At a Glance

If you’ve ever fumbled in the dark for a flashlight or realized your TV remote is dead at 11 PM, you’ve likely encountered the iconic red cat of Eveready Industries India Ltd (EIIL). But beneath the “Give Me Red” nostalgia lies a company that has spent the last few years looking less like a high-voltage powerhouse and more like a legacy brand trying to find its second wind. The Q4 FY26 results, however, suggest that the wind might finally be catching the sails—or at least, the batteries are finally being replaced.

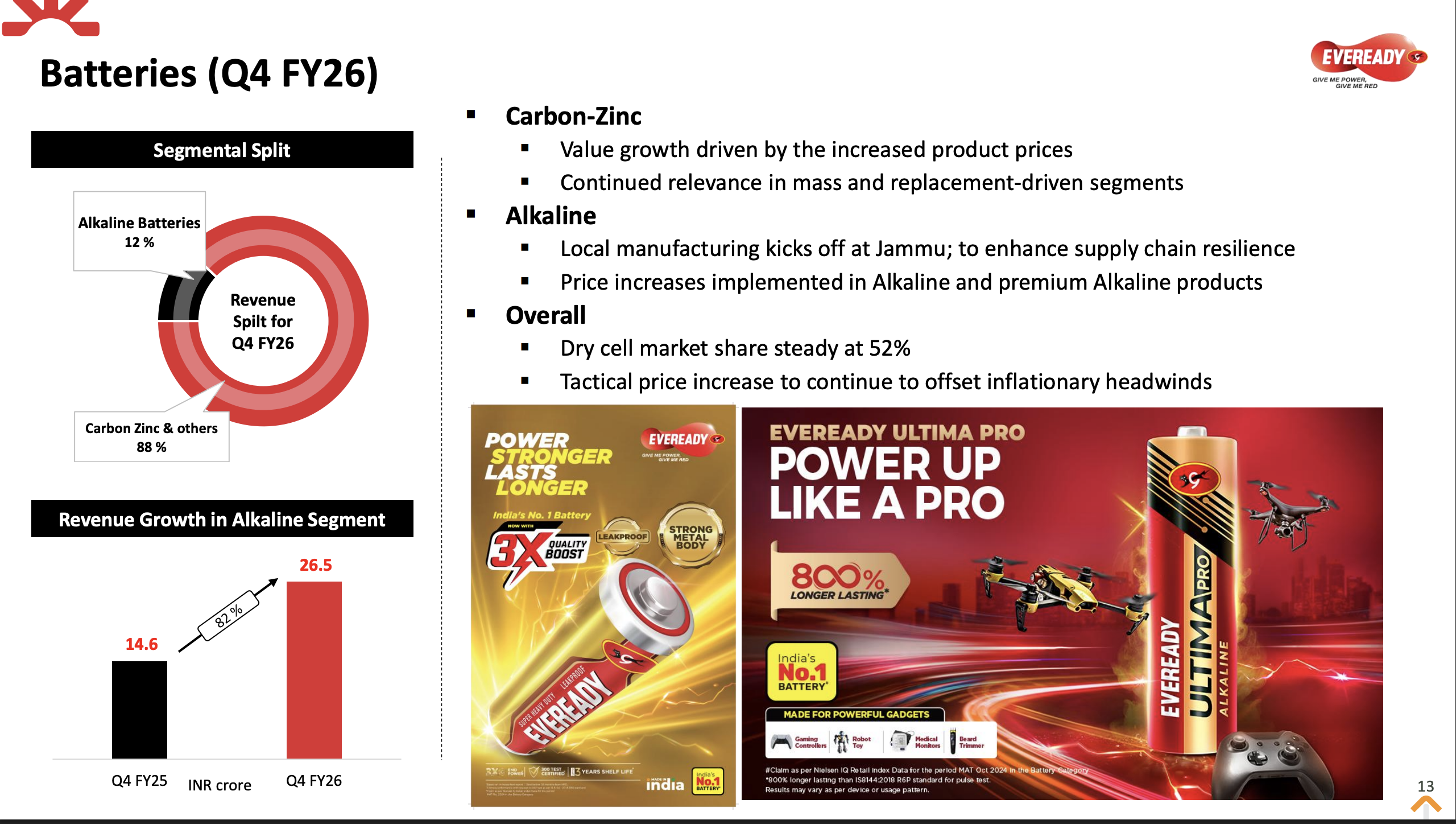

This isn’t just about selling AA batteries to rural households anymore. Eveready is currently undergoing a massive structural transformation. We are looking at a company that has successfully commissioned India’s only dedicated alkaline battery plant in Jammu, a move aimed squarely at taking on cheap Chinese imports and improving margins by a staggering 10% in that segment.

Financially, the headline numbers for Q4 FY26 are enough to make any spreadsheet-loving detective take notice. Net Profit soared by 790% YoY, landing at ₹92.8 crore (consolidated). Before you pop the champagne, it’s worth noting that a significant chunk of this was powered by a “spark” from exceptional items—specifically the ₹105.2 crore gain from the transfer of leasehold rights at their Noida plant.

The real intrigue, however, lies in the balance sheet. Eveready has been on a relentless debt-reduction diet. Net debt has been slashed to ₹178 crore (down from much higher levels in previous years), funded by asset monetization and improved operational efficiency. With the Burman family (of Dabur fame) now firmly at the helm, the “legacy baggage” of inter-corporate deposits and promoter-group debt—which famously saw a ₹489 crore provision in FY21—is being systematically cleared out.

Is Eveready finally moving from a “slow-leak” battery to a high-performance “Ultima” alkaline? The market seems to think so, with the stock trading at a P/E of 16.6, significantly lower than the industry median of nearly 30. But as any detective knows, the devil is in the raw material costs (Zinc and USD volatility) and the competitive intensity of the LED lighting space.

Introduction

Eveready Industries is a centenarian that has seen it all—from the British Raj to the digital revolution. Founded in 1934, it commands a dominant 50%+ market share in the dry cell battery market and over 70% in the organized flashlight market. In India, Eveready isn’t just a brand; it’s the category.

However, being a market leader in a mature category is a double-edged sword. For years, Eveready struggled with stagnant growth and high debt levels associated with its previous promoters (the Khaitan family). The entry of the Burman family via an open offer in 2022 marked a pivotal shift in governance and strategic intent.

The current business focuses on four pillars: Batteries (65% of revenue), Flashlights (12%), Lighting (23%), and small experimental adjacencies like mosquito rackets and mobile accessories. While batteries remain the cash cow, the “cow” is being upgraded from standard Carbon-Zinc to high-margin Alkaline batteries. The recently commissioned Jammu facility is the crown jewel of this strategy, aiming to localize production and insulate the company from currency fluctuations and import dependencies.

The lighting segment, once a drag on margins due to hyper-competition, is seeing a “mix upgrade,” focusing on professional luminaires and emergency LEDs. Meanwhile, the flashlight segment is pivoting toward rechargeables, anticipating a consumer shift away from disposable battery-operated models.

Business Model – WTF Do They Even Do?

They sell “portability.” Whether it’s the energy in a battery, the light in a torch, or the illumination in a bulb, Eveready’s business model is built on one of the most formidable distribution networks in India.

- Batteries: They manufacture and sell over 1.3 billion batteries annually. They are essentially the “toll booth” of the portable electronics world in India.