Anthem Biosciences Ltd Q4FY26: Capitalizing on the Big Pharma Pivot as Fixed Asset Base Approaches ₹1,000 Crore

Anthem Biosciences Ltd closed its fiscal year 2025–26 with a decisive operational performance, logging its highest-ever quarterly revenue of ₹610.94 crore in Q4FY26, up 26.44% year-on-year. This surge pushed full-year revenue from operations to ₹2,124.33 crore, marking a 15.17% expansion over FY25’s base of ₹1,844.55 crore. While the headline revenue trajectory underscores a healthy domestic and export appetite, the real substance of the year lies in the structural recalibration of profits: annual Net Profit jumped 31.14% to ₹591.79 crore, unlocking a fat 27.86% margin.

The primary catalyst for this earnings acceleration is an institutional pivot within the core Contract Research, Development, and Manufacturing Organization (CRDMO) segment. Historically reliant on early-stage biotechnology clients whose pipelines are notoriously exposed to macro-funding cycles, Anthem broke new ground in FY26 by onboarding two direct, large-scale pharmaceutical relationships. This institutional anchoring coincided with the final stages of a structural destocking correction across international supply lanes, turning an inventory headwind into a restocking tailwind.

Concurrently, a margin-enhancement initiative materialized at the gross level through the successful backward integration of a critical active pharmaceutical ingredient (API) intermediate. By manufacturing this raw material structure internally rather than sourcing it from volatile external corridors, Anthem boosted its trailing twelve-month Operating Profit Margin (OPM) to 39.24%. However, this operational velocity is colliding with a massive capital expenditure phase. With Unit III freshly fully operational and construction aggressively starting on a ₹1,200 crore Phase 1 rollout at Unit IV, the company is fundamentally altering its asset-turnover mechanics. When a business expands its fixed asset base so drastically, asset efficiency typically dips temporarily before the underlying manufacturing capacity catches up to the structural overheads. Investors are now watching whether this massive capacity wave will be absorbed by long-term big pharma contracts or if it will strain near-term capital efficiency metrics.

Introduction

Anthem Biosciences Ltd is an integrated Contract Research, Development, and Manufacturing Organization (CRDMO) that operates along both the small molecule (chemical) and large molecule (biological) therapeutic value chains. Established in 2006, the corporate model balances a high-end research discovery framework with commercial-scale production, producing advanced intermediates, specialty active ingredients, and active pharmaceutical ingredients (APIs) for global regulated and semi-regulated biological domains.

Following its domestic stock exchange debut on July 21, 2025—which absorbed a ₹3,395.00 crore initial public offering—the company has transitionally stepped into the institutional spotlight. This article evaluates Anthem’s operational positioning in light of its newly published FY26 financial records, detailing the execution parameters of its current custom synthesis and fermentation segments, the structural capacity build across its Karnataka operating sites, and the long-term capital allocation choices shaping its fair value range.

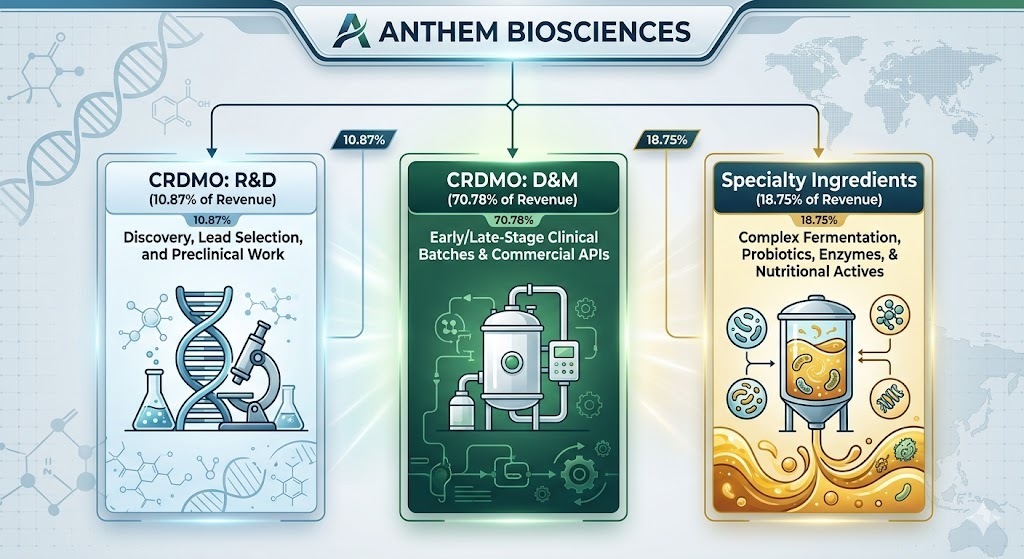

Business Model: WTF Do They Even Do?

Anthem operates a hybrid commercial configuration divided across three functional pillars: Contract Research (R&D), Development & Manufacturing (D&M), and Specialty Ingredients.

The core engines are the CRDMO segments, where R&D feeds early-stage discoveries directly into the commercial Development & Manufacturing (D&M) framework. This structural hand-off allows Anthem to retain long-term manufacturing rights for molecules developed in-house. On the other side, the Specialty Ingredients segment acts as an uncontracted flow business, using proprietary complex fermentation tools to sell nutritional actives, probiotics, enzymes, and premium vitamin analogues directly into the market.

Operational capacity is split between the established Bommasandra facility (Unit I) and the expanding Harohalli hub (Unit II and Unit III). Together, they maintain 425 kL of custom chemical synthesis volume and 142 kL of biological fermentation space. This footprint enables Anthem to concurrently manage over 242 active customer programs spanning complex new modalities like Antibody-Drug Conjugate (ADC) payloads, RNA interference (RNAi) structures, and advanced lipids.

Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Trend

The locked financial architecture for the reporting period is Quarterly Results, Consolidated Basis, in ₹ Crores.

Metric

Q4FY26

YoY (%)

QoQ (%)

Revenue from Operations

610.94

26.44%

44.38%

EBITDA / Operating Profit

267.22

36.90%

69.99%

PAT

189.76

129.68%

104.44%

EPS (₹)

3.38

128.38%

104.85%

Operational Commentary

The fourth quarter of fiscal 2026 registered steep adjustments across the primary operational layers. Quarterly revenue reached a peak of ₹610.94 crore, driven by a 30.72% year-on-year increase in CRDMO orders, which brought in ₹512.80 crore for the quarter. This late-year surge reveals an elementary financial truth: in asset-heavy manufacturing setups, operating leverage can stay