Share India Securities Ltd Mar 2026 : The Prop-Trading Paradox of a 283% EPS Surge and Flat Annual Profits

Section 1 — At a Glance

Operating at the intersection of quantitative algorithmic architecture and traditional capital market intermediation, Share India Securities Ltd presents a striking financial dichotomy. In its latest performance print, the group posted an exceptional quarterly diluted EPS expansion of 283.8% YoY, reaching ₹2.61 for Q4 FY26. Yet, this late-stage surge masks a broader structural deceleration across the full fiscal cycle. Full-year consolidated revenue stood virtually flat at ₹1,470.26 crore, representing a marginal 1.5% YoY growth, while annual profit after tax contracted by 1.1% YoY to ₹324.40 crore.

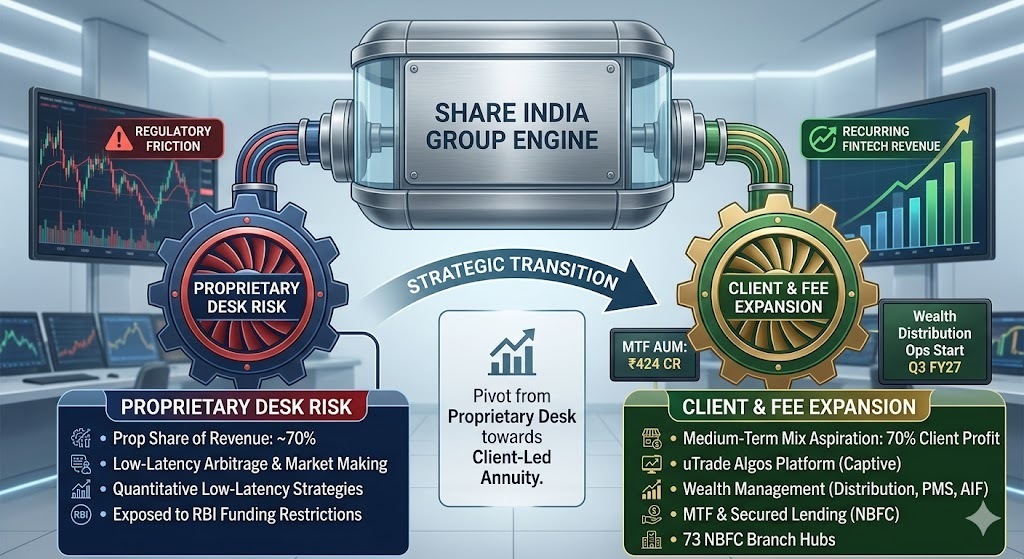

The primary catalyst captivating investor interest is management’s aggressive structural pivot away from proprietary desk risk toward high-margin, scalable retail tech subscriptions and wealth management verticals. This transition is anchored by the uTrade Algos platform, which saw its paid user base consolidate at 5,231 subscribers. Concurrently, significant headwinds are emerging from regulatory tightening. Severe restrictions on bank intraday funding limits for proprietary accounts have introduced structural friction, impacting roughly 20% of the group’s operational deposit frameworks. Furthermore, persistent bottom-line volatility is exacerbated by fair value mark-to-market adjustments on corporate treasury holdings.

Extraordinary sequential performance must always be validated against long-cycle annual run rates to ensure that operational realities have not been obscured by short-term trading tailwinds.

The core question looming over the asset is whether Share India can build a recurring fintech software and lending annuity fast enough to outrun the systemic regulatory squeeze targeting its core prop-desk engine.

Section 2 — Introduction

Share India Securities Ltd has charted an aggressive evolutionary path from an unlisted traditional brokerage operation incorporated in 1994 into a highly automated, algorithmically driven fintech conglomerate. Over three decades, the corporate framework has structurally integrated equity broking, automated high-frequency proprietary trading infrastructure, commodity derivatives handling, and a fast-expanding secured lending book under its non-banking financial company (NBFC) arm, Share India Fincap Private Limited.

This deep dive is necessitated by a massive regulatory inflection point characterizing the close of the 2026 fiscal period. The Reserve Bank of India has actively constrained bank exposures to proprietary trading desks, effectively dismantling historical intraday limit systems across capital markets. At the same time, Share India is deep within a corporate transformation—manifested through its pending National Company Law Tribunal (NCLT) merger with high-frequency trading firm Silverleaf Capital Services and the active rollout of asset management platforms. This analysis deconstructs the underlying quality of its earnings mix, balance sheet liquidity buffers, and the true executable horizon of its multi-product pivot.

Section 3 — Business Model: WTF Do They Even Do?

At its core, Share India functions as a dual-engine capital market locomotive. The primary engine—and historical profit driver—is high-volume trading and market-making, which historically accounted for up to 92% of top-line allocations. By leveraging internal tech infrastructure across subsidiaries like Algowire Trading Technologies and uTrade Solutions, the firm deploys quantitative low-latency strategies across exchanges, acting as a structural liquidity provider in equity options and currency derivatives.

The secondary engine is client monetization. The company provides traditional broking and margin trading facility (MTF) infrastructure to high-net-worth individuals and institutional accounts, coupled with secured SME lending via its 73-branch NBFC layout. The current strategic focus is transitioning from a transaction-dependent transactional model to a SaaS-like architecture. Here, retail investors pay subscription fees to utilize pre-packaged quantitative algorithmic strategies on uTrade Algos, while the firm captures sticky net interest margins on funding those exact trades through its internal MTF book.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Table Overview

The group’s recent filing displays high divergence between short-term quarterly operational elasticity and full-year compounding momentum.

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue

415.91

73.7%

11.8%

EBITDA

116.89

123.2%

-25.1%

PAT

57.83

211.3%

-34.7%

EPS (₹)

2.61

283.8%

-35.4%

Note: All quarterly values are sourced from the verified historical filings and match the group’s finalized disclosure structure.

While the YoY quarterly comparison exhibits massive optical expansion—primarily due to a severely depressed base in Q4 FY25—the sequential QoQ performance reveals notable stress, with operating profit down 25.1% and PAT dropping 34.7% relative to the December-ending period.

Structural margin degradation across sequential quarters often exposes the vulnerability of an asset-light financial intermediary when macro volatility overrides core transaction volumes.

Did Management Walk the Talk?

Reviewing guidance against hard execution reveals a mixed scorecard. Management has consistently vocalized an aggressive focus on scaling the client-led Margin Trading Facility (MTF) business to cushion proprietary trading cyclicality. Operationally, they hit their marks here—the MTF AUM scaled up significantly from ₹239.00 crore in FY25 to ₹423.90 crore by the close of March 2026. However, their ambitious multi-broker software integration blueprint for uTrade Algos—which was intended to onboard users from major external broker platforms like Motilal Oswal and Dhan—has been abruptly halted. Regulatory interventions from SEBI