Ratios That Really Matter – Sector-wise Cheat Sheet for Indian Stocks

Investing is like cricket, dear friend – you need different strategies for fast bowlers vs spinners. Likewise, each stock market sector in India has its own “go-to” financial ratios that tell you if a company is hitting sixes or stuck on a sticky wicket. Let’s tour the major sectors (from Aerospace to Transport) and check the top 2–3 ratios that analysts swear by for each. Don’t worry – we’ll keep it simple, throw in some Indian tadka (flavor), and maybe a joke or two. Grab your chai, and let’s get started!

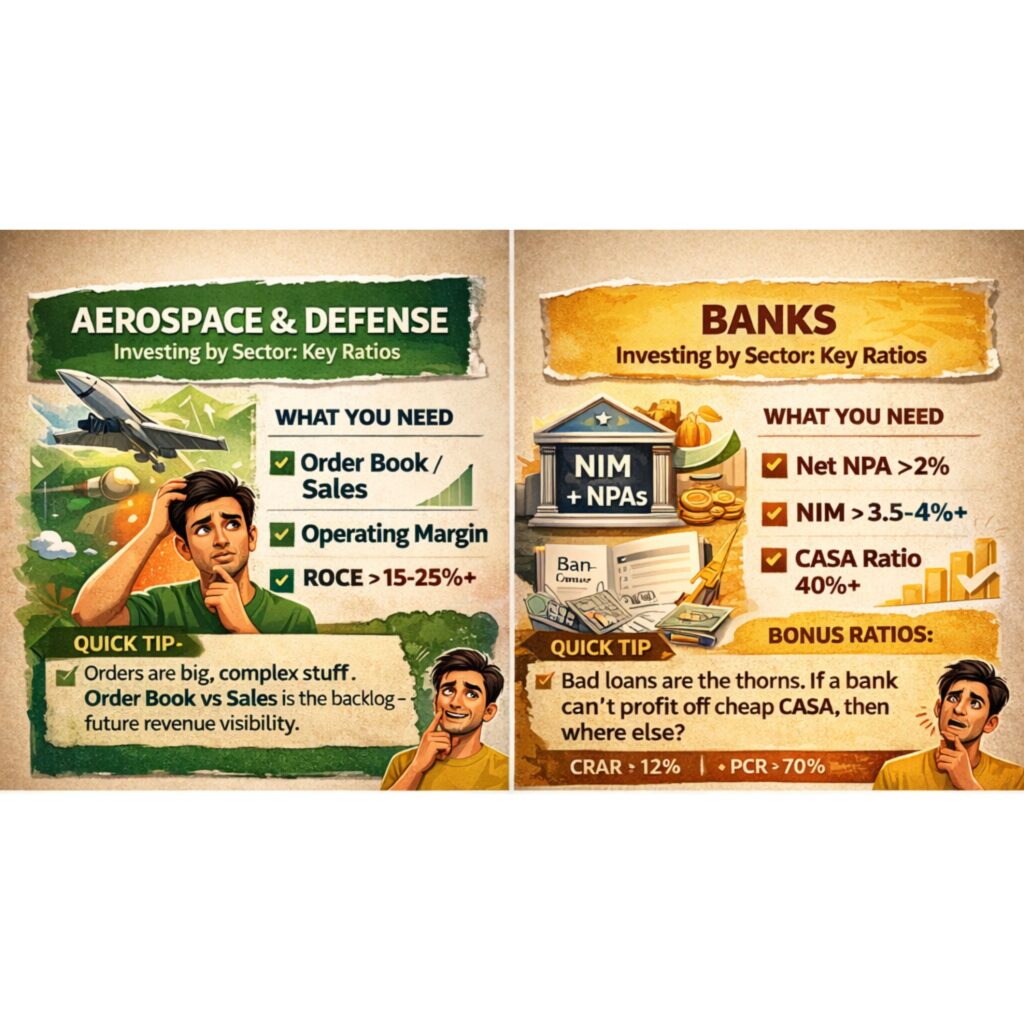

Aerospace & Defense 🚀🔫

This sector makes fighter jets, missiles, and high-tech equipment. It’s like the ISRO of the stock market – long projects and big budgets. Key ratios here are about future revenue and efficient use of money:

Order Book to Sales Ratio: Think of this as the pre-order queue for a new iPhone. A higher order book (confirmed orders) compared to current annual sales means the company has revenue visibility for years to come. For example, if a defense PSU has an order book worth 3x its annual revenue, it’s like a restaurant with tables booked out for months – a comforting sign![1]

Operating Profit Margin: Defense deals can be complex, so we check how much profit is made per ₹100 of sales. A healthy margin (say 15–20%+ operating margin) means the company isn’t just winning contracts but also cooking them efficiently. High margins are like a chef who still makes a profit even after a generous discount – it shows cost control.

