Sansera Engineering FY26: The ₹3,498 Crore Pivot From Auto Cylinders To Aerospace Blisks

Section 1 — At a Glance

Sansera Engineering Limited concluded FY26 on an unprecedented financial trajectory, establishing a record operational scale while fundamentally shifting its core corporate architecture. Headline revenues scaled 16% to reach ₹3,498 crore, outstripping macro auto-ancillary benchmarks and illustrating the potent compounding effect of structural client extensions. Profitability expanded at a superior velocity; consolidated profit after tax reached ₹327 crore, representing an exceptional 51% year-on-year surge fueled by material shifts in internal output mix and sustained manufacturing leverage.

While historical performance remains anchored to domestic two-wheeler internal combustion engine components, the current fiscal period marks an explicit inflection point. The company’s Aerospace, Defence, and Semiconductor (ADS) vertical achieved a breakthrough product turnover of ₹316 crore, surging 155% as multi-year international supply contracts moved cleanly out of First Article Inspection and into formal commercial execution. This structural diversification significantly de-risks the capital base against impending electric vehicle transitions.

However, this accelerated expansion alters capital efficiency dynamics. Return on Capital Employed (ROCE) moderated to 14.1% as a direct result of aggressive capacity creation and an expanding working capital footprint required to back international aerospace cycles. Operating cash flow generation was partially absorbed by localized raw material inventory lock-ups in specialized components, contrasting with historic asset-light liquidation patterns. True structural durability rests entirely on management’s ability to convert an unexecuted lifetime ADS backlog of ₹4,464 crore into high-margin liquid returns before the domestic automotive cycle encounters regular cyclical deceleration.

Section 2 — Introduction

Sansera Engineering has traveled a multi-decade path from a localized domestic tier-1 forging vendor to an engineering-led international manufacturer of critical high-tolerance precision components. Originally established to supply core powertrain infrastructure like connecting rods and complex crankshaft assemblies to India’s automotive giants, the corporate strategy has systematically rotated over the last five years. The company now coordinates complex metal deformation across 18 integrated manufacturing units situated across domestic industrial zones and an overseas hub in Sweden.

The primary business objective centers on capturing high-value-add niches within segments completely agnostic to the fuel transition. Rather than succumbing to the secular decline of standard automotive internal combustion engineering, the management team has deployed capital into adjacent precision domains requiring extreme geometric fidelity, notably aerostructure brackets, advanced radar subsystems, and structural components for global aerospace OEMs. The strategic blueprint aims to extract stable, high-volume cash flows from the legacy automotive segment while simultaneously scaling technical manufacturing capabilities to claim institutional early-mover advantages in deep-tech, defense, and high-margin semiconductor manufacturing machinery.

Section 3 — Business Model: WTF Do They Even Do?

At its heart, Sansera functions as an industrial metal surgeon, transforming raw steel and aluminum billets into hyper-complex, mission-critical components that cannot afford to fail. If a component sits inside an engine under tremendous thermodynamic strain or holds together a commercial airplane wing, Sansera wants to forge, machine, and heat-treat it.

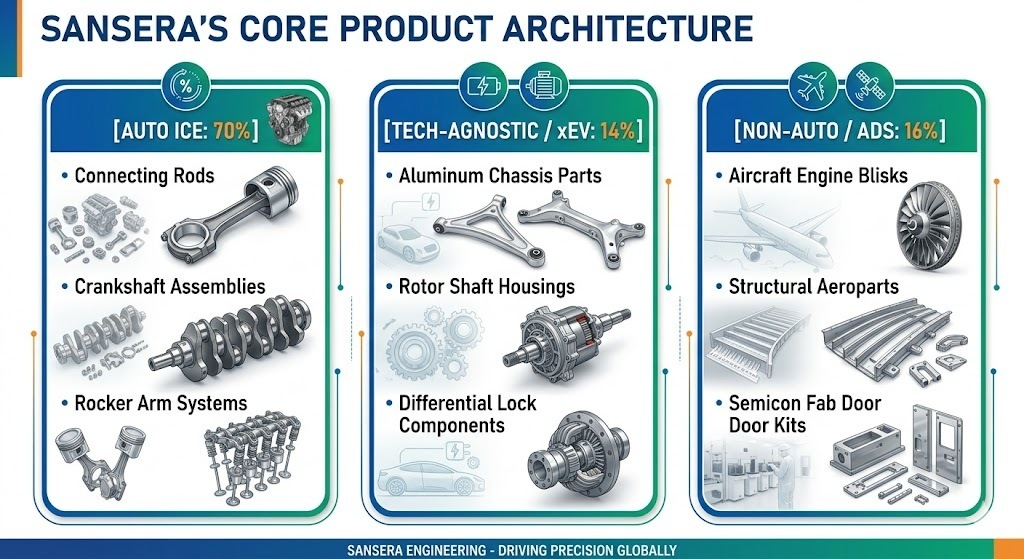

The product taxonomy is divided into distinct operational buckets:

Auto ICE (70% of FY26 Revenue): The legacy cash engine. This involves mass-producing connecting rods, integral crankshafts, and rocker arms for two-wheelers, passenger vehicles, and heavy commercial trucks. They are a global top-10 supplier of light vehicle connecting rods, which means they spend their days fighting for fractions of a rupee in client procurement offices.

Tech-Agnostic & xEV (14% of FY26 Revenue): Structural insurance against the death of gas-guzzlers. Think precision aluminum forged chassis parts, drivetrain rotor shafts, and differential lock hooks that fit into both traditional hybrids and pure battery electric vehicles.

Non-Auto (16% of FY26 Revenue): The high-margin playground. This is dominated by the Aerospace, Defence, and Semiconductor (ADS) vertical. Here, they move away from simple automotive components and step into hyper-complex structural parts, tailing edges, and landing gear parts for Boeing and Airbus, alongside ultra-high-precision door kits for semiconductor fabrication machinery.

The structural economics rely on fungible production lines. When global automotive demand softens, Sansera can physically alter tool configurations on its CNC machines to manufacture off-road components or aerospace brackets on identical shop floors. It is a model built on real industrial flexibility, converting pure capital expenditures into multi-industry capability.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4FY26)

YoY (%)

QoQ (%)

Revenue

₹998.74

+27.77%

+10.03%

EBITDA / Operating Profit

₹192.94

+51.86%

+19.08%

PAT

₹121.41

+163.59%

+76.70%

EPS

₹19.48

+102.92%

+76.45%

Did Management Walk the Talk?

Reviewing old commitments reveals an exceptional operational performance. Management previously targeted a steady reduction in rigid auto ICE concentration to approximately 60% via an aggressive diversification plan. As of the close of FY26, the non-ICE revenue mix scaled directly to 30%, ticking up to 32% within the final quarter. The overarching corporate target is no longer a distant investor-deck promise; it is actively landing on the income statement.

What is Management Promising in the Coming Quarters?