Gopal Snacks Ltd Q4 FY26: Revenue Hits All-Time High at ₹1,508 Cr but Fire Recovery Costs & Low Capacity Utilisation Weigh on Margins

1. At a Glance

The Indian snacking industry is a battlefield of flavors and regional dominance, and Gopal Snacks Ltd has long been the king of the “Gathiya” kingdom in Gujarat. However, the financial year 2026 has been a trial by fire—quite literally. While the company has managed to clock its highest-ever annual revenue of ₹1,508.2 crore, gaining massive investor attention for its sheer scale and 950+ distributor reach, the underlying numbers tell a story of a business working overtime just to stand still.

The most glaring red flag isn’t the topline growth; it’s the capacity utilisation, which is currently languishing between 35-40%. Having a massive manufacturing engine is useless if half the cylinders aren’t firing. Furthermore, the Operating Profit Margin (OPM) has taken a severe beating, collapsing from 14% in FY23 to a modest 7% in FY26. Much of this is attributed to the catastrophic fire at the Rajkot facility, which forced the company into expensive third-party manufacturing and logistics realignments.

Investors are watching a dramatic recovery play. On one hand, the company is aggressively expanding into “Focus Markets” like Maharashtra and Rajasthan, showing double-digit growth outside its home turf. On the other hand, it is battling GST demand notices totaling over ₹22 crore and a history of food safety allegations. The reliance on ₹5 price point packets, which account for 65.7% of revenue, makes the business vulnerable to even the slightest fluctuation in palmolein oil or chana prices.

Is the worst over, or is the current valuation of 83.8 P/E simply pricing in a perfection that the operational reality hasn’t yet delivered?