ROCE (Return on Capital Employed): This tells us how well a company uses the funds (both equity and debt) in its business. A higher ROCE (say above 15%) is great – some top defense firms boast ROCEs above 20–25%. It’s like the yield of a farmer’s land; more mangoes per tree means the farm is well-run. Low ROCE (single digits) might mean money is tied up in big projects not yet paying off.

Why they matter: The government is usually the only buyer here, and payments can be slow. A big order book/sales ratio indicates future revenues are locked in, reducing uncertainty[1]. Operating margin shows if the company can build complex weapons without cost overruns. And ROCE reveals if all those tanks and rockets are generating a decent return, or if capital is sitting idle in a hangar. Tip: Also keep an eye on debt levels – defense companies with moderate debt (debt-to-equity under 1) are preferable. Too much debt can ground even the best fighter jet.

Benchmark: Many Indian defense stocks trade at high P/E ratios (40x–50x earnings) due to growth hype,so focus on these fundamental ratios. A company like HAL (Hindustan Aeronautics) has a strong order book and healthy margins, which justifies its premium. If an aerospace firm has an order book equal to, say, 4 years of revenue, fat margins, and low debt – that’s as good as an Agni missile on target.

Automobiles 🏎️🚗

From Maruti’s mass-market cars to Tata Motors’ trucks, auto companies are the road runners of the economy. They face cyclical demand and cost pressures (rubber, steel, fuel). Key ratios here vroom around profitability and efficiency:

Operating Margin (EBITDA Margin): Car makers often run on thin margins – think 8–15% range for operating margin in good times. Higher is better, of course. It’s like mileage (km per liter) – a higher margin means the company squeezes more profit out of each rupee of sales. If raw material costs drop or a model is a hit, margins rev up. Example: Top auto ancillaries in India maintain ~12% EBITDA margins, while some luxury car players might rev higher. Single-digit margins (or losses) are a red flag indicating the company might be selling “at cost” just to stay in the race.

Sales Growth & Market Share: Not a ratio per se, but crucial. Volume growth (number of vehicles sold) is king. If a company’s sales are growing faster than the industry, it’s gaining market share – the equivalent of overtaking rivals on the highway. For instance, if overall car sales grew 5% but Maruti grew 10%, Maruti is zooming ahead. Consistent market-share gains usually reflect strong brand or product lineup (think “Swift”ly selling cars).

Return on Capital Employed (ROCE) or Return on Equity (ROE): Auto manufacturing is capital-intensive (factories, robotics, R&D for new models). A solid ROCE/ROE (say 15–20% in good years) shows the company is generating decent returns on its huge investments. For example, Eicher Motors (Royal Enfield) enjoyed high ROCE during the bike boom. Low single-digit ROCE means the company’s capital is idling in the garage.

Why they matter: Auto is cyclical – boom and bust. Operating margin tells you how well a company can handle cost swings (like steel prices or discounts during festive season). In downturns, margins can skid – some automakers barely break even if sales slump. Market share and sales growth show if the firm’s models are consumer favorites (a long waiting list for an SUV is a good problem!). ROCE/ROE reveals if the huge investments in plants are paying off or just depreciating. Good vs Bad: A company like Maruti typically has double-digit net margins and ROE ~15–20% in good years – that’s good. If margins fall under 5% or ROE is in single digits, it’s like a car stuck in first gear. Also watch debt – many automakers keep debt low; if you see debt-to-equity zooming past 1:1, alarm bells (or honks) should sound.

Practical tip: Auto analysts also watch inventory levels (unsold cars at dealerships). If inventory piles up (say more than 30 days of sales), the company may cut production or offer discounts – hurting future margins. So, a lean inventory and steady operating margin indicate the company isn’t overproducing and discounting heavily. In short, healthy margin, growing sales, low debt = a well-tuned engine. Anything else and the company might need a pit stop repair.

