Bharat Parenterals FY26 : The ₹27 Crore Bleed and the USFDA Regulatory Unlock

Section 1 — At a Glance

Bharat Parenterals Limited finished the fiscal year ending March 31, 2026, navigating a complex, structural multi-speed transition. Headline numbers confirm a deep bottom-line squeeze, with the company recording a consolidated net loss of ₹27.3 crore for FY26, despite a marginal topline expansion of 1.5% to ₹345.4 crore. This represents a visible recovery path from the deeper net loss of ₹43.7 crore posted in FY25. The operational heavy lifting was borne by a massive 485.3% surge in consolidated EBITDA, which climbed to ₹15.8 crore, expanding margins to 4.6% from a razor-thin 0.8% in the previous fiscal year.

Investor attention is currently split down the middle. On one side, the group’s premium development engine, Innoxel Lifesciences, completely de-risked its immediate horizon by securing a USFDA Establishment Inspection Report (EIR) alongside an unblemished EU-GMP clearance from Belgium’s FAMHP with zero critical or major observations. On the other side, intense short-term pressure on standalone operations continues to worry the street. Standalone revenues contracted by 23.1% to ₹234 crore as export tenders deferred and critical production lines underwent extensive structural upgrades. High debtor days of 159 days and expanded working capital days at 149 days further compound cash cycle anxieties. Earnings visibility remains structurally tethered to cash burn. Growth cannot be evaluated solely on trailing performance when long-term asset validation temporarily chokes immediate operating efficiency. The upcoming quarters will test whether this massive regulatory unlock translates directly to commercial cash flow.

Section 2 — Introduction

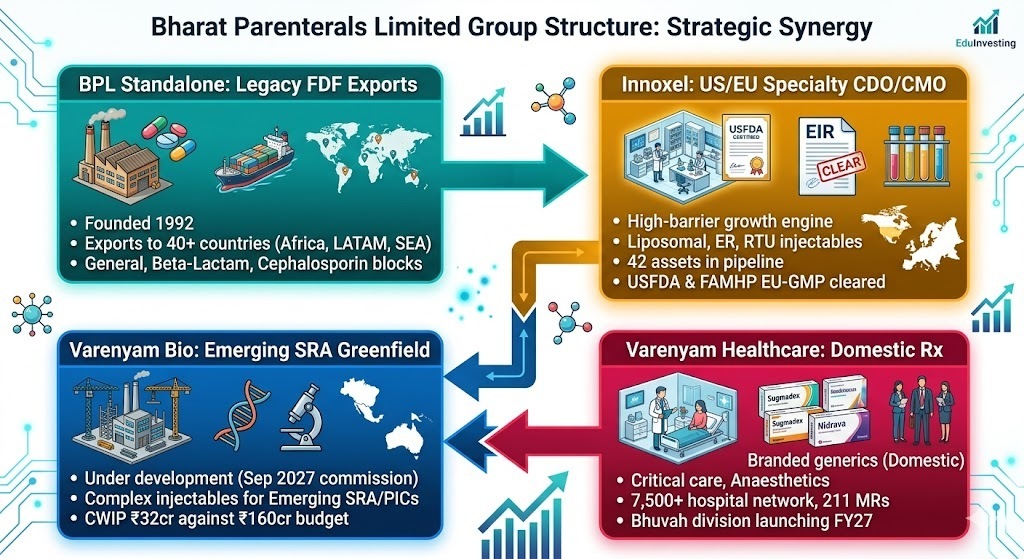

Bharat Parenterals Limited entered FY26 knowing it would be a bridge year, defined by heavy execution across multiple distinct business segments. Established in 1992, the company has historically operated as an export-driven formulation manufacturer focusing on semi-regulated geographies. However, the strategic trajectory has radically pivoted over the last 24 months via aggressive equity expansions and capital deployments into its core subsidiaries: Innoxel Lifesciences, Varenyam Healthcare, and Varenyam Bio Lifesciences.

This article exists today because the market is pricing a dramatic divergence between parent-level operational slowdowns and subsidiary-level regulatory milestones. In June 2024, the board executed a preferential allotment of 3.67 lakh fully paid-up equity shares valued at ₹53.78 crore to consolidate its holdings across the Varenyam ecosystem. These structural integrations have fully exposed the consolidated P&L to the high-depreciation, pre-commercial realities of modern pharma infrastructure investments. With the stock hovering at ₹1,383.95 and trading at nearly three times its book value, this deep dive evaluates if the underlying engine justifies the steep transition premium.

Section 3 — Business Model: WTF Do They Even Do?

At its core, the group operates an integrated pharmaceutical asset model split across four distinct velocity segments:

The parent entity, BPL Standalone, manufactures finished dosage formulations (FDF) across three primary blocks—General, Beta-Lactam, and Cephalosporin—in Vadodara, Gujarat. They produce everything from tablets and capsules to powdered injections, exporting across 40+ countries in LATAM, Africa, and Southeast Asia.

Innoxel Lifesciences serves as the high-margin, regulated-market technology engine. Operating on a 55.9% subsidiary model, Innoxel focuses on complex generics, liposomal formulations, and extended-release injectables targeted directly at the US and Western Europe. Their monetization follows an asset-light, out-licensing rhythm: upfront fees, milestone payments, and subsequent profit splits with generic MNCs.

Varenyam Healthcare drives the domestic branded institutional business, deploying 211 medical representatives targeting over 7,500 major hospital networks with an acute-care anaesthesia and critical care portfolio. Finally, Varenyam Bio Lifesciences is a pre-revenue greenfield platform designed to repurpose Innoxel’s complex IP for non-US regulated markets like Brazil and Australia. It is an intricate web of legacy cash-cow segments funding high-entry-barrier, deep-tech pharmaceutical bets.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Comparison Table

Metric

Latest Quarter (Mar 2026)

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue from Operations

₹99.62 cr

₹103.98 cr (-4.19%)

₹65.19 cr (+52.81%)

EBITDA / Operating Profit

₹(0.52) cr

₹2.23 cr (-123.32%)

₹1.74 cr (-129.89%)

Profit After Tax (PAT)

₹(8.16) cr

₹(9.44) cr (+13.56%)

₹(4.39) cr (-85.88%)

Reported EPS

₹(6.96)

₹(6.86)

₹(6.37)

The sequential trajectory tells a tale of two halves. While the final quarter registered a robust 52.81% top-line sequential bounce to ₹99.62 crore—primarily fed by a massive milestone billing cycle at Innoxel—operating margins collapsed into negative territory due to elevated year-end manufacturing adjustments and personnel costs at the parent level. Top-line numbers fluctuate violently across quarters when revenue recognition relies heavily on lumpy, non-discretionary licensing milestones rather than linear product dispatches.