Valiant Organics Limited Q3-FY26: The Turnaround Chemistry Facing A Crucial Structural Test

Section 1 — At a Glance

Valiant Organics Limited entered the final quarter of fiscal 2026 showing signs of a sharp operational pivot, mixed with localized structural headwinds. Headline numbers for the cumulative nine-month period ending December 31, 2025, show consolidated operational revenues stabilizing at ₹521.0 crore, registering a modest 1.2% growth over the ₹514.9 crore recorded in 9M-FY25. However, the real story lies beneath the top-line: operating EBITDA surged by 84.4% year-on-year to ₹61.6 crore, expanding margins by 533 basis points to 11.82%. This was accompanied by a robust turnaround in consolidated net profit to ₹17.5 crore from a painful loss of ₹7.6 crore in the same period last year, demonstrating resilience against persistent industry-wide pricing pressures.

What is Gaining Attention: Market participants are closely tracking the company’s gross profit margin expansion, which climbed by over 500 basis points to 43% in 9M-FY26. This recovery has been anchored by improved raw-material efficiencies, a stronger domestic mix, and an exceptional insurance claim collection of ₹5.7 crore that boosted the bottom line.

What is Worrying the Market: Severe localized operational friction has checked this momentum. The third quarter alone felt the combined heat of pricing compression and a temporary disruption at the Ahmedabad manufacturing plant following a fire incident, leading to a sequential margin contraction. Long-term working capital intensiveness remains structurally high, with Gross Current Asset days standing at an elevated 162 days.

True operating turnaround is achieved when core asset efficiencies improve, not when exceptional receipts temporarily cushion the bottom line.

The company’s board has simultaneously authorized a thorough evaluation of corporate restructuring options—ranging from mergers to demergers or strategic amalgamations—setting the stage for a major corporate transition.

Section 2 — Introduction

Valiant Organics Limited occupies an essential, yet highly volatile, niche within the Indian specialty chemicals matrix. Established over three decades ago, the business has historically focused on substituting import-dependent industrial chemistries within the domestic supply chain. While the company commands considerable scale across core building blocks, its historical trajectories have been frequently disrupted by environmental compliance interventions, global raw material adjustments, and concentrated structural setups.

The publication of the company’s Q3-FY26 results presents an ideal window for deep fundamental scrutiny. With a current market capitalization of ₹816.49 crore and a snapshot current market price of ₹291.4, Valiant Organics is trading at a critical juncture where operational metrics are attempting to decouple from a multi-year cyclical downturn. This review unpacks the quality of the recent margin recovery, evaluates the structural strength of the balance sheet, dissects segment performance, and looks objectively at the corporate governance and restructuring signals flashing across the executive radar.

Section 3 — Business Model: WTF Do They Even Do?

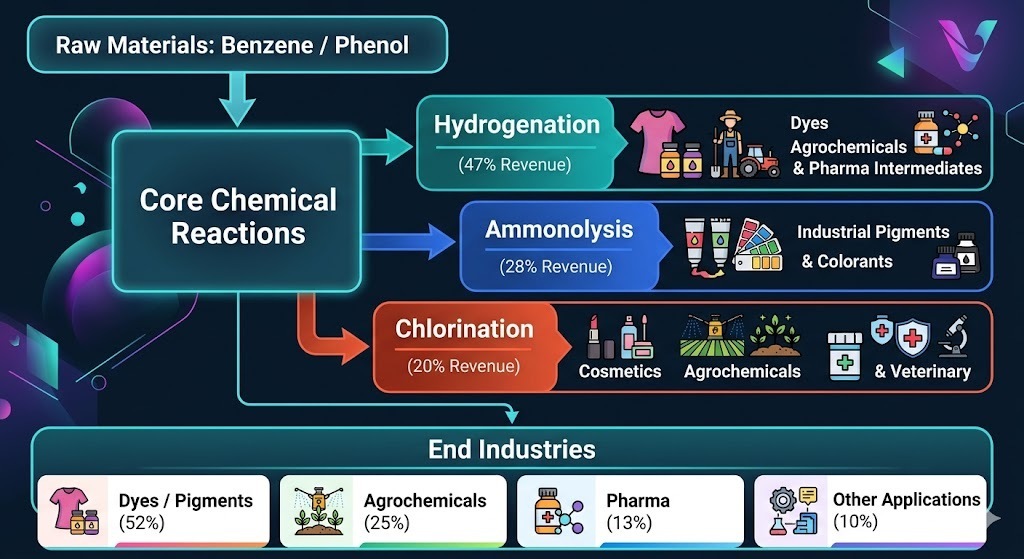

To the uninitiated investor, Valiant Organics looks like an industrial maze of complex chemical reactions. Stripped of the technical jargon, the company manufactures intermediate building blocks that act as the chemical “glue” for several everyday final products.

Operating across six manufacturing units with an aggregate capacity of 70,000 tonnes per annum (TPA), Valiant slices its revenue engine into key chemical buckets. Hydrogenation stands as the largest process block, accounting for 47% of revenue and producing vital elements like Para Amino Phenol (PAP) and Anisidines. Ammonolysis generates 28% of revenue through items like Para Nitro Aniline (PNA) for the dyes sector, while Chlorination drives 20% of the top line, focusing on core chlorophenol derivatives used extensively in agrochemicals, cosmetics, and veterinary applications.

The business operates a classic B2B model, supplying critical inputs to a blue-chip domestic clientele that includes Anupam Rasayan, Lanxess India, and Clariant. Financially, the model is highly sensitive to end-user industry cycles: Dyes and Pigments absorb a massive 52% of output, followed by Agrochemicals at 25% and Pharmaceuticals at 13%. When the international textile and pigment markets hit a wall, Valiant’s volume momentum drops, forcing it to find a balance between volatile industrial commodity cycles and high-margin specialty ingredients.

Section 4 — Financials Overview

Figures are consolidated, in ₹ crore.

Performance Tracking Table

Metric

Latest Quarter (Dec 25)

YoY

QoQ

Revenue from Operations

₹159.30

-14.77%

+1.27%

EBITDA / Operating Profit

₹15.60

+1.30%

-26.42%

PAT

₹3.60

-34.55%

-36.84%

EPS (Reported)

₹1.30

+28.71%

-35.64%

Financial Trend Commentary

The consolidated financial landscape reveals an enterprise wrestling with top-line friction while trying to establish a more efficient baseline. Revenue from operations for the quarter stood at ₹159.30 crore, down 14.77% on a year-on-year basis, impacted by persistent deflationary pricing in global chemistries. Sequentially, revenues stayed flat