Banking & Finance 🏦💰

Banks are a different beast – instead of selling products, they deal in money itself. Indian banks have their own lingo of ratios. Think of a bank like a vada pav stall that lends out money (buns) and collects it back with interest (the chutney!). Key ratios to judge a bank’s health:

Net NPA (Non-Performing Assets) & Gross NPA: This is the bad loan indicator. Gross NPA % tells us how much of the total loans have gone sour (customers not paying up). Net NPA is after provisions (money set aside for losses). In India, lower is hugely better. Good banks keep Net NPA under 1–2%; anything above 5% is worrisome, and in double digits is disastrous (remember the PSU bank crisis of 2018). Think of NPAs like the percentage of friends who never return the money you lent – if too many default, you’re in trouble. A Net NPA < 2% is considered good[5], showing the bank’s loan book is mostly healthy.

NIM (Net Interest Margin): This is basically the bank’s spread – the difference between what it earns on loans vs pays on deposits, as a percentage of interest-earning assets. For Indian banks, a NIM of 3–4% is healthy. Higher NIM means the bank is like a smart shopkeeper – borrowing at low cost (your savings account at 3% interest) and lending at higher rates (personal loans at 12%), pocketing the juicy difference. A NIM above ~3.5% is excellent (e.g. Kotak Bank ~4.5%), while anything under 2% is like selling at cost – not sustainable[10].

CASA Ratio (Current Account Savings Account ratio): This measures the proportion of cheap funds in total deposits. CASA accounts (savings, current) pay very low interest (0–4%), unlike fixed deposits. A high CASA (40%+ is strong) means the bank has a lot of low-cost money, which boosts NIM. In India, HDFC Bank and others pride themselves on high CASA ~45–50%. It’s like having a big portion of roti and rice in your thali that you got at discount – helps keep overall costs down.

(We promised 2–3 ratios, but with banks a few more are vital:)CRAR (capital adequacy) ensures the bank has enough capital buffer (typically 12%+ is good), and Provision Coverage Ratio (PCR) shows how much of bad loans are already provided for (PCR > 70% is healthy). Also ROA around 1%+ is good for banks, since their assets are mostly loans. But let’s not drown in alphabet soup!*

Why they matter: Banking is all about trust and risk management. NPA tells you if the bank’s borrowers are paying or partying with the money (you want a bank that’s conservative in lending – no Vijay Mallya situations). NIM indicates profitability – higher NIM is like a wider dosa, more for the bank to eat. CASA and NIM go hand-in-hand: more low-cost CASA = better NIM. Ultimately, these ratios signal if a bank can weather storms.

Good vs Bad: A well-run private bank like HDFC Bank had Gross NPA ~1.4% and Net NPA ~0.4% recently, NIM ~4%, CASA ~45%. That’s a chef’s kiss combo – very few bad loans and high margin. In contrast, a struggling bank might have Gross NPA of 10%+ (ouch) and NIM of 2% or less – meaning many loans gone bad and thin profit on each rupee lent. Also, such a bank’s P/B ratio will be low (often <1) because investors don’t trust its book value. By the way, banks are valued by P/B more than P/E. For instance, SBI trades around 1.5x book, whereas Kotak is ~4x book due to superior metrics.

Analogy: NPAs are like the proportion of your friends who never return borrowed money (lower the better), NIM is the profit on each vada pav you sell (higher means fatter pav), and CASA is like having ingredients (money) that are dirt cheap or free (current account deposits are like free salt – essential and virtually no cost). Focus on banks with low NPAs, solid NIM, and high CASA – those are the HDFC/Bajaj Finance of the world, not the next Yes Bank fiasco.

