Jay Bharat Maruti Q4 FY26: Dynamic Tax Maneuver and Gujarat State Subsidies Fuel a Massive 333% Surge in Full-Year Profits

Section 1 — At a Glance

Jay Bharat Maruti Ltd (JBML) has delivered an exceptional full-year financial performance for the period ending March 31, 2026, driven by a sharp strategic pivot, lower effective tax provisions, and localized operational support. Annual sales scaled up to ₹2,550.99 crore, indicating a healthy 11.39% growth over the previous fiscal year’s metric of ₹2,290.12 crore. The real fire, however, ignited at the bottom line. Net profit rocketed by 333.58% to hit ₹137.86 crore, compared to just ₹31.80 crore recorded in the preceding fiscal period. This stellar earnings expansion pushed the standalone Earnings Per Share (EPS) up to ₹12.74.

What is captivating investor attention is the company’s dramatic margin turnaround. Operating profit (EBITDA) reached ₹282.78 crore, expanding its operating margin profile significantly to 11.08% from a compressed 7.21% in the prior year. This structural improvement was heavily supported by a massive GST incentive of ₹35.50 crore accrued in Q4 FY26 for its Gujarat J5 plant, coupled with higher capacity utilization. Furthermore, a strategic shift to a concessional tax regime under Section 115BAA triggered a remeasurement of deferred taxes, delivering an immediate one-time balance sheet booster of ₹36.79 crore.

However, underlying anxieties remain centered around extreme client concentration. JBML remains critically tethered to its joint venture partner, Maruti Suzuki India Limited (MSIL), which gobbles up 85% to 90% of total component sales. High capital spending has also kept absolute borrowings elevated at ₹531.21 crore, sustaining an interest burden of ₹43.66 crore.

In the microcap and smallcap arenas, extreme client dependency creates an operational paradox where a single patron fuels both your grandest expansions and your deepest structural vulnerabilities.

The upcoming narrative explores whether this sudden margin expansion is a structural shift or a transient fiscal windfall.

Section 2 — Introduction

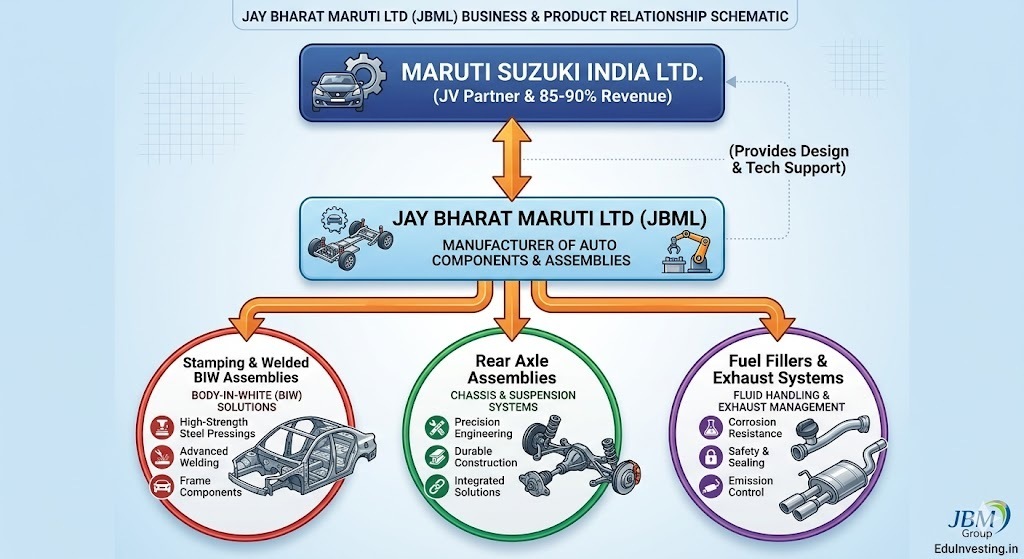

Jay Bharat Maruti Ltd, incorporated in 1987, functions essentially as an extended manufacturing arm of India’s passenger vehicle market leader, Maruti Suzuki India Limited. JBML operates as a specialized joint venture between the Arya family and MSIL, where the automotive giant retains a critical 29.28% equity stake. This analysis emerges at a pivotal moment, as the auto component manufacturer has just wrapped up its final quarter of fiscal year 2026 with a dramatic structural realignment of its tax liabilities and operational execution across its four domestic manufacturing sites.

The company is currently executing massive brownfield and greenfield expansions to mirror MSIL’s upcoming automotive hubs, including major allocations within the vendor park at Kharkhoda, Haryana, and SMG, Gujarat. The investment thesis for JBML is transitioning away from a slow-moving component supplier into an integrated EV-ready sheet-metal chassis partner. This article provides a comprehensive evaluation of its multi-year capital expenditure program, cash conversion dynamics, and standalone valuation framework.

Section 3 — Business Model: WTF Do They Even Do?

To the uninitiated investor, Jay Bharat Maruti might seem like a generic metal stamper, but it actually operates as a highly integrated tier-1 automotive structural partner. The company primarily manufactures Sheet Metal Components, Welded Assemblies, Exhaust Systems, Fuel Fillers, Rear Axle Assemblies, and robust Chassis & Suspension systems. If you are driving a Maruti Suzuki vehicle, there is an incredibly high probability that the underlying Body-in-White (BIW) frame protecting you was engineered, stamped, and welded inside a JBML factory floor.

The operational loop is highly synchronized: MSIL provides revenue visibility and technical tie-ups with Japanese engineering suppliers, while JBML builds plants right next to MSIL’s factories to eliminate logistics friction. Product sales account for roughly 91% of total income, with services contributing 1% and other operating revenues supplying the remaining 8%. It is a high-volume game where factory efficiency and metal yield ratios dictate survival.

Section 4 — Financials Overview

Figures are standalone, in ₹ crore.

The headline performance reveals significant scale expansion across the final quarter of the year, driven by higher localized automotive volumes and state-backed fiscal incentives.