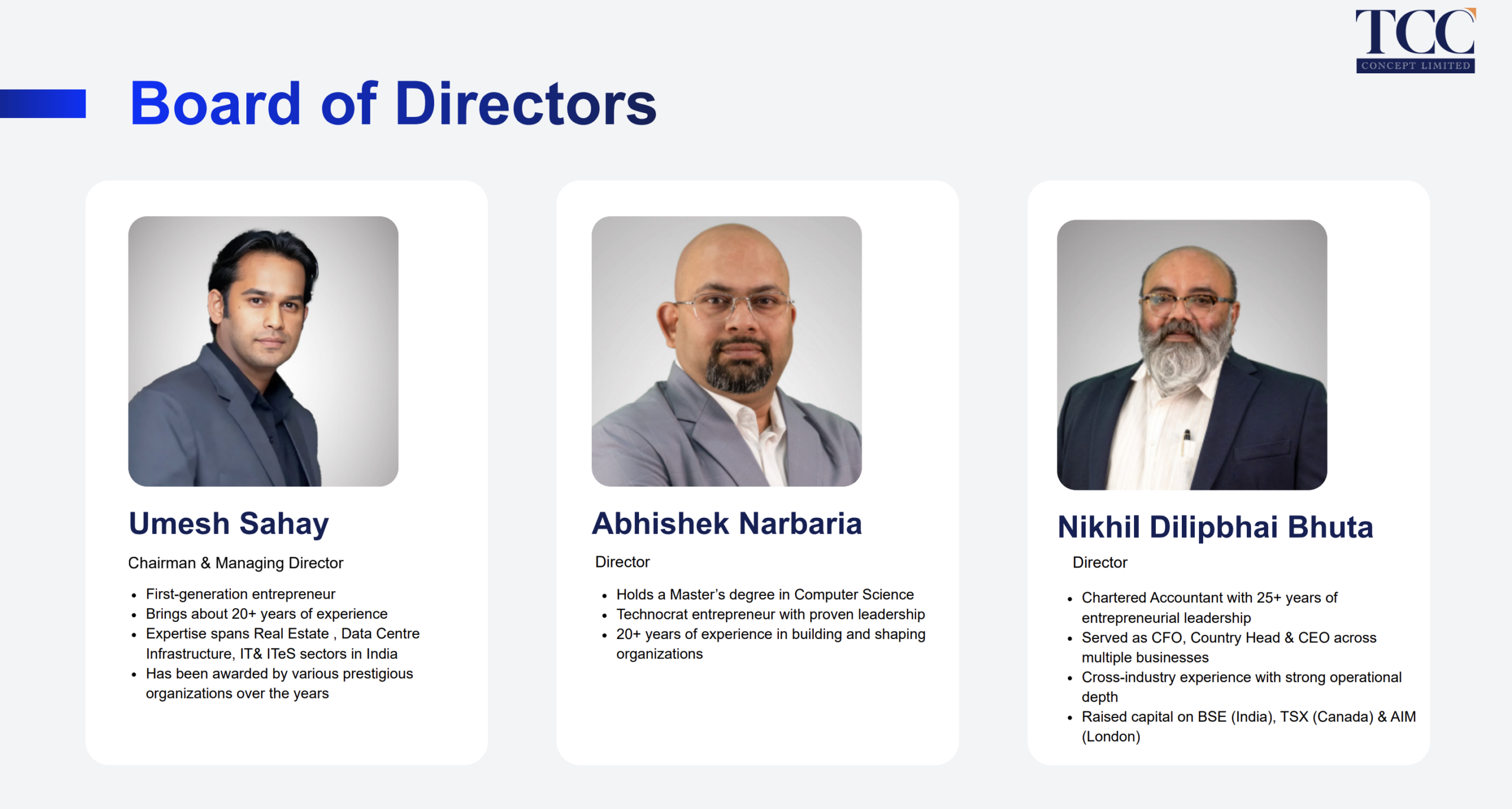

1. At a Glance – The Real Estate Aggregator That Just Bought a Furniture Empire

TCC Concept Ltd is not your typical sleepy real estate brokerage. At ₹433 per share and a market cap of ₹2,060 Cr, this former “Aaswa Trading and Exports Ltd” has reinvented itself into a multi-headed corporate experiment spanning real estate, AI platforms, data centres, and now… furniture retail.

Q3 FY26 numbers? Revenue at ₹46.5 Cr versus ₹22.4 Cr last year. That’s a 108% YoY jump. PAT at ₹13.9 Cr, up 35% YoY. Operating margins? A juicy 65% in the quarter. Stock P/E sits at 40.5 while industry median is 33.

But here’s the masala — the company has acquired 98.98% of Pepperfry for ₹661.47 Cr via share swap. Yes, that Pepperfry. The furniture giant.

Return over last 3 months? Down 16.2%. Market seems confused. Should you be? Or is this one of those “transformation stories” that look messy before they look magical?

Let’s open the file.

2. Introduction – From Trading Company to Tech-Real Estate-Furniture Cocktail

TCC Concept Ltd was incorporated in 1984. For decades, it was not exactly lighting up Dalal Street.

Then FY24 happened.

Name changed from Aaswa Trading and Exports Ltd to TCC Concept Ltd. Registered office shifted from Gujarat to Pune. Object clause altered to add real estate services, brokerage, property tech, leasing, and subscription-based technologies.

Translation? New avatar unlocked.

Then came acquisitions:

- 100% Brantford Ltd

- 100% EMF Clinic Pvt Ltd

- 100% Altrr Software Services Ltd

- 98.78% NES Data

- 98.98% Pepperfry (via ₹661.47 Cr share swap)

This isn’t diversification. This is corporate Avengers assembling.

But here’s the detective question: Is this a carefully crafted ecosystem… or a corporate buffet where everything is on the plate?

Promoter holding fell from 60.87% to 45.69% by Dec 2025. That’s a sharp drop. Preferential issues, ESOPs, share swaps — dilution has been busy.

Yet revenue has jumped. Profit has grown. Working capital days improved dramatically from 770 to 86.

So are we witnessing genuine transformation or financial engineering?

Let’s break it down.

3. Business Model – WTF Do They Even Do?

At its