Chemicals (Specialty & Commodities) 🧪⚗️

The chemical sector spans commodity chemicals (think basic bulk chemicals, fertilizers) to high-margin specialty chemicals (for pharma, cosmetics, etc.). India’s specialty chemical firms have been on a roll, thanks to the China+1 trend. Key ratios revolve around margins and efficiency:

Gross Profit Margin / EBITDA Margin: This instantly tells you if it’s a commodity or specialty business. Commodity chemical makers (like basic petrochemicals or fertilizer companies) have relatively lower margins (maybe 10–20% gross margin), because products are undifferentiated – like selling salt, you compete on price. Specialty players boast higher margins (30–50% gross, or 20%+ EBITDA) because of niche products and pricing power. If a chemical company has consistently high margins and isn’t swinging wildly with raw material prices, that’s a good sign of a “moat” (specialty or brand). Example: A company like Alkyl Amines or Naveen Fluorine often has healthy margins even when raw material prices fluctuate – indicating strong pricing power. On the other hand, a commodity player’s margin is at the mercy of global price cycles (e.g., if crude oil spikes, their costs go up and margins can crash).

ROCE (Return on Capital Employed): In chemicals, ROCE is king for gauging efficiency. Some Indian specialty chemical darlings have ROCEs in the 40–50% range, which is phenomenal – it means for every ₹100 of capital, ₹40-50 of operating profit. The industry median ROCE might be ~18%, so anything above that indicates a superb business model. High ROCE usually comes with zero or low debt in this sector – many star performers are essentially debt-free. If ROCE is single digits, the company might be struggling with capital-intensive projects or low-margin products.

Debt-to-Equity Ratio: Why this again? Because chemical plants can be expensive, and companies often take loans to expand capacity. But debt is double-edged: it can boost growth or blow up with cyclic downturns. Many of India’s best specialty chemical companies carry no debt or very low debt, funding expansion via internal cash. A D/E ratio < 0.5 is comfortable; some even have zero debt. If you see a chemical company with high debt (D/E >> 1) and low interest coverage, be cautious – a downturn in chemical prices could put it in a solvent… I mean insolvent… situation.

Why they matter: Specialty chemical companies trade at high P/E multiples (often 30x, 50x earnings) because of growth prospects. But to deserve that, they should have stable or rising margins and high ROCE. Gross margin and ROCE confirm if the business truly has an edge or is just riding a temporary price swing. Debt level tells you if growth is sustainable or on credit overdose.

Good vs Bad:Clean Science & Tech, for instance, has averaged ~47% ROCE over a decade with zero debt– that’s excellent. It also has high margins and strong growth. Such a company justifies a rich valuation. On the flip side, a fertilizer company might have ROCE ~8% and lots of government-controlled pricing – not exciting; it’s valued at a low P/E for a reason. Benchmark: Indian specialty chemical firms generally spend around 6–9% of revenue on R&D, a sign of focusing on innovation. If R&D spend is near zero and margins are low, the company is likely a price-taking commodity player (or sleepy public sector unit).

Practical tip: Look at margin stability. If a chemical maker’s margin jumps one year and collapses the next, it might be commodity-oriented. The winners often show consistent or gradually improving margins over cycles. Also, monitor export percentage – many Indian chemical firms export a lot (good for growth, but also exposes to forex fluctuations). High ROCE + low debt + decent margins = a chemical stock that could spice up your portfolio rather than blow it up.

Consumer Goods (FMCG) 🛒🍿

These are your everyday products – soaps, snacks, shampoos – dominated by FMCG giants like Hindustan Unilever, ITC, Nestlé etc. Boring? Maybe. Profitable? Oh yes. FMCGs are like that reliable friend who always has money for chai. Important ratios here focus on profitability and efficiency, since growth is steady but not high:

Net Profit Margin: FMCG companies often enjoy juicy margins thanks to strong brands and economies of scale. A net margin of 15–20% is common for the giants. For example, HUL’s net profit margin hovers around 17%. That means out of ₹100 of KitKats or Lux soap sold, ₹17 is pure profit – quite high, courtesy of brand power (you pay a premium for that soap’s “fresh fragrance” promise!). Smaller or new consumer goods companies might have lower margins (<10%), but established ones guard their margins fiercely. If an FMCG’s margin is declining year after year, it could indicate rising input costs (like palm oil, sugar) not being passed on – a worry.

ROE / ROCE: FMCGs are typically asset-light (they don’t need huge factories for each additional packet of chips sold) and have high return on equity. ROE of 20–30%+ is a hallmark of a strong FMCG player. For instance, HUL and Nestlé India have ROE in the 20–30% range, sometimes even higher in good years. This is because they have negative working capital (they get money from distributors upfront, pay suppliers later) and strong brands – a money machine. High ROE is like a sign of a dominant business – every rupee of shareholder money is churning out 20-30 paisa of profit annually. In contrast, if an FMCG has ROE under 10%, something’s off – maybe it’s investing heavily for growth or losing market share.

