1. At a Glance – Small Cap, Big Drama

₹152 crore market cap.

₹81.5 share price.

3-month return: -14.6%.

1-year return: -20.8%.

ROCE: 78.6% (yes, you read that right).

ROE: 68.2%.

Debt: ₹1.30 crore. Basically chai-paani level.

Now the spicy part.

Latest quarter (Dec 2025):

Revenue ₹17.68 crore.

PAT: -₹0.30 crore.

EPS: -₹0.16.

So we have a company with stunning return ratios but a quarterly loss. And if you look carefully at the P&L, earnings include ₹12.57 crore of other income (TTM). That’s not core business. That’s financial jugaad.

DCM is that one friend who says, “Business is stable bro,” while simultaneously fighting real estate regulators, dealing with disputed advances, wage lockouts, and municipal demands worth ₹24,134 lakh.

Confused? Good. You should be.

Because DCM is not a simple IT company.

It’s a cocktail of:

- Grey iron castings

- Suspended real estate projects

- IT infrastructure services

- Related party transactions

And somewhere inside this khichdi is value… or volatility.

Let’s investigate.

2. Introduction – The Multi-Business Maze

DCM Ltd was incorporated in 1977. That’s vintage India. License Raj era.

Fast forward to 2026, and the company now runs three verticals:

- Engineering (grey iron castings)

- Real Estate (Hisar land parcel drama)

- IT Infrastructure Services

Three completely different businesses under one roof.

Why?

Because India.

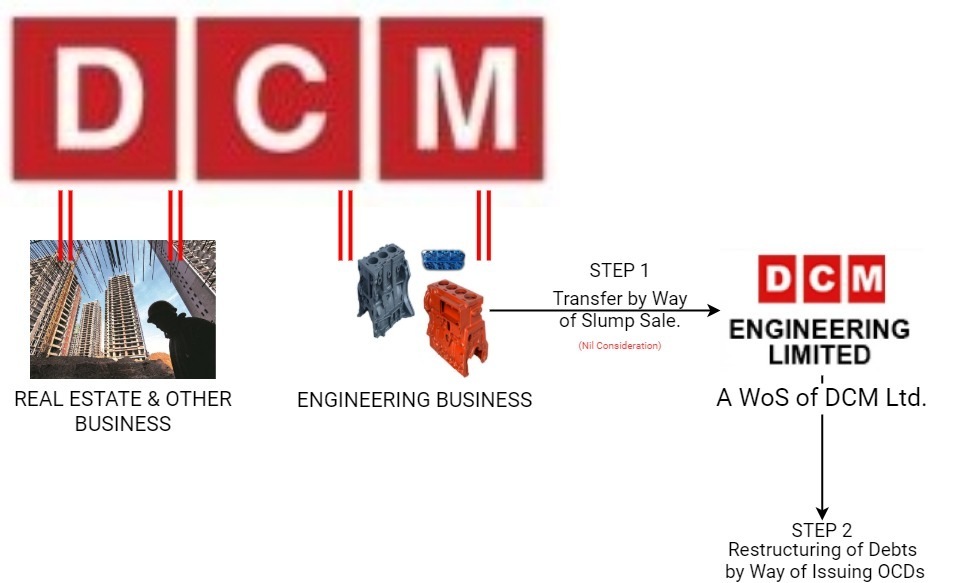

On one side, they manufacture cylinder heads and blocks through DCM Engineering Limited.

On another, they are trying to develop 68.35 acres in Hisar under Deen Dayal Jan Awas Yojna.

But wait.

That project’s license was suspended by DTCP in April 2023 due to an inquiry by the Deputy Commissioner, Hisar.

And then in November 2025, they issued a notice to forfeit ₹5,000 lakh JDA advance and terminate the agreement.

Add to that:

- Lockout wages ₹7,845 lakh

- MCD demand ₹24,134 lakh

This is not a company. This is a courtroom season on Netflix.

Meanwhile, the IT subsidiary is building cloud, AI-ML, RPA, NLP-based solutions. Basically all buzzwords in one PowerPoint.

So question for you:

Are we looking at