Uno Minda Ltd Mar 2026 : The ₹3,670 Crore Capital Allocation Odyssey Driving a 52x Earnings Multiple

Section 1 — At a Glance

Uno Minda Limited concluded its fiscal year 2026 by matching industry premiumization shifts with a heavy infrastructure buildout, pushing full-year consolidated revenue to ₹19,589 crore. While headline sales expanded by 17% year-on-year, the financial year was defined by a complex capital allocation strategy. The company is managing a massive ₹3,670 crore multi-year project pipeline, which has pushed its raw debt balance from ₹944 crore in FY22 to ₹2,740 crore by March 2026.

Investor attention is split between two distinct trends. On the positive side, content-per-vehicle expansion continues across key lines, supported by a ₹600 crore annual peak value contract for an Android-based infotainment platform and a ₹450 crore order for two-wheeler lamps. On the negative side, the aggressive debt-funded expansion has altered the balance sheet structure, while domestic electric vehicle registration growth shows near-term softness. Two-wheeler EV penetration pulled back from 7.76% in Q2 FY26 to 5.1% in Q3 FY26, testing the ramp-up velocity of newly built greenfield EV powertrain assets.

Operating profit lines have tracked top-line execution, with full-year adjusted EBITDA reaching ₹2,182 crore. However, heavy execution demands have left a visible mark on asset returns. Adjusted return on equity stood at 18.6% for FY26, down slightly from historical highs as uncommissioned capital expenditure and strategic land bank investments sit in capital employed before generating operations. Valuation multiples remain high; the stock trades at a price-to-earnings multiple of 51.8x, reflecting significant growth expectations embedded by the market.

Section 2 — Introduction

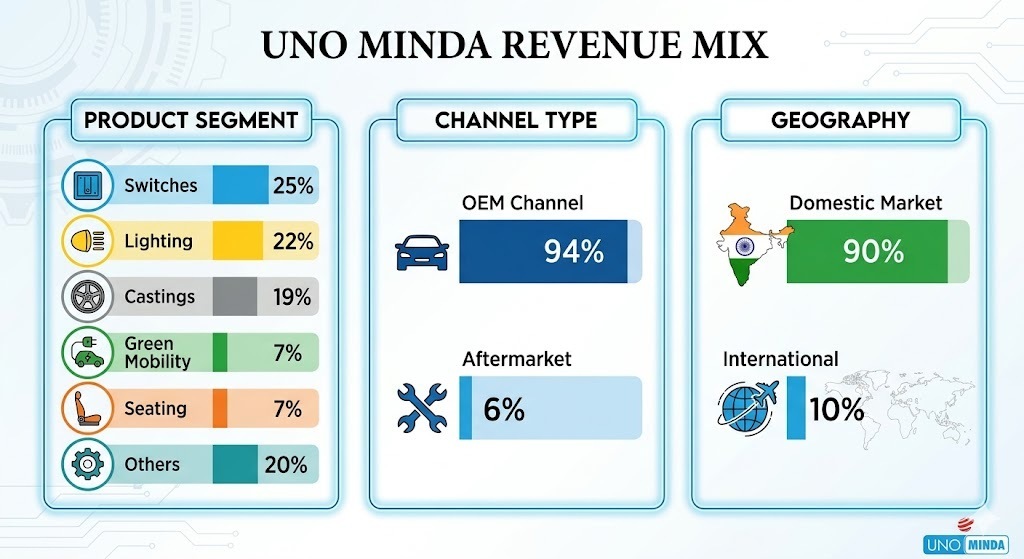

Uno Minda Limited, established in 1958, has transformed from a Tier-1 auto-component supplier into a highly diversified tier-0.5 partner for major automotive global manufacturers. The company’s historic bread-and-butter switches and horn lines have expanded into automated lighting setups, large alloy wheel casting lines, complex seating assemblies, and localized EV powertrain architectures.

The publication of the full-year audited financials for the period ending March 2026 marks an operational transition. Management has initiated an aggressive engineering campaign, running 12 distinct localized and international expansion projects simultaneously. These include setting up a massive 1.8 million wheels-per-annum greenfield alloy factory at Chhatrapati Sambhajinagar and building high-voltage EV powertrain centers in partnership with global technology leaders like Inovance. This article deconstructs whether the current operating metrics justify the company’s aggressive growth premium, or if the rising burden of fixed costs poses a structural risk to near-term profitability.

Section 3 — Business Model: WTF Do They Even Do?

Uno Minda operates a manufacturing framework aimed at capturing maximum wallet share per vehicle hull. The core business relies on proprietary engineering design and deep joint-venture integrations. The company runs 19 separate joint ventures and technical license agreements across various geographies, using localized expertise to manufacture components that are technically insulated from sudden technological disruptions.

The underlying logic is simple: keep the core catalog ICE-EV agnostic. While engine architectures change, the vehicle still requires premium switches, structural seats, complex indicators, and stylized alloy blocks. By systematically increasing potential kit value—which reaches up to ₹22,231 for premium two-wheelers and crosses ₹2,52,878 for top-tier sport utility vehicles—Uno Minda extracts increasing value per vehicle assembly, out-pacing generic automobile volume charts.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Quarterly Performance Analysis

Metric

Latest Quarter (Mar 2026)

YoY (Mar 2025)

QoQ (Dec 2025)

Revenue

5,336

4,528

5,018

EBITDA / Operating Profit

603

527

554

PAT

352

289

300

EPS

5.64

4.64

4.79

Note: PAT and EPS rows in this table represent the net consolidated values before specific promoter non-controlling interest allocations to remain strictly comparable across raw fiscal quarterly filings.

The quarterly numbers show steady volume growth, though operating margins remained bounded at 11.3% due to rising commodity input costs. A major driver was the surge in global aluminum indexing during the fourth quarter, combined with cross-border shipping inflation related to ongoing West Asian logistics friction.

What is Management Promising in the Coming Quarters?

During the latest investor interactions, management outlined clear strategic pathways for the upcoming fiscal years:

Export Pipeline Activation: The business secured a ₹390 crore long-term export commitment for proprietary seating solutions from three global clients. This is backed by a major ₹450 crore annual peak value program for specialized two-wheeler lamps, scheduled for serial production starting