Godawari Power & Ispat Ltd Mar 2026 : Mining Megawattage Triggers 5x Revenue Blueprint

Section 1 — At a Glance

Godawari Power & Ispat Limited (GPIL) has delivered a highly resilient fiscal performance for the year ended March 31, 2026, anchoring consolidated revenue at ₹5,381 crore and achieving a steady consolidated Net Profit of ₹802 crore. Despite a macro backdrop of softening commodity steel realizations across the domestic market, the company optimized its operating metrics to squeeze out an EBITDA of ₹1,253 crore, locking in premium EBITDA and PAT margins of 23% and 15% respectively.

The primary catalyst captivating investor interest is the successful operationalization of the new 2.0 MTPA iron ore pellet plant in December 2025, which scales total pellet capacity to 4.7 MTPA and achieved a 78% capacity utilization rate in its inaugural full quarter. Simultaneously, the receipt of the long-awaited Consent to Operate (CTO) for the Ari Dongri mines has more than doubled captive mining capacity to 6.0 MTPA.

However, near-term caution stems from a recent 10% structural correction in finished steel prices combined with logistical inflation, causing transport costs to swell by ₹200 to ₹250 per ton.

Commodity integration protects margins during industry downcycles, but massive asset expansions require disciplined execution to prevent near-term return dilution.

The market’s long-term gaze is fixed firmly on management’s radical green transformation and downstream value-add roadmap. This includes a ₹900 crore foray into a 0.7 MTPA Cold Rolled Mill (CRM) complex and a bold diversification into a 20 GWh Battery Energy Storage System (BESS) assembly facility.

Section 2 — Introduction

Godawari Power & Ispat Limited has structurally re-engineered its operational identity over the last two decades. Once a standard merchant pellet manufacturer vulnerable to the violent swings of secondary steel markets, the company has transformed into a robust, backward-integrated infrastructure proxy. The recent amalgamation of Godawari Energy Limited into GPIL—sanctioned by the NCLT effective March 23, 2026—further rationalizes the group’s corporate shell architecture.

This analysis evaluates GPIL at a crucial inflection point. Management has simultaneously approved a monumental ₹7,000 crore capital expenditure program for a new 1.0 MTPA blast furnace-route integrated steel plant, while simultaneously advancing cell supply agreements for a multi-gigawatt clean energy infrastructure play. With the stock hovering at ₹284.5 and carrying a market capitalization of ₹19,149 crore, this piece separates secondary industrial cyclicality from structurally sticky cost advantages.

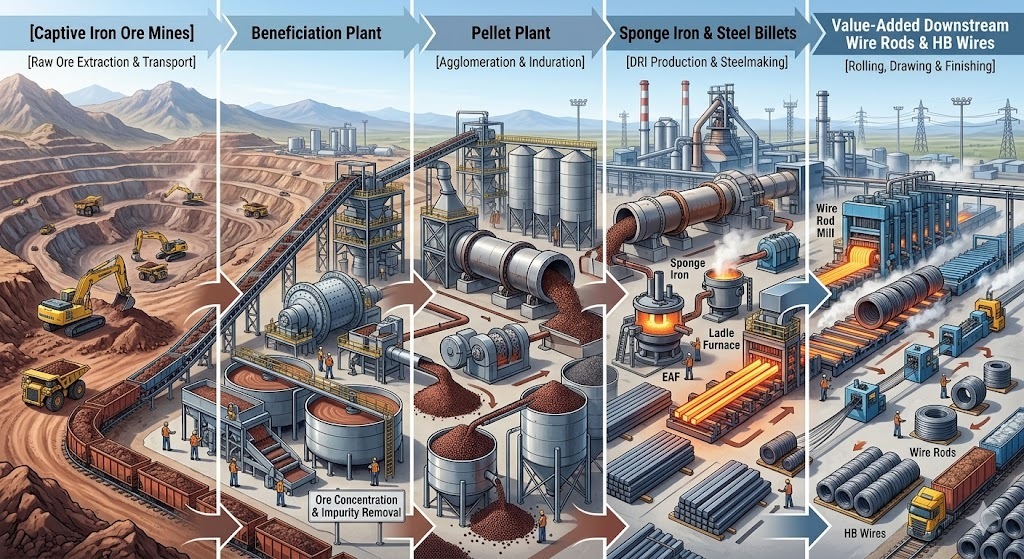

Section 3 — Business Model: WTF Do They Even Do?

At its core, GPIL runs a highly coordinated industrial loop that plays a game of internal margin capture. The business model extracts low-cost iron ore from its 100% owned captive Ari Dongri and Boria Tibu mines, upgrades the low-grade Fe ore via advanced beneficiation plants, and feeds it into proprietary pellet lines.

The resulting high-grade ~65% Fe pellets are either consumed internally to feed sponge iron and steel billet units or sold as premium merchant products. Downstream units then process these billets into mild steel (MS) rounds, hard bright (HB) wires, and galvanized structures.

To eliminate volatile grid dependencies, the company generates power captively through a combination of industrial waste heat recovery systems (WHRP), biomass facilities, and rapidly expanding captive solar farms. This structure leaves GPIL highly insulated, drawing 85% of its raw material requirements internal to its own balance sheet.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Comparison Table

Metric

Latest Quarter (Mar 2026)

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue

₹1,610.27

+9.69%

+41.32%

EBITDA / Operating Profit

₹439.01

+37.86%

+91.43%

PAT

₹280.09

+26.54%

+95.53%

EPS (Reported)

₹4.17

+25.98%

+94.86%

The sequential spike in Q4 FY26 was an absolute blowout, driven by an inventory liquidation masterstroke where 89,000 tons of carryover pellet inventory were sold alongside the initial commercial volumes of the expanded pellet plant.

Volume growth driven by inventory clearing rather than secular price increases delivers excellent near-term cash, but it must not be confused with long-term run-rate realizations.

Did Management Walk the Talk?

Reviewing historical commentary reveals that management delivered precisely on their volume promises. While the first nine months of the fiscal year were severely crippled by an unfortunate accident at the pellet manufacturing plant and a delay in mining environmental