Jubilant Foodworks Ltd FY26: The ₹9,513 Crore Pizza Party with a Very Heavy Debt Delivery

The market’s relationship with India’s premier pizza provider has officially entered a state of profound confusion. For twelve months straight, the headline numbers screamed breakneck expansion, powered by the massive consolidation of a sprawling Eurasian empire. Yet under the hood of this delivery vehicle, a different narrative is taking shape. While the top-line crossed historic thresholds, the business has systematically replaced its once-celebrated cash pile with thousands of crores of borrowings. Investors are left weighing an aggressive multi-brand food-tech infrastructure against a return profile that remains structurally diluted by international execution risks and intensifying competitive friction on the home front.

Introduction

Jubilant Foodworks Limited (JFL) occupies a unique, hyper-visible position in the Indian consumer landscape. As part of the Jubilant Bhartia Group, it has historically operated as an absolute powerhouse of food service execution, scaling the iconic Domino’s Pizza franchise across multiple geographies. Over the last few years, the corporate playbook has shifted dramatically. No longer content with just being India’s neighborhood pizza kitchen, management has embarked on an ambitious corporate transformation—aggressively stacking international master franchises, rolling out premium fried chicken chains, and building heavy tech infrastructure designed to automate the food industry.

Business Model: WTF Do They Even Do?

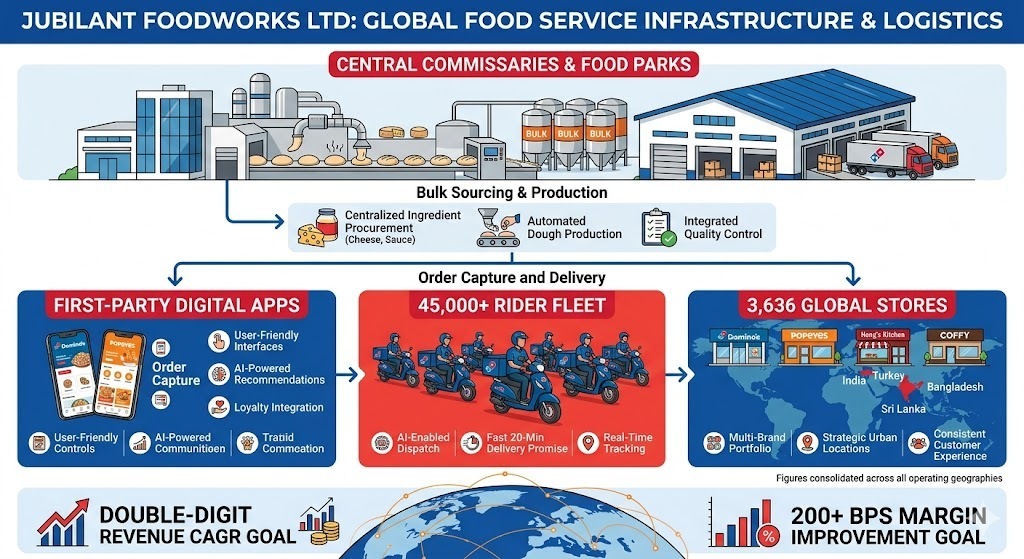

At its core, Jubilant is a master assembly line masquerading as a quick-service restaurant. The architecture relies on an integrated supply-chain network of 8 massive domestic commissaries and food parks that centralize everything from dough-ball production to bulk cheese procurement. This setup feeds a vast, fast-moving retail footprint.

The brand portfolio is handled like an ambitious, slightly chaotic investment basket:

Domino’s Pizza: The absolute cash cow, holding exclusive rights across India, Sri Lanka, Bangladesh, Turkey, and adjacent territories.

Popeyes: The shiny new engine brought in to challenge global fried chicken incumbents in India.

Dunkin’ & Hong’s Kitchen: A slow-burning mix of Western coffee-and-doughnut retail and homegrown Indo-Chinese quick service.

COFFY: A hyper-frequency Turkish café play picked up during recent overseas acquisitions.

Orders are captured predominantly via a proprietary digital app infrastructure and rushed out by a delivery fleet of 45,000+ riders. It is an asset-heavy tech-enabled distribution game where keeping ovens hot and delivery times under 20 minutes is the only metric that keeps the lights on.

Financials Overview

Figures are consolidated, in ₹ crore.

Metric

Latest Quarter (Q4FY26)

YoY

QoQ

Revenue

₹2,499.47

+19.31%

+2.89%

EBITDA / Operating Profit

₹484.90

+23.73%

+0.22%

PAT

₹93.60

+67.31%

-6.68%

EPS

₹1.42

+42.00%

-14.80%

The top-line momentum remains remarkably resilient, maintaining double-digit annual velocity as the international footprints fully kick into the consolidated numbers.

When a consumer company’s structural earnings power can grow volumes by double digits over high historic bases, the fundamental distribution engine is clearly firing correctly.

What is Management Promising in the Coming Quarters?

During the latest earnings deliberations, management outline a highly specific execution framework. The key operating targets include delivering a double-digit revenue CAGR through FY28, which will be unlocked by scaling the domestic Domino’s footprint past the 3,000-store milestone. Furthermore, leadership specified that the business is modeling a 200+ basis point operating margin expansion relative to FY24 baselines, driven by a systematic reduction in the profitability drag from emerging brands.

For the Popeyes vertical, management expects the chain to evolve into a ₹1,000 crore business operating 250 highly profitable outlets over the medium term. Crucially, they noted that the heavy international debt inside the Netherlands holding structure is now entirely insulated from the Indian balance sheet, self-servicing its obligations through standalone Turkish cash generations.

Valuation Discussion: Fair Value Range Only

To evaluate the current pricing paradigm, we pull the key parameters directly from the data spine. With a Current Market Price (CMP) of ₹429.75 and an outstanding base of 65.98 crore adjusted equity shares, the public markets value the enterprise at ₹28,356.91 crore. The fully reported Net Profit for FY26 stands at ₹428.48 crore, translating to a full-year reported EPS of ₹6.49. This places the