1. At a Glance – Bihar’s Maize King or Compliance ka Kingfisher?

Ladies and gentlemen, welcome to the most confusing buffet in Indian smallcap land.

On one side, you have Regaal Resources — a company growing like a Bihar mandi trader during peak harvest season:

- Revenue growing at 36.9% CAGR

- Profit doubling

- Capacity expansion underway

- Strong ROE (~25%)

And on the other side…

You have:

- DGGI raids

- Multiple ROC penalties (₹20 lakh, ₹12.5 lakh, ₹11 lakh… like a penalty IPL auction)

- ₹149 million tax recovery notice

- Governance lapses like delayed director appointments

So what exactly is happening here?

Is this a high-growth agro-processing gem, or a compliance ka serial offender wearing a growth costume?

Because let’s be honest — when a company gets:

- tax notices

- regulatory penalties

- and still says “everything is fine”

…it usually means either:

👉 management is confident

👉 or management is… very confident

And we all know how that ends in Indian markets.

But wait — before you dismiss it as another “operator special”, look deeper:

- Strong demand tailwinds

- Capacity doubling to 1,650 TPD

- Strategic Bihar location

- IPO money used for debt reduction

So here’s the real question:

👉 Is this a future midcap story being temporarily messy… or a future case study in corporate governance?

Let’s investigate.

2. Introduction – IPO Fresh, Drama Fresher

Regaal Resources got listed in August 2025.

Barely a few months old in the public markets.

And already:

- Price volatility

- Exchange clarifications

- Regulatory notices

- DGGI search

This is not a stock…

This is a Netflix series.

Now step back.

The company is in a boring but powerful business:

👉 Maize processing

👉 Starch manufacturing

👉 Agro derivatives

Basically, they take corn and turn it into:

- food ingredients

- industrial chemicals

- feed products

Not sexy. But profitable.

And India’s macro tailwinds are screaming:

- Packaged food boom

- Pharma growth

- Paper industry demand

- Export potential

So fundamentally — this is a right business at the right time.

But…

👉 Why so many compliance issues so early after listing?

👉 Why tax notices right after IPO?

👉 Why repeated penalties in Feb 2026 alone?

Coincidence?

Or early signs of operational looseness?

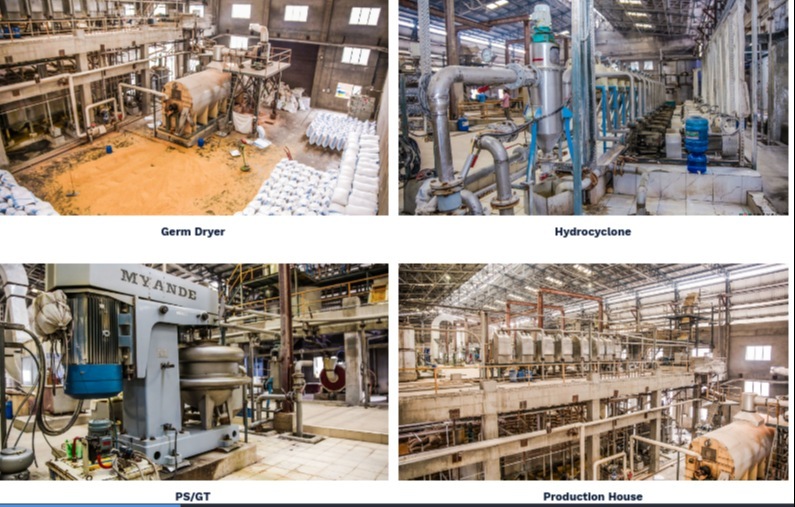

3. Business Model – WTF Do They Even Do?

Imagine this:

Farmer grows maize → Regaal buys it → crushes it → converts it into 20+ products → sells to industries.

That’s it.

Simple business.

But execution is everything.

What they sell:

- Native starch (59% revenue)

- Co-products (gluten, fiber)

- Traded maize

- Value-added products (tiny but growing)

Customers:

- Paper companies

- Food processors

- Animal feed companies

Basically, if you’ve eaten biscuits or used paper, Regaal is somewhere in that chain.

Competitive Advantage:

- Located in Bihar (cheap raw material)

- Only maize milling plant in that region

- Strong farmer network

- High capacity utilization (~99%)

But here’s the catch:

👉 This is a low-margin commodity business unless you move to value-added products.

And currently?

👉 Only ~2% revenue from value-added products.

So they are still:

👉 Volume player, not margin player

Question for you:

👉 Can they successfully transition to high-margin derivatives… or