Asset Turnover / Working Capital Cycle: (Okay, this is two things, but hear me out.) FMCGs thrive on volume and efficient use of capital. Asset turnover (Sales/Total assets) shows how many rupees of sales are generated per rupee of assets – often high for FMCG because of lean balance sheets. They also often have negative cash conversion cycles – meaning they receive cash from customers faster than they pay their suppliers. This effectively finances their business at zero cost. You won’t often get this number directly, but a clue is in the current ratio (often ~1 or less) and quick movement of inventory. In simple terms, a great FMCG company is a bit like a grocery store that sells products so fast and on cash that it uses the customer’s money to stock up before the supplier’s bill is due – sweet deal! If you see inventory days creeping up or receivables rising, it could mean the company is pushing product with longer credit – not ideal.

Why they matter: FMCG is usually not about breakneck growth (mature firms might grow sales 5–12% a year), so investors pay up for consistency and high returns on capital. Margins and ROE tell you if the business has a moat (brands, distribution). High margins and ROE suggest the company can pass on raw material cost increases via price hikes or by cutting a little gram from each biscuit without consumer noticing 😉. Low margins might mean the company sells commoditized products or is in a price war.

Good vs Bad:Good FMCG: high margin, ROE 25%, virtually no debt, steady growth – e.g., Nestlé India has ~20% net margin and ROCE ~50% (due to low capital needs), which is superb. Bad FMCG: lower margin (~5-8%) and ROE < 10% for a smaller player could mean it lacks pricing power or scale. That said, if it’s a nascent company investing in brand building, margins may improve later – but as a beginner, stick with those already showing strong numbers.

Benchmark ranges: In India, FMCG behemoths often trade at P/E ratios of 40–60x. Yes, that’s nosebleed high, but that’s because of their stable profits and high ROE. For instance, HUL has been valued around 55x earnings. Why would anyone pay ₹55 for ₹1 of HUL’s earnings? Because that ₹1 is super high quality – likely to grow and continue for decades with high ROE. If you find an FMCG stock at a P/E of 10, chances are it’s either in a very bad shape or it’s a smaller one yet to earn investor trust. Tip: Look at volume growth (the number of units sold) reported each quarter. A good monsoon or low inflation often leads to higher volume growth for FMCGs (rural demand up). High volume growth + stable margin = double win (more sales without discounting).

In summary, FMCG ratios are sweet: Big margins, fat ROE, skinny debt. These companies are the marathon runners of Dalal Street – they won’t sprint, but they’ll reliably compound your wealth. Just don’t expect thrill-a-minute growth; think slow and steady Ladoo-making machine.

Information Technology (IT) 💻🖱️

India’s famed IT services sector (TCS, Infosys, Wipro, etc.) is all about brains, not heavy machines. They earn dollars by writing code and managing systems. The business model is asset-light (main assets are computers and offices) but people-heavy. Key ratios center on profitability and return since growth is somewhat predictable (linked to global tech spending):

Operating Profit Margin: Indian IT companies generally have strong operating margins, often in the 20–30% range. The big boys like TCS have historically had EBIT margins around 25% or more(in fact, TCS reported ~30% in one quarter, though ~25% is more typical). Even mid-sized IT firms aim for 15–20% margins. High margin indicates the company manages costs well (utilization of staff, offshoring advantage) and can command decent billing rates. If margins drop a lot, it could be due to wage hikes or pricing pressure. Analogy: margin is like how much ghee is left after making a batch of ladoos – IT firms usually have a lot left because once they cover employee costs, the additional revenue from more projects mostly flows to profit (scalable business).

Return on Equity (ROE): IT companies often have high ROE because of their asset-light model and generous dividends. TCS, for example, had an ROE of ~47% in 2022-23, and Infosys about 32%. These are sky-high. Why? They require little reinvestment – a lot of profit is paid out or sits in cash, and equity is not bloated. An ROE above 25% is stellar and common among top IT players. If an IT company’s ROE falls into teens or single digits, either it’s hoarding too much cash (which increases equity base) or its profitability is under pressure. For investors, high ROE with good dividend payout is like having your cake and eating it too – the company generates tons of cash and returns it as well.

