Rudra Global FY26: A ₹623 Crore Topline with a One-Percent Net Margin Twist

Section 1 — At a Glance

Rudra Global Infra Products Limited presents a classic study in the structural bottlenecks of the secondary steel sector. The headline metrics for the financial year ending March 31, 2026, display an expanding operational footprint that stands in stark contrast to its razor-thin bottom-line efficiency. Annual sales scaled a historic high of ₹622.83 crore, representing a 11.06% year-on-year growth from the ₹560.79 crore printed in the previous fiscal. However, this volumetric push failed to translate into meaningful capital surplus. Net profit for FY26 closed at a modest ₹13.51 crore, yielding an annual net profit margin of just 2.17%.

While a rating upgrade by Infomerics to IVR BBB/Stable in February 2026 underscores an improving short-term debt servicing capability, institutional vulnerability remains high. The business model requires massive working capital to sustain manufacturing cycles, which reached an elongated 144 days due to aggressive raw scrap hoarding. Total debt obligations sit heavily at ₹134.76 crore against a tangible net worth of ₹139.00 crore.

The primary operational risk resides in raw material price volatility, where scrap consumption consistently eats up over 90% of structural revenue, leaving the operating architecture exposed to global supply shocks. A capital structure dependent on high-utilization fund limits suggests that while volume expansion continues, true wealth creation remains bottlenecked by the inherent economics of re-rolling mills.

Section 2 — Introduction

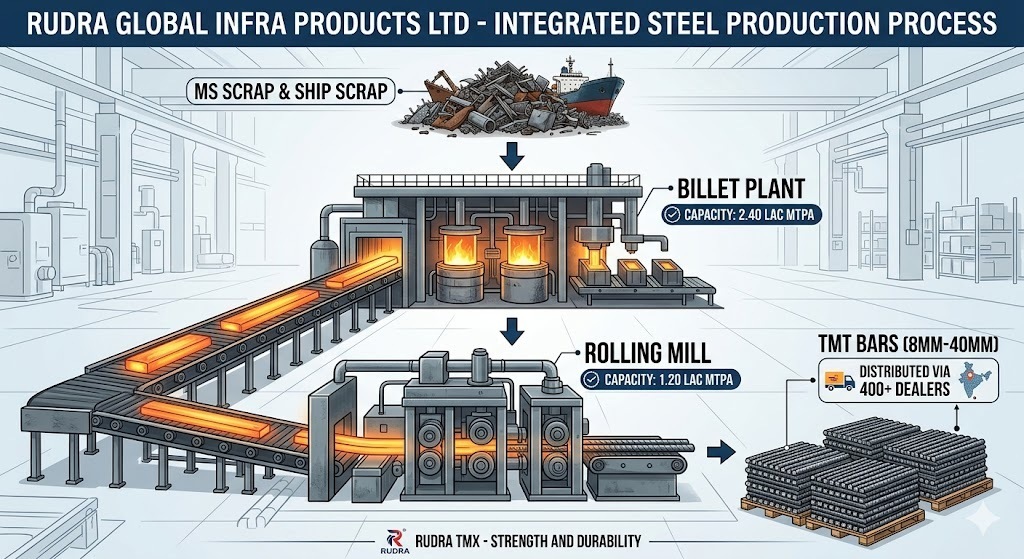

Rudra Global Infra Products Limited (formerly known as MD Inducto Cast Limited) operates out of the manufacturing heartland of Bhavnagar, Gujarat. Over the last decade, the corporate strategy has shifted from a basic induction furnace setup to an integrated forward-rolled TMT bar infrastructure. To the untrained eye, moving up the value chain from molten metal billets to structural steel sounds like a corporate promotion. In practice, it means the company has simply found larger, more complex ways to process industrial scrap metal under tight margins.

The operational nerve center rests near the Alang Ship Breaking Yard, giving the plant a clear logistical advantage in securing scrap steel at short notice. Over the years, management has built an expansive local distribution channel to push its regional retail brands. Yet, despite transforming structural scrap into heavy-duty reinforcement bars for tier-one infrastructure clients, the business runs on the financial equivalent of a high-wire act—where massive trade volumes are regularly deployed to chase single-digit absolute returns.

Section 3 — Business Model: WTF Do They Even Do?

Rudra Global’s business model can be summarized as an industrial alchemy experiment: taking old, discarded ship hulls and industrial scrap metal, melting them down via induction furnaces into billets, and rolling them into corporate-branded TMT steel bars.

They market these products under names like Rudra TMX, JB 500 TMX, and Tridev TMX, promising corrosion-free structural integrity to elite infrastructure giants like L&T, Reliance Industries, and Adani. They have even set up dedicated retail outlets branded as Rudra Inframart to control the direct-to-builder distribution loop.

The corporate revenue split reveals an extreme concentration of focus: manufactured goods contribute 99% of total operating income, with TMT bars taking up 94% of that pie. Essentially, they are a single-product engine operating at the absolute mercy of localized construction activity. It is a high-volume, low-differentiation business where your product is buried under metric tons of concrete, and your pricing power is practically non-existent.

Section 4 — Financials Overview

Figures are standalone, in ₹ crore.

Headline Performance Table

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue

₹178.26

6.61%

12.40%

EBITDA / Operating Profit

₹5.72

-50.77%

-61.12%

PAT

₹1.03

-84.92%

-89.55%

Reported EPS

₹0.10

-85.29%

-89.80%

The sequential breakdown of the final quarter of FY26 reveals severe margin contraction.