Walchandnagar Industries Ltd Mar 2026: The ₹15 Crore Turnaround and the Satara Lockdown Surcharges

Walchandnagar Industries has pulled off a dramatic final act for the financial year. After spending most of FY25 drowning in deep operational losses, the turn of the year brought a curious mathematical miracle: the company reported a positive net profit in back-to-back quarters, closing out March 2026 with a quarterly profit of ₹2.94 crore. Yet, beneath this newfound operational joy lies a business still highly dependent on an ancient heavy engineering portfolio and a balance sheet that has spent the year aggressively reallocating capital to keep its lenders quiet.

While headline metrics indicate the bottom line has successfully narrowed its full-year pain, structural weaknesses remain tightly fastened to the core infrastructure. Promoters continue to struggle with liquidity, over 49% of their skin in the game remains locked away in pledges, and the core heavy engineering division is carrying the dead weight of a practically idle foundry division. The turnaround is mathematically real, but it remains heavily subsidized by “other income” and strategic land asset liquidation options rather than standalone manufacturing excellence.

Section 2 — Introduction

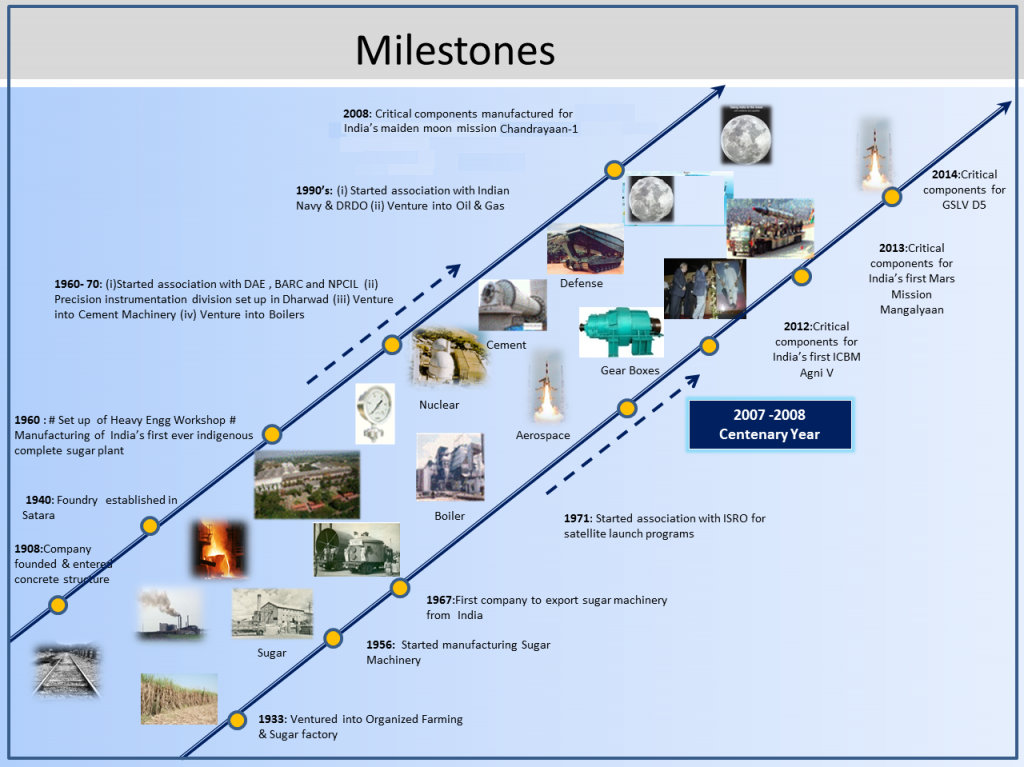

Walchandnagar Industries Ltd (WIL) is an ancient, heavy engineering titan that has seen the inside of India’s industrial landscape since its inception in 1908. Based out of its newly consolidated corporate headquarters in Pune, the company acts as a high-tech project execution specialist, manufacturing massive specialized machinery for aerospace, defense, and core industrial sectors.

Despite its prestigious lineage—including supply lines for space flight sub-assemblies and advanced defense missile components—the operational reality of late has resembled a complex structural puzzle. The financial year 2026 was less about smooth manufacturing automation and more about intense fire fighting, marked by severe labor unrest at its primary Satara manufacturing plant and a massive corporate restructuring that involved packing up its legacy offices and liquidating real estate to protect its cash reserves.

Section 3 — Business Model: WTF Do They Even Do?

To put it elegantly, Walchandnagar Industries builds things that are far too large to fit into a regular cargo container. They are custom heavy-engineering architects. Their business model is divided into three parts: a high-tech Heavy Engineering unit that brings in a massive 77% of their revenue, a Foundry and Machine Shop at 14%, and an assortment of miscellaneous “Other” services picking up the remaining 9%.

They don’t sell fast-moving consumer products; they win giant institutional orders—such as manufacturing a 64-meter-long HF Kiln (marketed proudly as the longest in the world) or supplying specialized hardware to the Vikram Sarabhai Space Centre (VSSC). The revenue mix is overwhelmingly skewed toward domestic buyers, who account for 96% of the billing ledger. The remaining 4% is exported to international clients who presumably enjoy the thrill of tracking a multi-ton industrial gear moving across the ocean.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Financial Performance Trend

Metric

Latest Quarter (Mar 2026)

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue

₹93.02

₹53.08

₹80.95

EBITDA / Operating Profit

₹4.15

₹-47.10

₹15.30

PAT

₹2.94

₹-56.12

₹4.66

Reported EPS

₹0.43

₹-8.32

₹0.69

The financial year ended on a highly erratic note. Revenue for the March 2026 quarter jumped to ₹93.02 crore, representing an explosive 75.2% expansion compared to the abysmal industrial freeze of March 2025. This dramatic spike helped flip the previous year’s massive operational loss into a positive quarterly operating profit of ₹4.15 crore.

Financial Wisdom Drop: A rapid surge in quarterly revenue that occurs alongside a heavy collection of other income can often hide underlying weaknesses in factory productivity.