branded approach in favor of a scaled, multi-customer contract manufacturing model. Today, the business operates across multiple high-growth categories including home care, personal care, packaged beverages, extruded foods, consumer healthcare, and leather footwear. By building out localized manufacturing infrastructure across key industrial hubs, the firm has positioned itself as an essential partner to top-tier enterprise clients looking to outsource production.

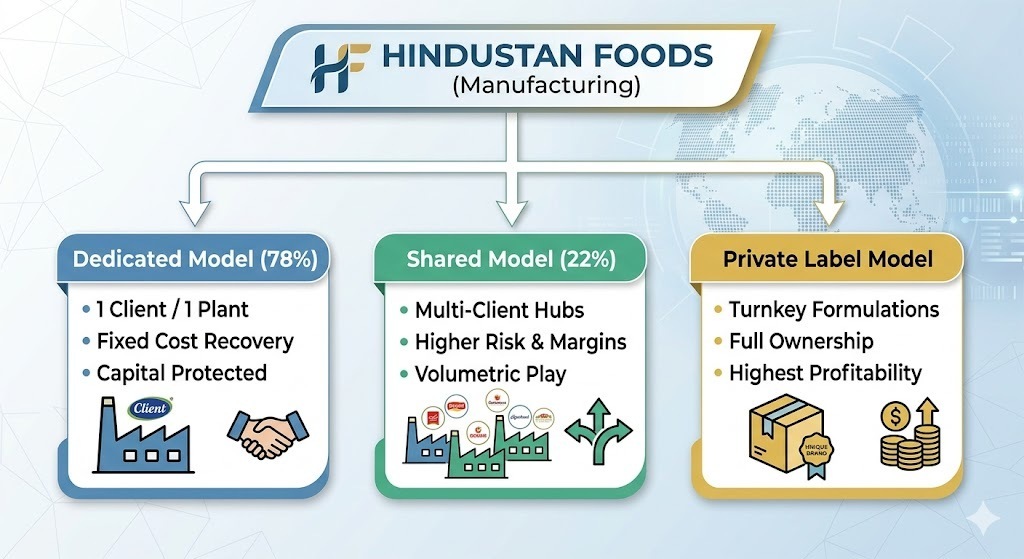

Business Model: WTF Do They Even Do?

Hindustan Foods is essentially the corporate equivalent of a high-end ghost kitchen, but instead of assembling gourmet burgers for food delivery applications, it runs heavy industrial machinery to churn out detergent bars, ice cream sticks, and sneakers for multinational consumer giants. The company operates a network of production hubs, deliberately spread out across regional territories like Goa, Coimbatore, Baddi, Jammu, and Silvassa. They don’t spend sleepless nights worrying about retail distribution or advertising campaigns; they let enterprise clients handle the marketing while they focus entirely on optimization of factory throughput.

The manufacturing ecosystem is neatly divided into three operational buckets:

Dedicated Manufacturing (78% of Revenue): This is the ultimate corporate security blanket. Hindustan Foods builds or acquires an entire factory, slaps a single client’s name on the gate, and signs a long-term contract that guarantees the recovery of all fixed costs and debt-servicing obligations regardless of actual production volumes. It accounts for the vast majority of the top line, giving the balance sheet highly predictable cash flows.

Shared Manufacturing (22% of Revenue): This is where they invite multiple brands to share the same assembly lines. It carries higher utilization risks and operational friction, but when the lines are running flat out, it offers significantly better margins than the dedicated model.

Private Label Manufacturing: The company owns the underlying product formulations and offers turnkey solutions to retail brands. Because they control the raw material selection and intellectual property, this boutique vertical stands as the most profitable engine in their portfolio.

Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4FY26)

YoY (%)

QoQ (%)

Revenue

₹1,120.90

16.54%

7.19%

EBITDA

₹104.10

27.89%

7.54%

PAT

₹41.55

31.90%

7.09%

EPS (Reported)

₹3.43

29.43%

7.19%

Quarterly revenue crossed the four-digit mark at ₹1,120.90 crore, outperforming the ₹961.80 crore delivered in the same period last year. Operating leverage kicked in cleanly, allowing quarterly PAT to climb to ₹41.55 crore. However, this quarter wasn’t entirely clean; profitability absorbed an exceptional charge of ₹1.1 crore linked directly to structural realignments under the new labor code.

What is Management Promising in the Coming Quarters?

During the May 2026 earnings call, management issued an explicit full-year