SEAMEC Ltd Q4 FY26: The ₹3,299 Million ONGC Lifeline vs The Strait of Hormuz Standoff

Section 1 — At a Glance

SEAMEC Ltd concluded its fiscal year 2026 by logging a consolidated full-year revenue of ₹1,000.00 crore, translating into an emphatic 46.58% top-line expansion against the ₹682.20 crore generated in fiscal 2025. This structural acceleration trickled directly to the bottom line, where consolidated net profit rocketed by 188.40% on-year to land at ₹253.50 crore. Operational performance was heavily augmented by prolonged vessel deployment terms, specifically through the high-yielding, lump-sum contractual setup of SEAMEC III and an multi-platform revamping project.

While headline metrics showcase an unmitigated cyclical boom, the structural realities underlying the asset base command deep investor caution. The operational continuity of the enterprise remains fundamentally lashed to the capital expenditure budgets of a single domestic heavyweight, Oil & Natural Gas Corporation Ltd (ONGC). This asset deployment visibility is simultaneously being threatened by complex geopolitical blockades in West Asia. The SEAMEC Paladin spent the entire fourth quarter completely non-operational and stranded inside a Dubai shipyard, cut off from commercial routes by the closure of the Strait of Hormuz.

Furthermore, technical vulnerabilities continue to induce severe friction across the fleet. Multiple vessels are stumbling into unscheduled technical breakdowns that trigger punitive contractual off-hire periods where the company stops earning.

Supernormal profits generated at the peak of an infrastructure asset cycle frequently mask severe structural vulnerabilities, as fixed asset dependency leaves earnings highly exposed to sudden operational disruptions.

The structural question moving into fiscal 2027 is whether an imminent ₹800 crore fleet-replacement capital expenditure program can successfully substitute aging, breakdown-prone hardware before structural spot-market dynamics reverse.

Section 2 — Introduction

SEAMEC Ltd occupies a highly specialized, capital-intensive corner of the maritime logistics universe, commanding India’s largest domestic fleet of multi-functional Diving Support Vessels (DSVs). Operating under the promoter umbrella of HAL Offshore Ltd—which tightly holds a 72.72% equity stake as of March 2026—the corporate identity of SEAMEC is undergoing a profound structural pivot. Historically restricted to plain-vanilla subsea vessel rentals, the enterprise has aggressively branched out into international dry bulk transportation via maritime hubs in Dubai and deep NATM tunnel engineering infrastructure through its joint venture setup.

The publication of the fourth-quarter financial results marks a defining crossroads for the corporate entity. A revised maritime draft directive issued by the Directorate General of Shipping in May 2025 has temporarily suspended a controversial vessel scrapping mandate. This policy adjustment has effectively reprieved three of SEAMEC’s oldest multi-functional units, allowing assets older than 40 years to escape mandatory disposal and linger on active charter frameworks. However, this regulatory breathing room coincides with an aggressive, debt-leveraged asset acquisition map designed to systematically replace aging marine steel, positioning the balance sheet at a high-stakes transition point.

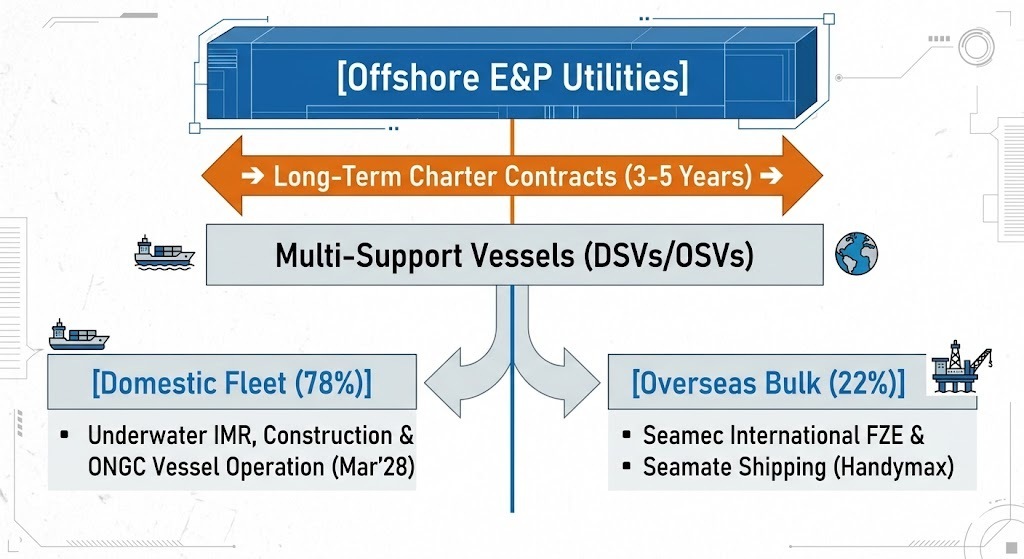

Section 3 — Business Model: WTF Do They Even Do?

To the uninitiated investor, SEAMEC appears to run a typical shipping company, but it actually operates as a high-precision underwater engineering utility. The enterprise owns and leases specialized, heavy-duty marine assets designed to sustain human life and mechanical functionality in volatile offshore deepwater environments. Its fleet comprises six specialized Diving Support Vessels, one Offshore Support Vessel, and a massive accommodation barge. These assets are packed with advanced saturation diving systems, remotely operated vehicle (ROV) deployment bays, and high-capacity industrial firefighting gear.

The core monetization engine relies on charting these vessels out through two distinct commercial mechanisms: long-term engineering charters lasting three to five years, which insulate the top line from oil-price volatility, and short-term spot charters. The primary operational objectives are subsea inspection, maintenance, and repair (IMR) of oil platforms, subsea pipeline placement, and emergency pollution control. The structural business mix is split between domestic operations, which drive 78% of fiscal 2026 revenues, and international dry-bulk cargo movements through two Handymax bulk carriers managed by overseas subsidiaries, contributing the remaining 22%.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Consolidated Quarterly Financial Performance

Metric

Latest Quarter (Q4 FY26)

YoY (%)

QoQ (%)

Revenue

330.40

57.56%

-0.30%

EBITDA

162.40

78.07%

8.12%

PAT

103.70

152.93%

3.91%

EPS (₹)

40.70

152.79%

3.88%

The consolidated top-line momentum achieved during the final quarter highlights an exceptional capacity to command optimal asset pricing during industry upcycles. However, a sequential analysis exposes a flatlining revenue run-rate due to structural friction. While standalone operations were dragged down by a structural impairment charge on its UK investment subsidiary, the consolidation process entirely eliminated this non-cash hit.

What is Management Promising in the Coming Quarters?

During the May 2026 investor briefing, the executive leadership outlined a strictly controlled execution map for fiscal 2027. Management explicitly guided for a conservative 15% expansion across both top-line revenues and bottom-line profitability,