Xchanging Solutions Mar 2026: The ₹312 Crore Cash Pile Trading at 12x Earnings

Section 1 — At a Glance

A multi-year stagnation in corporate top-line metrics frequently masks a massive structural realignment in core capital allocation strategy. Xchanging Solutions Ltd presents a stark clinical case of an micro-cap technology entity where operational revenue has remained essentially trapped within a narrow structural band, yet corporate net profitability and cash reserves have expanded significantly. The structural conflict is immediate: while five-year compound annual sales growth languishes at a highly compressed 0.72%, net profit for the fiscal year ended March 31, 2026, surged to ₹59.45 crore, representing a substantial 19.91% expansion year-on-year from ₹49.58 crore.

This bottom-line efficiency is entirely driven by capital recoveries and severe cost optimization rather than expanding industrial market share. The primary analytical concern centers on the structural drop in operating cash flows relative to accounting profits alongside multi-year litigation liabilities that threaten a significant portion of corporate liquid assets. Corporate resource management remains highly unusual, characterized by the maintenance of an exceptional cash and bank balance of ₹311.72 crore against a total market capitalization of just ₹751.11 crore.

When an enterprise hoards liquid cash equivalent to more than 40% of its total market valuation while maintaining a flat multi-year revenue trajectory, the economic entity is no longer operating purely as a technology services company; it is effectively functioning as a closed-end capital repository with an internal IT business attached to it.

The primary structural question is whether the upcoming corporate era under a reconstituted executive suite can translate this massive internal balance sheet liquidity into actual structural market growth, or if the asset base will remain heavily underutilized while being chipped away by regulatory transfer pricing adjustments.

Section 2 — Introduction

Xchanging Solutions Ltd represents an intriguing case study of a legacy multinational corporate stepchild operating quietly within the Indian public equity markets. Originally incorporated in 2002, the entity functions as an Information Technology services provider specializing in IT software, hardware, and computer programming solutions with a heavy global delivery footprint. The structural architecture of the company is highly institutionalized; it operates as an indirect subsidiary of DXC Technology Company—a major technology systems integrator listed on the New York Stock Exchange. DXC controls a rigid 75.00% promoter stake through a web of intermediate holdings led by Xchanging (Mauritius) Limited.

The operational focus of the company has fundamentally pivoted away from scale and toward extreme financial lean-ness. Over the last several years, management has chosen to wind down capital-intensive domestic pursuits to optimize for high-margin, predictable foreign software service provisions. This shift culminated in a significant structural transition on March 4, 2025, when the long-serving Managing Director and CEO, Mr. Nachiket Vibhakar Sukhtankar, exited the firm and was replaced by Mr. Swaminathan Swaminathan to oversee this highly mature, cash-rich capital structure.

Section 3 — Business Model: WTF Do They Even Do?

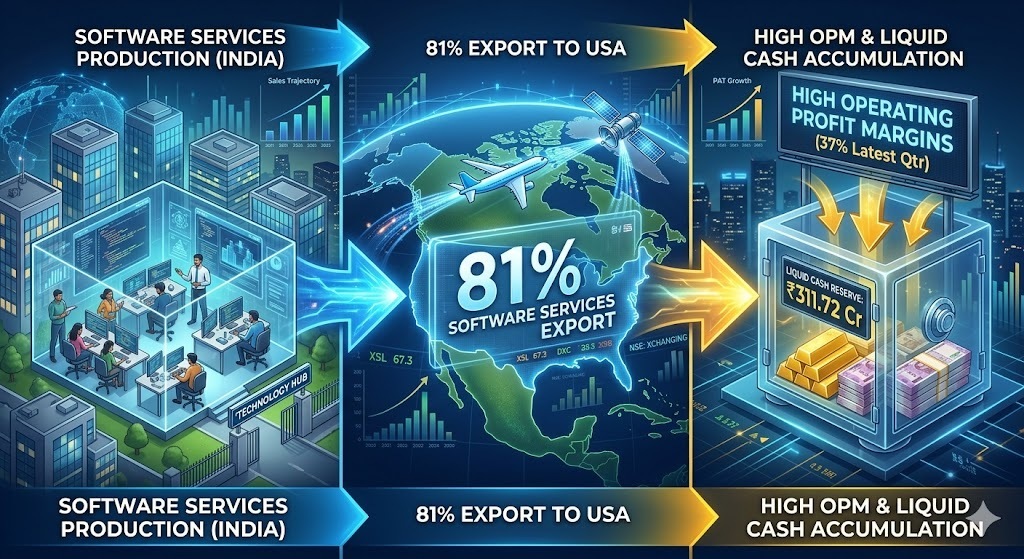

If you walk into Xchanging Solutions expecting to find engineers building the next generative AI frontier model, you will find yourself staring at an incredibly quiet, highly optimized billing machine instead. The business model is essentially a structural pipeline designed to funnel software development services from India directly into Western corporate architectures—specifically the United States.

To understand how hyper-concentrated this operational model truly is, look at the structural revenue splits for the entity:

By Business Line: Sale of Software services accounts for a dominant 89% of the top-line, leaving a tiny residual sliver for hardware and ITES. The remaining 10% comes from interest income generated by its massive, stagnant pool of cash.

By Geography: The United States represents a staggering 81% of total consolidated revenue, while Singapore commands 10%. The home turf of India is an afterthought at a meager 7%.

The entity operates as a captive offshore delivery unit for its global ultimate parent, DXC Technology. It does not scale via aggressive client acquisition; it maintains a highly exclusive pool of long-term maintenance and Time & Material contracts. In essence, Xchanging Sol behaves less like an agile tech outfit and more like a contractual software annuity stream that trades geographic operational complexity for deep, predictable dollar-denominated cash flows.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

Metric

Latest Quarter (Mar 2026)

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue

51.30

50.74

48.82

EBITDA / Operating Profit

19.07

17.35

16.08

PAT

16.24

14.65

13.18

EPS (₹)

1.46

1.32

1.18

The quarterly trajectory illustrates an absolute masterclass in extracting structural efficiency out of completely flat top-line dynamics. Quarterly revenue crept up by a minor 1.10% year-on-year to ₹51.30 crore. Yet, look at the operating profit line, which scaled up by 9.91% over the same exact period to ₹19.07 crore.

Did Management Walk the Talk?

Reviewing past guidance against the structural financial statements reveals an executive team that has completely abandoned corporate growth guidance to focus entirely on margin protection. With a total permanent employee headcount that has dropped structurally from