Employee Metrics (Bonus: Utilization & Attrition): These aren’t classic financial ratios, but they’re important. Utilization rate (percentage of employees billable on projects) and attrition rate (staff quitting) give context. High utilization (80%+) is good for margins, while high attrition (20%+ per year) can be costly as hiring/training new folks hurts margins. You’ll see these discussed in result commentaries. If attrition is surging, future margins might be impacted as companies raise salaries to retain talent. Keep an eye on it as a qualitative factor.

Why they matter: IT services operate on relatively fixed costs (mostly salaries). So operating margin is a direct measure of efficiency and value-add. A company like Infosys maintaining ~21% margin despite wage inflation means it moved up the value chain or managed costs well. ROE reflects both profitability and capital allocation; IT firms with high ROE and huge cash piles often give special dividends or buybacks. For example, Infosys and TCS routinely distribute 70-80% of profits as dividends, which keeps ROE high by not accumulating unnecessary equity.

Good vs Bad: A top-tier IT firm has ~25% operating margin, ROE > 30%, and steady revenue growth (say 10–15% in rupee terms). That’s the profile of a wealth creator. On the other hand, if an IT company’s margin is falling towards 10% or single digits, it might be stuck in a competitive, low-value segment or mismanaging costs. A low ROE might mean it’s sitting on cash (which is not terrible, just not being utilized – investors often pressure such companies to return cash). Example: Some smaller IT companies had ROEs drop when they kept cash from big deals and didn’t deploy or return it – effectively bloating equity. Investors then often prefer they announce a dividend.

One more ratio often used is PE to Growth (PEG) ratio: since IT companies trade at P/E of 20–30 and grow earnings ~10–15%, a PEG ~1–2 is common. But don’t sweat this; focus on fundamentals: margin and ROE. High margin and ROE, coupled with even moderate growth, usually make a solid investment. Also, USD/INR matters – a weakening rupee often boosts rupee revenue for IT firms (since a lot of revenue is in USD). So a tip: if rupee falls sharply, IT margins might get a temporary bump (exports become more valuable).

Humor bit: IT analysts also talk about “onsite-offshore mix” – sending more work offshore (India) increases margin (less cost). So think of it like this: if your cousin in the US pays you in dollars to code, but you do the work from India and spend in rupees, you’re minting money – that’s the IT offshoring model in a nutshell, and that’s why these ratios look so good!

Pharmaceuticals & Healthcare 💊🏥

Indian Pharma is two-fold: domestic branded generics (companies selling medicines in India, often under brand names) and export-focused generics/API manufacturers (selling to US, EU). This sector’s performance hinges on regulation and R&D. The key ratios revolve around margins, but with a twist of R&D and debt management:

R&D Expense Ratio: Innovation is lifeblood in pharma. The R&D spend as % of sales shows how much a company is investing for future drugs. Indian pharma companies typically spend 6–9% of revenue on R&D. A higher R&D ratio could indicate focus on complex generics or new drug development – good for the long term, provided it yields results (approvals, new launches). If a company spends too little on R&D (say 1-2%) and isn’t a pure-play API (which require less R&D), it might be milking old products without preparing for the future. Conversely, very high R&D (>15%) might hurt short-term profits, but could pay off big (or flop – it’s a risk). Think of R&D spend like practice hours for a cricket team – no guarantee of winning, but no practice means certain failure[29][30].

EBITDA/Net Profit Margin: Pharma margins vary widely. Domestic-focused companies with strong brands (e.g. Abbott India, Pfizer India) often have 20%+ net margins. Pure generic exporters might have lower net margins (~10-15%) due to competition in regulated markets, but still healthy. A good EBITDA margin for pharma could be 20–30%. If you see margins consistently above 30%, that could indicate either a niche (e.g. Divi’s Labs API business with high margins) or maybe a one-time boost (like a drug with temporary monopoly). Low margins (<10%) could mean pricing pressures or too high an expense structure.

