1. At a Glance – The Plastic Drum King Who Forgot Margins Exist

This is one of those companies where everything looks perfect… until you zoom into the profit line and suddenly it feels like a Bollywood movie where the hero disappears in the second half.

Revenue is growing. Capacity is expanding. Big clients are onboard. Solar, recycling, capex, ESG—everything sounds like a LinkedIn influencer post.

But then…

PAT drops 30% YoY.

Margins shrink.

Debt rises.

Interest and depreciation quietly eat profits like relatives at a wedding buffet.

And management?

They’re basically saying:

“Trust us bro, next year will be great.”

Classic.

The real question is:

Is this a genuine operating leverage story about to explode,

or just another capex-heavy midcap stuck in ‘future potential’ mode forever?

Because right now, Pyramid Technoplast looks like:

A company that built the entire factory… but forgot to switch on the profit machine.

2. Introduction – The Industrial Packaging Drama You Didn’t Ask For

Let’s be honest.

Nobody wakes up and says:

“Today I will invest in plastic drums.”

But here we are.

Pyramid Technoplast Ltd is not glamorous. It doesn’t sell EVs, AI, or fintech dreams.

It sells:

- Plastic barrels

- Chemical containers

- Steel drums

Basically, the tiffin boxes of the industrial world.

But here’s the twist…

This boring business:

- Has sticky demand

- Serves chemical giants

- Is linked to industrial growth

- Has recurring replacement demand

So while influencers chase “next multibagger EV startups,”

this company quietly supplies containers to:

- Adani Wilmar

- Asian Paints

- Aarti Industries

Meaning:

If chemicals move, Pyramid earns.

But here’s where the story gets spicy…

They went into:

- Massive capex

- New plants

- Solar investments

- Recycling units

And now…

they’re stuck in that dangerous zone:

“Everything is built… but profits haven’t caught up yet.”

Ever seen a gym membership in January?

That’s Pyramid Technoplast right now.

3. Business Model – WTF Do They Even Do?

Let’s simplify this like you’re explaining to a friend who still thinks EBITDA is a cricket league.

Core Business:

They manufacture industrial packaging products:

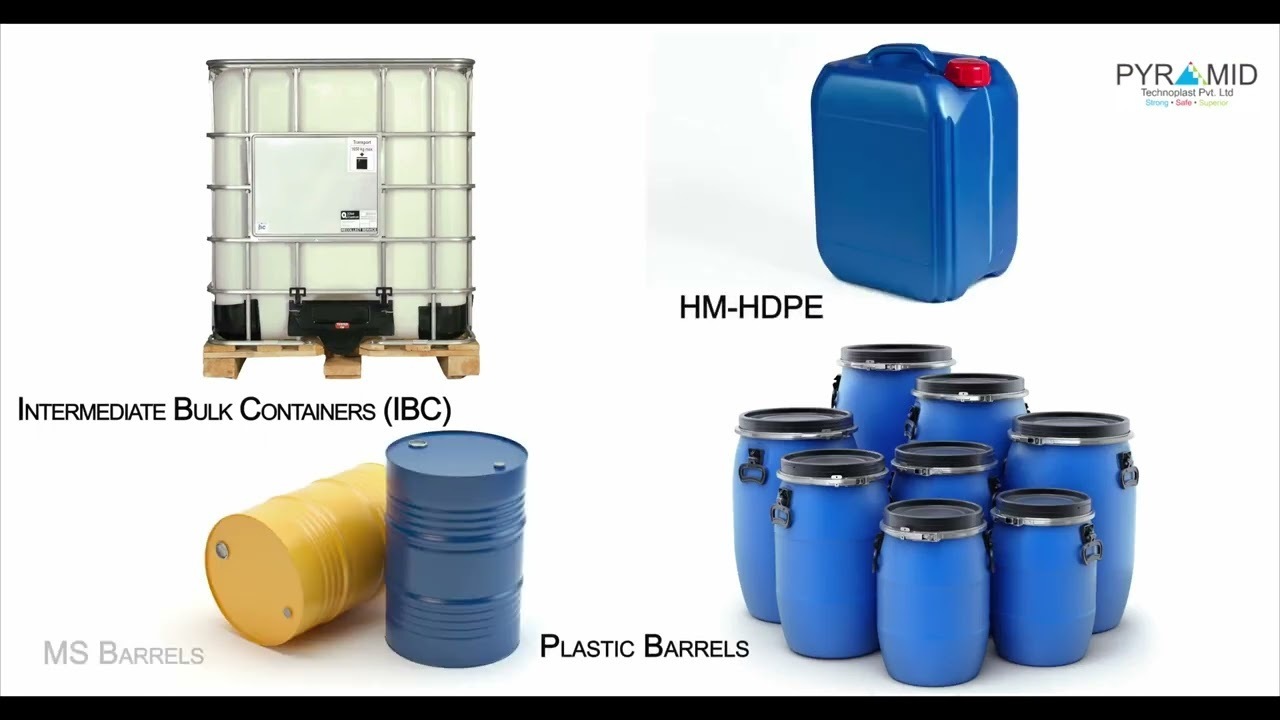

1. Polymer Drums (43% revenue)

- Used for chemicals, liquids

- Sizes: 20L to 250L

- High volume, stable demand

2. IBC Containers (37%)

- Large 1000L containers

- Used for bulk storage

- Fastest growing segment

3. MS Drums (11%)

- Steel containers

- Lower margins

4. Others (12%)

What makes the business interesting?

1. Boring but essential

Nobody skips packaging.

If chemicals are produced → packaging is required.

2. Diversified clients

Top customer = only 6% revenue

Top 10 = 27%

That’s actually healthy.

3. Backward integration

- In-house caps, lids

- Recycling plant

Translation:

Trying to control costs before raw materials control them.

But here’s the catch…

This is a commodity-like business:

- Margins depend on raw material prices

- Pricing power is limited

- Scale matters

So the real game is:

“Can they improve margins faster than they expand capacity?”

4. Financials Overview – Growth vs Profit Tug of War

Quarterly Results Detected → Q3 FY26 → Annualisation Rule