Shankara Buildpro Ltd FY26: The Million-Tonne Heavy Metal Party That Forgot the Cake

Section 1 — At a Glance

Shankara Buildpro Limited’s FY26 performance is a masterclass in brute-force volume expansion masquerading as an asset-light transformation. The company delivered a blistering operational headline, surpassing its internal steel volume target of 1.0 million tonnes to close the fiscal year at 10.16 lakh tonnes. This massive execution push catapulted consolidated revenue from operations by 30% YoY to ₹6,826 crore. Profit after tax followed a similarly steep trajectory, surging 64% YoY to ₹128 crore. However, this explosive growth remains starkly lopsided. While the core steel marketplace thrived on infrastructure spending and aggressive penetration into Western India, the margin-accretive non-steel vertical ran straight into a macroeconomic brick wall, posting a tepid 2% annual revenue growth to ₹606 crore. Investors are heavily cheering the post-demerger return on capital employed, which expanded to a superior 36% for FY26, alongside an improved cash conversion cycle. Yet underneath the headline euphoria lies an operating model tethered tightly to commodity pricing, leaving consolidated EBITDA margins thin at 3.35%. When volume outpaces structural mix improvements, scale acts as a magnifying glass for industry-wide cyclical pain points. The critical puzzle for the market now is whether this spin-off can successfully pivot from low-margin steel trading to high-margin retail solutions before the infrastructure cycle peaks.

Section 2 — Introduction

Shankara Buildpro Limited (SBL) enters the public markets with a fresh ticker but three decades of legacy. Officially incorporated in late 2023 , the entity assumed its current form following a National Company Law Tribunal (NCLT) sanctioned demerger from Shankara Building Products Limited, effective April 1, 2024. SBL was specifically carved out to house the retail-led marketplace and trading business, receiving regulatory approvals for listing on the NSE and BSE in January 2026.

This article exists because SBL’s inaugural full-year financial presentation provides the first unvarnished look at the company’s standalone mechanics, free from the manufacturing drag of its former parent. The listing marks a strategic attempt to command an independent, asset-light retail multiple. However, the timing forces the company to immediately defend its valuation against structural regional policy delays and volatile underlying steel inputs.

Section 3 — Business Model: WTF Do They Even Do?

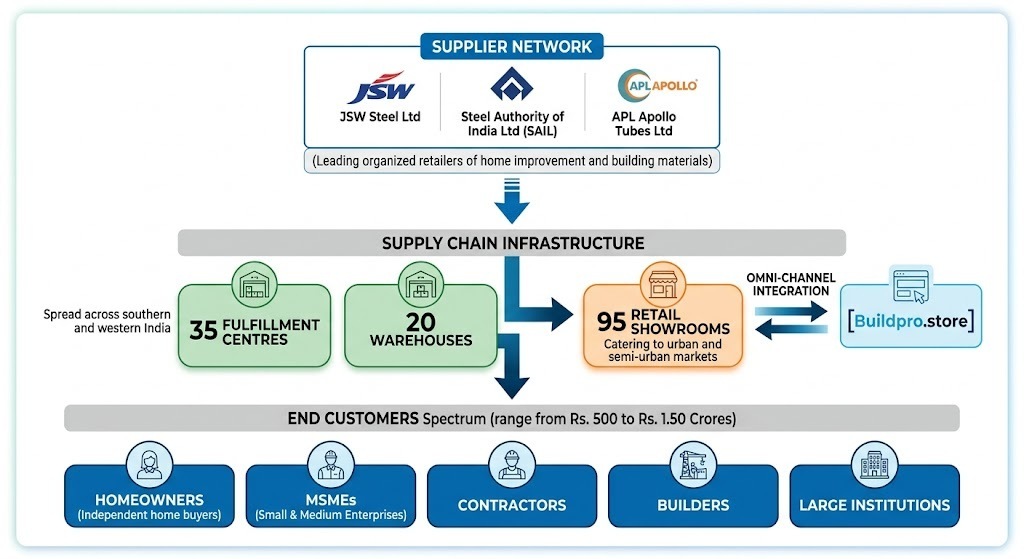

To the uninitiated, Shankara Buildpro looks like a sprawling, highly fragmented B2B middleman. To a smart investor, it is a localized distribution monopoly operating a multi-channel building materials marketplace. SBL bridges the gap between massive primary producers and small-scale buyers by managing a network of 95 operational retail showrooms, 35 fulfillment centers, and 20 warehouses across 10 states and a Union Territory.

The company operates two distinct business universes:

The Steel Vertical: SBL acts as India’s largest distributor of steel pipes and tubes, shifting heavy volumes of structural steel, roofing sheets, and mechanical tubing from giants like JSW Steel and SAIL directly to infrastructure projects and fabricators.

The Non-Steel Vertical: This is the retail dream—selling tiles, sanitaryware, bath fittings (via Kohler, Jaquar, and Cera), and electrical gear to higher-margin retail buyers.

The “omni-channel” pitch is anchored by their digital platform, Buildpro.store, designed to drive online product discovery and subsequent physical store footfalls. SBL essentially monetizes the messy logistics of moving heavy building components to independent home builders, developers, and local dealers.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Table

Metric

Latest Quarter (Mar 2026)

YoY (%)

QoQ (%)

Revenue

1,996.30

27.95%

19.81%

EBITDA / Operating Profit

69.73

48.17%

28.11%

PAT

41.36

41.69%

65.77%

EPS (₹)

17.06

41.69%

65.79%

SBL’s final quarter of FY26 was an absolute blowout in terms of top-line velocity, with quarterly sales kissing the ₹2,000 crore mark. EBITDA margins for the quarter tickled the upper end of historical bounds at 3.51%, expanding by 46 basis points YoY. This margin expansion confirms that when volume scales over fixed warehousing overheads, operational leverage does occasionally show up to work. Rapid top-line growth can easily