2. Introduction

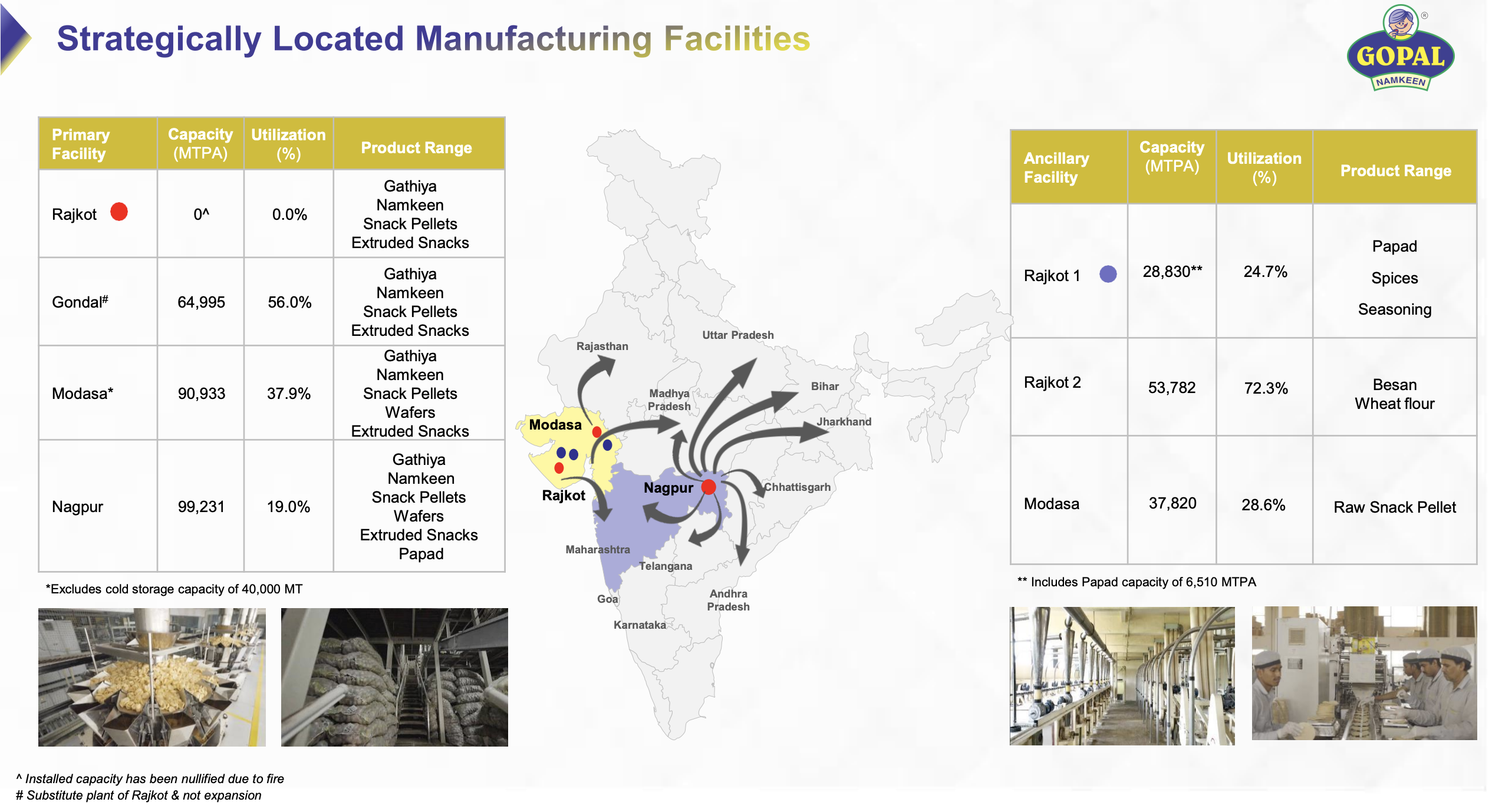

Gopal Snacks Ltd is a powerhouse in the ethnic savories market, originating from the snack hub of Rajkot. Founded in 1999, it has evolved from a small-scale partnership into a vertically integrated FMCG giant listed on the NSE and BSE as of March 2024. The company’s identity is synonymous with Gathiya, a traditional Gujarati snack, where it holds a dominant 31% market share in the organized Indian market.

The business operates on a massive scale, with a total installed capacity of 410,154 MTPA across facilities in Rajkot, Modasa, and Nagpur. Its distribution network is its primary moat, utilizing 294 owned logistics vehicles to service over 953 distributors across 12 states. Despite its national ambitions, the company remains deeply rooted in Gujarat, which accounts for roughly 71% of its revenue.

The recent IPO, which raised ₹650 crore, was entirely an Offer for Sale (OFS), meaning the capital didn’t enter the company’s books but went to selling shareholders. This places the burden of growth entirely on internal accruals and existing debt lines. As the company navigates the post-fire recovery phase, it is shifting its energy toward marketing and branding, spending 1.7% of its revenue on ads to shed its image as a purely regional player.

3. Business Model – WTF Do They Even Do?

Gopal Snacks sells “habitual” products. They make things that people buy without thinking twice while standing at a local “Pan-beedi” shop or a grocery store. Their business is built on the “Power of Five”—the ₹5 packet. By catering to the massive lower-and-middle-income demographic, they ensure high volume, even if the margins are razor-thin.

The Product Hierarchy

The Hero (Gathiya): This is their bread and butter, contributing 27% to the revenue. They aren’t just selling snacks; they are selling a Gujarati staple.

The Namkeen & Western Mix: A mix of traditional snacks and wafers. While Gathiya is the anchor, Namkeen contributes 22% and Wafers 10%.

The Vertical Integration Play: Unlike many competitors who outsource, Gopal produces its own spices, seasoning, besan, and even some packaging. They even make their own oil soap from byproduct oil. It’s a “waste-not, want-not” model that helps claw back small percentages of margin.

The Strategy

They use a push-model through a massive distributor network. The “Detective” in us notices that they are now moving to a “Double Coverage” model—servicing outlets twice a week instead of once. This is a classic FMCG move to increase shelf-presence and prevent competitors from filling the gaps.

Is a business that relies on ₹5 coins sustainable when inflation is eating into the weight of the packet?

4. Financials Overview

The latest results show a significant jump in quarterly revenue, but the profitability remains volatile due to “Exceptional Items” related to insurance payouts from the fire incident.

Quarterly Performance Comparison (₹ Crore)

Metric

Latest Quarter (Mar ’26)

Same Qtr Last Year (YoY)

Previous Quarter (QoQ)

Revenue

409.63

317.53 (+29%)

400.82 (+2.2%)

EBITDA

31.50

2.00 (+1475%)

30.40 (+3.6%)

PAT

29.95

-39.50 (Recovery)

15.50 (+93.2%)

EPS (₹)

2.40

-3.17

1.24

Annualised EPS Calculation:

Since the latest result is for Q4 FY26, we use the reported full-year EPS.

FY26 Reported EPS = ₹5.91

Financial Wisdom: High revenue growth is often a vanity metric if not accompanied by stable OPM.