This is not a typo. The company earned ₹0.07 crore in the latest quarter and the market is valuing it at a P/E of 1,754. Even Bollywood scripts have fewer plot twists.

Q3 FY26 delivered revenue of ₹138.88 crore, almost flat YoY, but profit basically evaporated. Interest coverage stands at 1.00. Translation? Earnings are barely covering interest. That’s like earning ₹10 and paying ₹9.99 to the bank.

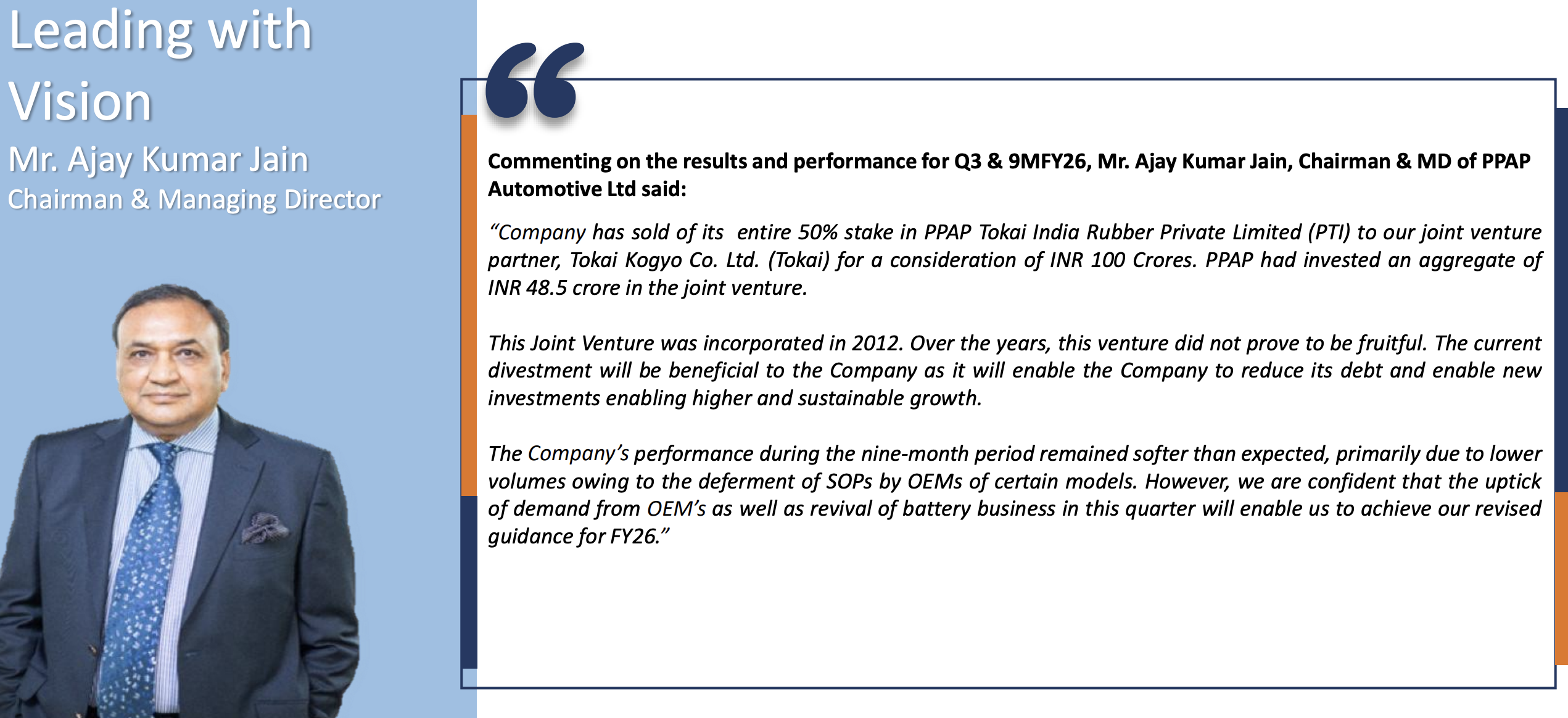

But wait — management just sold a 50% JV stake for ₹100 crore. Debt may fall. Interest cost may drop ~30%. Batteries are “about to turn around.” Tool room is “robust.” Aftermarket is “scaling.”

Smallcap detective mode activated. Is this a turnaround before ignition… or an engine misfire wrapped in plastic moulding?

2. Introduction – The Plastic Empire With Identity Crisis

PPAP Automotive Ltd started in 1995. It makes automotive sealing systems and plastic moulded parts. Think rubber channels on car windows, plastic trims, injection moulded components — the silent heroes of every car.

For years, the business was straightforward: make PVC/TPO profiles, supply to OEMs like Maruti, Honda, Hyundai. Collect money. Repeat.

Then ambition entered the chat.

Batteries? Yes. Aftermarket? Yes. Industrial non-auto? Yes. Tool room as independent profit centre? Yes. JV with Japanese partner? Also yes.

Classic smallcap syndrome: “We can do everything.”

Now Q3 FY26 shows the cost of that expansion phase. Sales stagnation. Profit collapse. Interest coverage tight. Customer concentration high.

Management admitted capital allocation mistakes in concall. Board questioned “bleeding capital.” They exited the JV and received ₹100 crore.

Good move? Probably. Late move? Maybe.

The big question: Is this disciplined reinvention — or post-damage control?

And more importantly: Can a company with ROE of 2.37% justify a 1,754 P/E multiple?

Let’s dissect.

3. Business Model – WTF Do They Even Do?

PPAP has five engines running.

1) Automotive Parts

Core business. PVC/TPO sealing systems and injection moulded parts. Engine agnostic — works for ICE and EV.

2) Commercial Tool Room (Meraki)

Precision mould manufacturing. Up to 1.5m × 1.0m moulds. Serves automotive + white goods + medical.