Hemisphere Properties India Ltd Mar 2026: The ₹4,074 Crore Landlord with ₹0.99 Crore of Sales

Section 1 — At a Glance

A market capitalization of ₹4,074 crore backed by an annual revenue of precisely ₹0.99 crore presents one of the most polarizing valuation disconnects on the public bourses. Hemisphere Properties India Limited does not operate a traditional business; it is a corporate vessel designed with the singular mandate to hold, protect, and eventually monetize 740 acres of surplus land left behind from the historical disinvestment of Videsh Sanchar Nigam Limited. This unique mandate means the historical financial statements represent a multi-year archive of operational losses, rising administrative costs, and compounding finance charges rather than active commercial execution. Investors have historically piled into the counter looking entirely at the astronomical fair value of its real estate portfolio, which independent valuers peg at over ₹10,588 crore. However, the operational reality features deep legal entanglements, multi-state stamp duty disputes, and an absolute lack of core operating cash flows. The tension between the slow-moving wheels of government land monetization and the rapid-fire speculation of the equity market has reached a critical boiling point. For years, the story was entirely academic—a theoretical exercise in net asset value calculations. But the final quarter of the financial year ended March 31, 2026, has completely flipped the script, transforming a stagnant asset-play into an active, high-stakes corporate drama.

Section 2 — Introduction

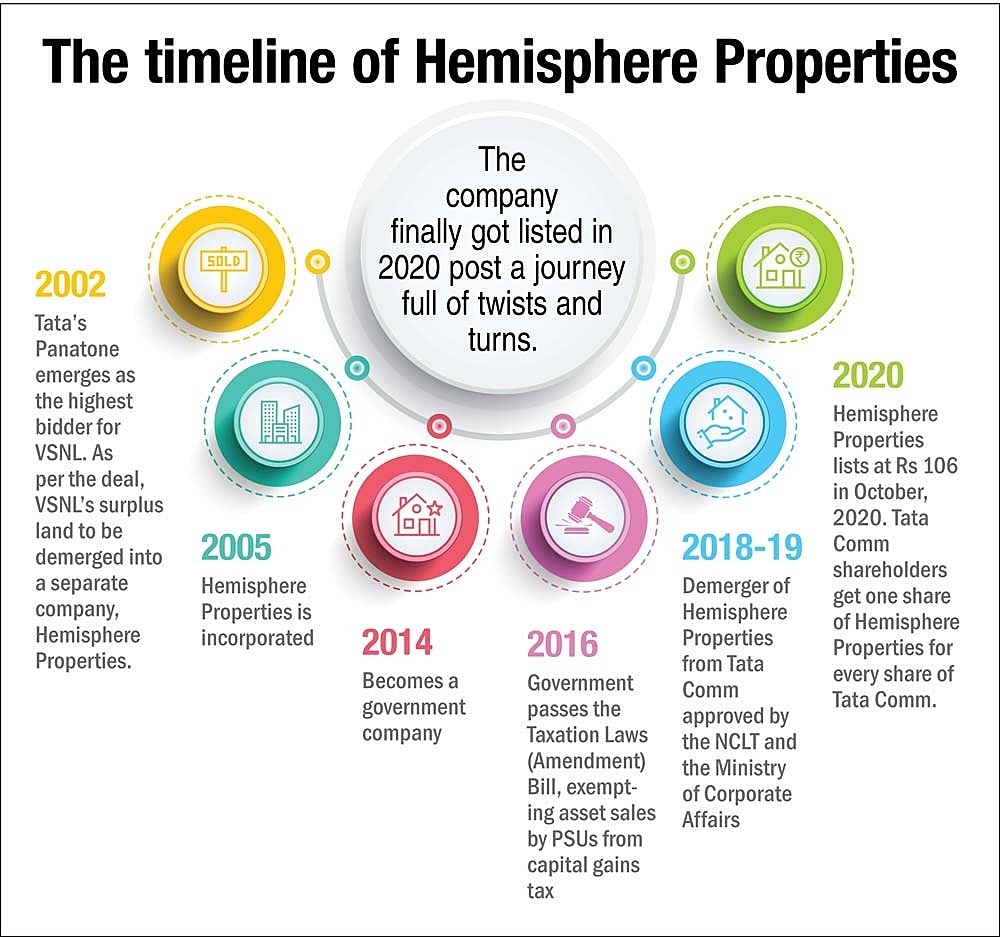

Welcome to the wild world of corporate spin-offs, where assets are massive, operations are non-existent, and the accounting entries read like a cry for help. Originally incorporated in 2005, Hemisphere Properties was handed a golden goose that was locked inside a bureaucratic safe. When Tata Communications took over VSNL, these pristine parcels of land in Delhi, Pune, Chennai, and Kolkata were separated to protect public interest. Fast forward over two decades, and the company acts less like a real estate developer and more like a glorified security guard defending premium pin codes from encroachments and litigation.

Section 3 — Business Model: WTF Do They Even Do?

If you are looking for a business model involving raw material procurement, assembly lines, or a sales force, you are looking in the wrong place. Hemisphere Properties does exactly one thing: it sits on dirt. Specifically, it sits on 739.69 acres of prime urban land across India. The portfolio is dominated by a massive 524-acre spread in Pune (Dighi/Bopkhel), complemented by ultra-premium locations like Greater Kailash (69.46 acres) and Chattarpur (58 acres) in New Delhi, alongside chunks in Chennai and Kolkata. How do they monetize this? Historically, they don’t. Their entire “revenue from operations” consists of tiny pockets of rental income. With a grand total of 5 full-time employees listed in their recent organizational data, this isn’t a company; it’s a legal filing cabinet with a stock ticker attached.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Mar 2026)

YoY

QoQ

Revenue

0.26

8.33%

0.00%

EBITDA / Operating Profit

-2.34

-65.94%

0.85%

PAT

-1.72

60.55%

46.85%

EPS

-0.06

60.00%

45.45%

The income statement is a minimalist masterpiece. Revenue for the quarter stood at ₹0.26 crore, matching the previous quarter and slightly edging past the ₹0.24 crore from March 2025. Meanwhile, quarterly operating profit remains deeply negative at -₹2.34 crore, because even when you don’t build anything, the lawyers and security personnel still send invoices. A negative operating profit paired with interest expenses of ₹2.34 crore for the quarter guarantees a bottom-line bleed, yielding a net loss of ₹1.72 crore. Earnings quality here isn’t a measure of operational efficiency; it is an annual countdown of how much capital is consumed to keep the lights on while waiting for an auction.

Management did not host an elaborate conference call to discuss operational leverage or distribution channels, because there are none. However, in their statutory reporting disclosures, the message from the leadership remains completely focused on regulatory clearances and structural monetization rather than quarterly earnings metrics.

Section 5 — Valuation Discussion: Fair Value Range Only

Valuing this corporate shell using standard trailing multipliers is an exercise in futility, as there are no positive operational