1. At a Glance – The Curious Case of the Crane King

If Sherlock Holmes were an investor, he’d probably raise an eyebrow at Tara Chand InfraLogistic. On the surface, this company looks like a disciplined, high-margin logistics and equipment rental machine—clocking 37% EBITDA margins, maintaining ~83% utilization, and expanding aggressively with ₹100+ crore capex plans.

But dig a little deeper and things get… interesting.

You’ve got:

- Heavy debt creeping in (₹130 crore borrowings)

- Continuous capex addiction (₹145 crore in FY25, ₹121 crore already in FY26)

- Working capital cycles stretching like Mumbai traffic

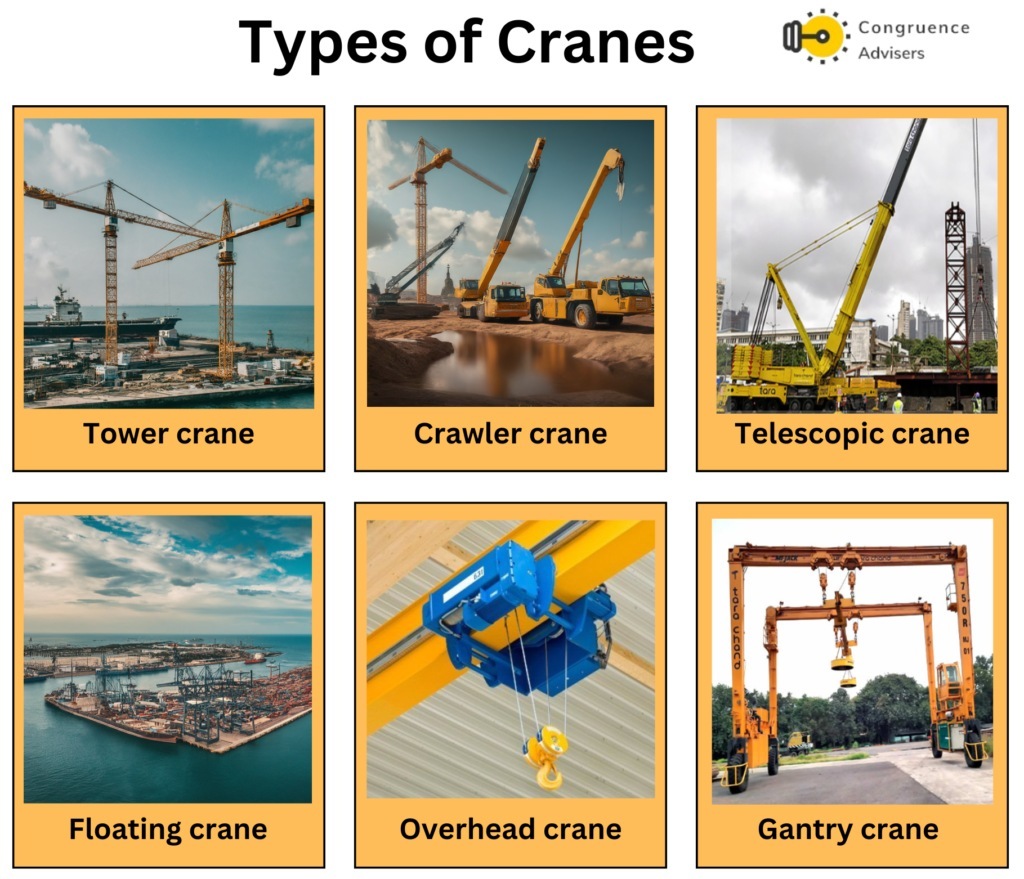

- And a business model that depends heavily on cranes, steel, and infrastructure cycles (basically, the Indian economy’s mood swings)

Yet somehow, despite all this, the company keeps delivering:

- 30% sales growth (TTM)

- 136% profit growth (3-year)

- ROE ~20%

So the big question is:

Is this a well-oiled logistics powerhouse… or just a highly leveraged crane rental company playing musical chairs with infrastructure demand?

Let’s investigate.

2. Introduction – From Steel Godown to Infra Enabler

Tara Chand InfraLogistic Solutions Ltd (TCISL) started in 2012—basically when India was still figuring out whether infrastructure would boom or just remain a PowerPoint dream.

Fast forward to today:

- The company operates across 21 states + Mauritius

- Serves clients like Tata Steel, Reliance, L&T, Vedanta

- Handles 7.21 million metric tonnes of steel (H1FY26)

Sounds impressive, right?

But here’s the twist.

This isn’t just a logistics company.

It’s a weird hybrid of:

- Crane rental business

- Steel logistics operator

- Warehousing company

- Infrastructure execution partner

Basically, it’s like:

“A truck operator who also owns cranes, warehouses, and occasionally behaves like a contractor.”

And that’s where the story gets spicy.

Because hybrid models can either:

- Create massive operating leverage

OR - Become a capital-heavy headache

So ask yourself:

Is this diversification genius… or confusion disguised as