BSL Ltd Q4 FY26 : Debt-Heavy Textile Mills a ₹0.99 Crore Net Loss

Section 1 — At a Glance

BSL Ltd’s full-year performance highlights a steep operational deceleration, characterized by severe margin compression and escalating capital distress. Total operational revenue for FY26 marginally corrected by 1.50% to ₹657.04 crore from ₹667.06 crore in the previous fiscal year. However, structural bottlenecks across core processing segments caused annual EBITDA to slide by 17.4% to ₹49.83 crore, dragging EBITDA margins down by 146 basis points to 7.6%. The bottom line suffered the worst damage, with net profit collapsing by 70.83% to a tiny ₹2.38 crore, down from ₹8.16 crore in FY25. This structural compression was acutely visible in Q4 FY26, as the company plunged into a net loss of ₹0.99 crore, compared to a net profit of ₹2.52 crore in Q4 FY25.

Investor focus is increasingly drawn to BSL’s massive debt burden, with borrowings climbing to ₹439.29 crore against a tiny net worth of ₹119.91 crore. This extreme leverage has pushed the debt-to-equity ratio to an alarming 3.66x. While the recent operationalization of the new cotton fabric unit offers volume support, it has failed to arrest the margin bleed. A company cannot borrow its way to structural profitability when its interest coverage has degraded to just 1.09x. The immediate task for management is navigating this severe capital imbalance before cash reserves completely run dry.

Section 2 — Introduction

BSL Ltd, an established name in the Indian textile landscape since 1971, operates an integrated manufacturing setup spanning spinning, processing, and weaving across poly-viscose, worsted, and cotton segments. The company has spent decades catering to both international buyers and domestic suiting markets, including premium institutional ties like home-furnishing giant IKEA.

Yet, historical pedigree offers zero protection against capital misallocations. BSL recently embarked on an aggressive, debt-led capital expenditure plan to pivot toward cotton spinning and compact ring spinning capacities. This massive layout was expected to diversify revenue streams, but instead, it hit operational reality at the worst possible time. With global supply chains fragmented and high input costs squeezing margins, BSL now finds its entire operating cash flow eaten up by finance costs. This analysis dissects whether BSL can spin its way out of this balance sheet trap, or if the debt will pull it under.

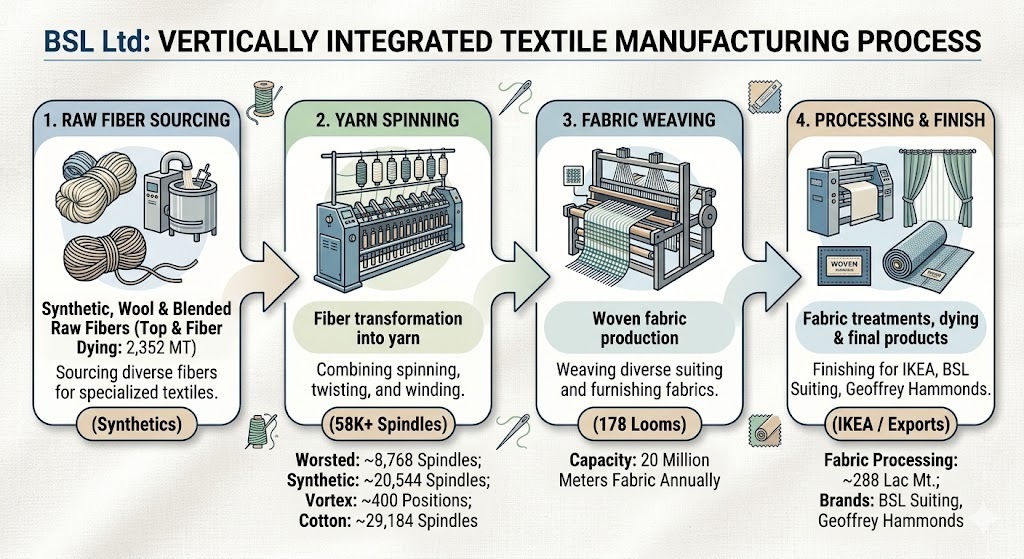

Section 3 — Business Model: WTF Do They Even Do?

At its core, BSL converts raw fiber into premium textiles through three business verticals: Suiting, Furnishing Fabrics, and Yarns. The company operates 178 looms and over 58,000 combined spindles to manufacture synthetic blended fabrics under its own brand, alongside premium worsted labels like Geoffrey Hammonds.

Historically, its suiting and furnishing segments split domestic and export markets evenly. In late 2025, the company threw its hat into the cotton spinning arena, commissioning a 29,184-spindle compact unit capable of churning out 700 tons of cotton yarn per month. While being vertically integrated sounds impressive on investor slide decks, it also means BSL carries heavy fixed assets, high power costs, and massive working capital dependencies. When demand slows down, these heavy mills continue consuming cash regardless of whether the looms are spinning or sitting idle.