Brand Concepts FY26: The Premium Price of Playing the Price Game

Section 1 — At a Glance

A bruising multi-front capital war, compressed pricing power, and an ambitious asset-heavy pivot define the current state of affairs at Brand Concepts Limited. For a company that built its modern reputation scaling highly aspirational global lifestyle licenses across the domestic market, the fiscal year ended March 31, 2026, delivered a sharp, quantitative reality check. Topline momentum remained visibly resilient, with annual sales climbing 19.23% to reach ₹348.07 crore. However, the institutional cost of buying that growth came at the direct expense of structural earnings quality. Full-year net profit cratered by 81.45%, collapsing from ₹5.23 crore in the prior fiscal year to a razor-thin ₹0.97 crore.

This dramatic earnings divergence traces cleanly to a deliberate, high-stakes manufacturing expansion that collided head-on with hyper-aggressive category discounting from heavily funded direct-to-consumer entrants. While headline gross margins expanded under the influence of backward-integrated production, operating inefficiencies and an elevated structural fixed-cost framework effectively consumed the benefits. Simultaneously, the balance sheet underwent a rapid, debt-fueled expansion, with total borrowings ballooning to ₹181.56 crore. This capital deployment elongated the company’s cash conversion cycle and severely compressed interest coverage thresholds. A business model’s ultimate viability is determined not by the sheer volume of assets it manages, but by the incremental economic returns those assets generate over their true cost of capital. Investors are left assessing whether this operational bottoming out represents a temporary transition or a structural reset.

Section 2 — Introduction

Brand Concepts Limited operates at the intersection of fashion merchandising and domestic travel asset retail. Strategically pivoting from its historical roots as a pure-play distributor and retail house, the company has transformed into an omni-channel fashion entity focused on travel gear, small leather goods, and women’s handbags. The operational core of the enterprise relies heavily on an exclusive, multi-brand licensing model, bringing prominent international labels to middle-class consumer segments. Recently, management initiated a massive structural transformation, setting up a capital-intensive manufacturing ecosystem designed to bring luggage production entirely in-house. This pivot from a lean, variable-cost distribution agency to a vertically integrated capital asset owner represents a structural shift that fundamentally rewrites the financial profiles, risk parameters, and balance sheet mechanics of the organization.

Section 3 — Business Model: WTF Do They Even Do?

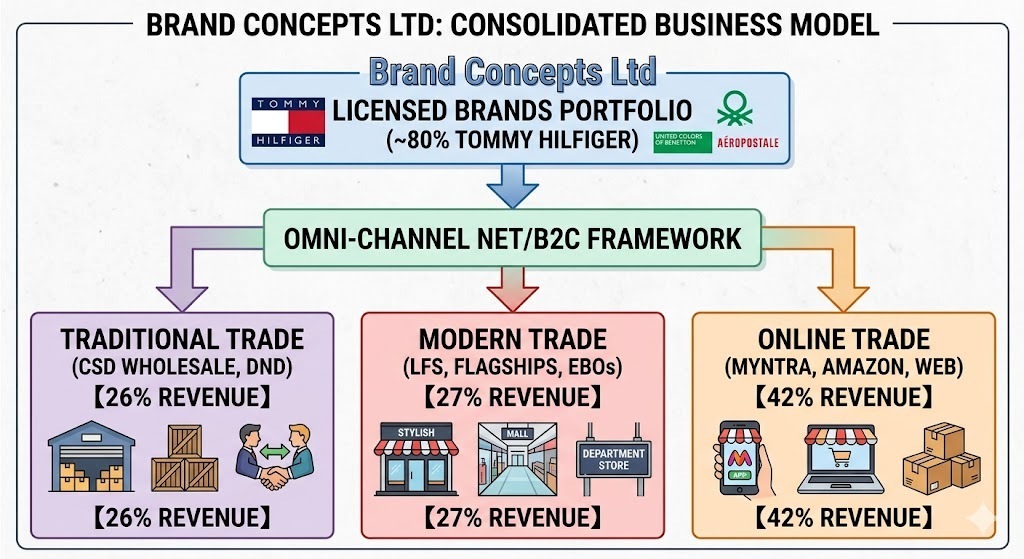

If you strip away the sleek retail frontage and premium mall lighting, Brand Concepts is essentially a high-end corporate renter of prestigious international brand equity. The company operates by acquiring long-term exclusive licenses to manufacture and retail travel gear and accessories for major global brands.

Their current economic existence is heavily dependent on single-source brand romance. The flagship license, Tommy Hilfiger, single-handedly generates roughly 75% to 80% of total organization revenues. The rest of the portfolio is a mixed bag of premium and mass labels, including United Colors of Benetton, Aeropostale, and the newly acquired Juicy Couture and Superdry licenses. They distribute this licensed gear through an omni-channel maze of 56 exclusive brand outlets, large format department stores, traditional wholesale dealers, and high-volume online e-commerce platforms.

To break this extreme concentration on Tommy Hilfiger, management built a massive, 350,000 square foot manufacturing plant in Ujjain to crank out hard and soft luggage. The strategic thesis was elegant: manufacture your own inventory, capture a massive manufacturing margin, and feed it through your own retail channels. Instead, the factory opened just in time to watch a horde of venture-capital-backed luggage startups dump hundreds of crores into digital marketing and price wars.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore. (Note: Data Sheet P&L items reflect standalone reporting, which tracks the consolidated core operational reality of the merged entities ).

Quarterly Financial Performance

Metric

Latest Quarter (Mar 2026)

YoY

QoQ

Revenue

₹90.42

35.66%

2.37%

EBITDA / Operating Profit

₹8.06

35.92%

24.00%

PAT

₹0.77

-60.31%

20.31%

EPS (Reported)

₹0.62

-64.37%

21.57%

Topline execution in the fourth quarter looks excellent on paper, jumping 35.66% year-on-year to ₹90.42 crore. Operating profits kept pace, moving up to ₹8.06 crore. Yet, when you travel down the P&L elevator to the net profit basement, there is barely anyone left alive. Net profit for the quarter dropped to a trivial ₹0.77 crore