1. At a Glance – Capsules, Corticosteroids & Chaos

At ₹153 per share and a market cap of ₹159 crore, Natural Capsules Ltd is currently trading at 0.65x book value (Book Value ₹237). Sounds cheap? Wait. The company just reported Q3 FY26 revenue of ₹37.75 crore and a net loss of ₹7.12 crore. OPM has collapsed to -6.15%. Interest coverage is negative. ROCE is 2.67%. ROE is 0.28%. Debt stands at ₹112 crore.

In the last 3 months, the stock is down 18.4%. In one year, it has fallen 27.8%. Meanwhile, EV is ₹266 crore and EV/EBITDA is a spicy 95.9. Yes, ninety-five.

This is a company that once enjoyed 21% operating margins in FY23 and EPS of ₹20.02 that year. Today? TTM EPS is -₹18.55.

The twist? They are India’s sole manufacturer of Dexamethasone API and Betamethasone API under their subsidiary. They have a ₹200 crore capex greenfield API facility. They are eligible for ₹67 crore under the PLI scheme.

So is this a turnaround-in-progress or a textbook case of “ambition financed by debt”?

Let’s open the capsule and see what’s inside.

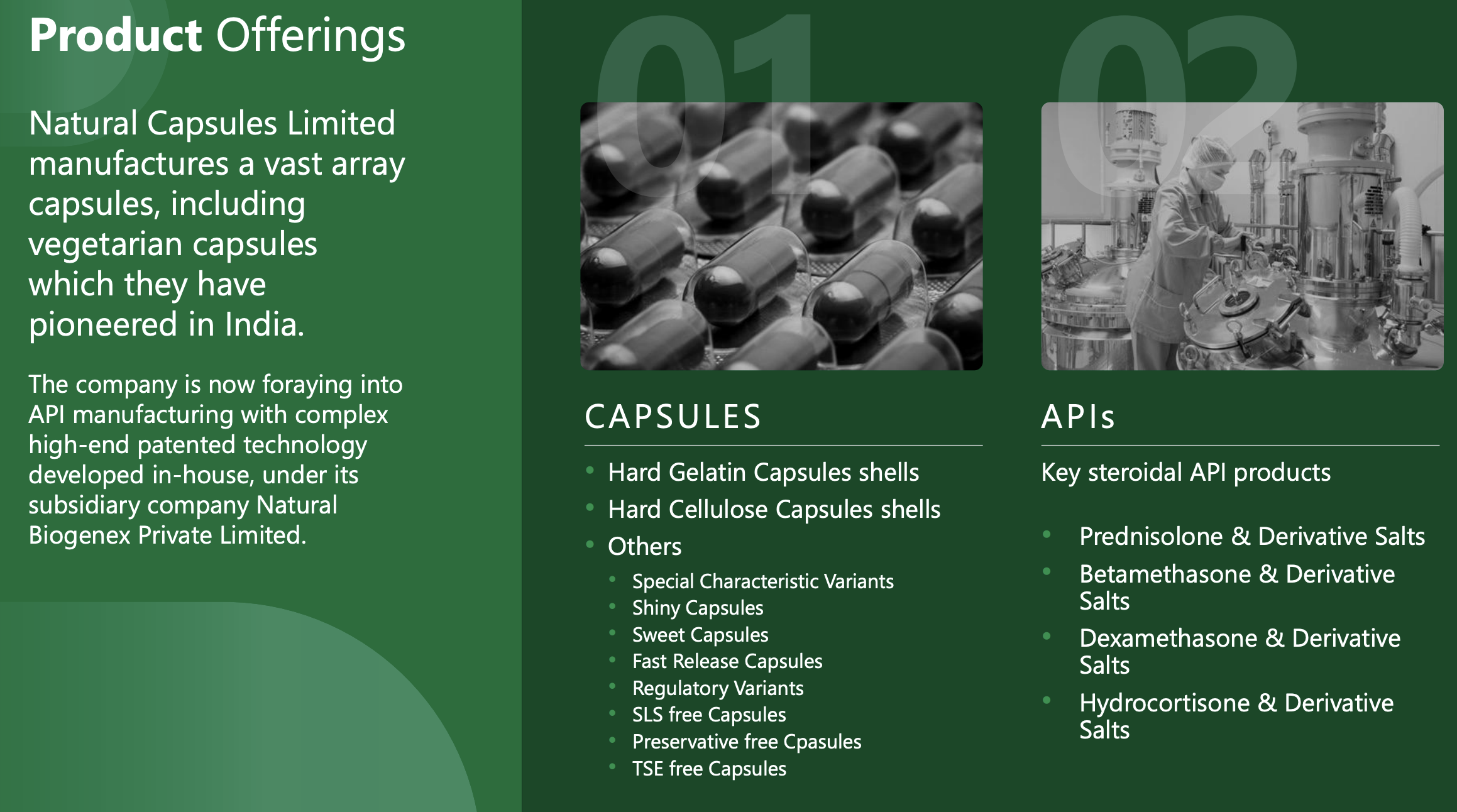

2. Introduction – From Capsule King to API Aspirant

Founded in 1993, Natural Capsules began as a hard capsule shell manufacturer. Over time, it became the first Indian manufacturer of vegetarian capsules and the second largest Indian gelatin capsule producer in India.

That’s respectable.

Two plants. Combined capacity: 19.5 billion capsules per year. FY25 utilization: 94.21%. That means machines were almost running at full speed.

So what went wrong?

The company decided to enter steroidal APIs through its wholly-owned subsidiary Natural Biogenex Pvt Ltd in 2020. They built India’s first integrated steroid API fermentation + synthesis plant in Tumkur. Total capex ballooned from ₹100 crore to ₹167 crore, and total project cost reached ₹200 crore including expenses.

Then came:

- API fermentation ramp-up delays

- Pondicherry plant temporary shutdown

- US tariff impact

- Credit rating downgrade

- Rising interest costs

Q3 FY26 showed revenue down 13.9% QoQ and PAT loss of ₹7.12 crore.

When you stretch too fast, even capsules crack.

But the bigger question: Is this temporary turbulence or structural stress?

3. Business Model – WTF Do They Even Do?

Let’s simplify this.

Segment 1: Capsule Shells

They manufacture:

- Hard Gelatin Capsules

- Hard Cellulose (HPMC) Capsules

- SLS-free, preservative-free, TSE-free variants

Customers include Abbott, Glenmark, Pfizer, Alkem, Aurobindo and more.

Capsules are boring but stable. Pharma companies don’t experiment with capsule suppliers easily. In fact:

- 86% turnover comes from repeat customers

- 30% customers are associated for 10+ years

- 58% for more than 5 years

That’s sticky revenue.

Exports go to 30 countries:

- Africa 45.6%

- South America 23.2%

- North America 21.5%

So capsules are their bread and butter.

Segment 2: Steroidal APIs

Now this is the ambitious child.

Products:

- Dexamethasone (10 MT capacity, sole Indian producer)

- Betamethasone (12 MT, sole Indian producer)

- Prednisolone (15 MT, one of two producers in India)

Facility: 5-acre Tumkur greenfield plant, designed for WHO-GMP, USFDA, EU GMP compliance.

Target:

- FY26 API revenue expected ₹90 crore

- Optimum utilization 60–70% by FY28

- Potential revenue ₹240–250 crore

- PLI incentive ₹67 crore over 6 years

Sounds fantastic on paper.

But fermentation ramp-up delays are slowing reality.

So here’s the big question:

Can they execute before debt squeezes