Debt/Equity or Interest Coverage: Many pharma companies historically took on debt for acquisitions abroad (remember Sun Pharma-Ranbaxy deal) or for capacity expansion. But as a rule, it’s safer if debt is low, because pharma can face unpredictable challenges (USFDA bans, patent losses). A debt-to-equity ratio below 0.5 is comfortable for most. High debt in pharma is particularly risky because if a big product fails or gets banned, the fixed obligations remain. Interest coverage should ideally be well above 5x. Most large Indian pharmas keep debt moderate; for example, Sun Pharma after paying down Ranbaxy’s loans became virtually debt-free. In contrast, some smaller companies that took FCCBs (foreign currency loans) in the 2000s got burned. So a quick health check: if interest coverage is, say, 10x, the company’s practically debt-free; if it’s 2x, the company is choking on pills it can’t swallow.

Why they matter: Pharma is a mix of stable and risky. Domestic business is stable (people fall sick in good times or bad), but export generics can be volatile (patent cliffs, U.S. FDA inspections). Margins tell you how much cushion the company has if, say, a price control hits or a plant is shut down temporarily. R&D ratio is a guide to future pipeline: a company not investing in R&D may see its portfolio go obsolete. But R&D heavy model needs monitoring – is it yielding new approvals? For instance, Dr. Reddy’s or Biocon might spend a lot on R&D for biosimilars – if those get approvals, great, if not, the spend was a drag. Debt matters because pharma downturns (from regulatory issues) can be sudden and severe, and you don’t want high fixed costs then.

Good vs Bad: A good pharma company (from an investor perspective) might have EBITDA margin ~25%, steady or growing; ROCE in the mid-teens (or higher if it’s more consumer-health focused); moderate R&D ~8% of sales with a visible product pipeline; and little debt. These tend to trade at P/E multiples of 20–30. Example: Abbott India has strong domestic franchise, high margins ~20%, and virtually no debt – hence it commands a premium valuation. A troubled pharma might show declining margins (e.g., intense U.S. generic pricing pressure), high debt and interest costs, and R&D spend that’s not yielding (e.g., repeated ANDA rejections or FDA import alerts – essentially products stuck in limbo). That will reflect in poor ROCE (single digits) and perhaps a P/E in the single digits too – a sign investors are skeptical.

Benchmarks:What’s good? Net NPA concept doesn’t exist here (that’s banks), but perhaps growth: high-single-digit revenue growth is decent for big pharma, double-digits is great. One interesting ratio:ANDAs approvals or new launches per year – not a financial ratio, but if a company consistently launches, say, 10-15 new products a year in the U.S., it’s refilling its arsenal. On the other hand, watch for Working Capital ratios – pharma companies can tie a lot in inventory/receivables. If you see receivable days shooting up, it might be because they pushed sales to distributors (not a great sign).

Tip: Always watch news of U.S. FDA inspections for export-oriented firms – a plant clearance can boost prospects (not directly a ratio, but your friend should know qualitative stuff too!). And remember, one successful drug can transform a company (just as one flop can hurt), so diversification of product portfolio is like not putting all eggs in one petri dish.

Metals & Mining ⛏️🥇

This sector includes steel companies, aluminum, other metals, plus mining outfits (like Coal India, NMDC). They are cyclical commodities – when economy booms or China’s hungry, they thrive; in downturns, they suffer. Important ratios focus on leverage and cost efficiency, because you can’t control the selling price (set by global markets):

Debt-to-Equity Ratio: Metals require heavy capital for mines, smelters, blast furnaces – often funded by debt. In good times, high debt seems fine; in bad times, it’s a millstone. So a conservative balance sheet is key for survival through cycles. Generally, a D/E < 1.0 is preferable. Many prudent metal companies try to de-leverage in boom times. For instance, Tata Steel after 2021’s steel boom paid down a lot of debt. If D/E is >2, that company is likely high risk, especially if prices fall. We saw cases in past commodity downturns where companies with big debt went into restructuring. Remember: commodity down-cycles can be brutal – almost all metal companies in India made losses in the 2015-16 downturn, so too much debt in such phases is ruinous.

Operating Cost per Unit (or Operating Margin): The winners in metals are usually the lowest-cost producers. If you produce steel at $300/ton and your competitor at $350/ton, when prices fall to $320, you survive and they bleed. While you might not find “cost per ton” on financials easily, you can gauge by EBITDA margin. During peaks, steel companies’ EBITDA margins could be 25–30%. During slumps, margins shrink to single digits or even negative. Keep an eye on operating margin as a proxy for cost competitiveness. Also, companies often report metrics like “cost of production” in investor presentations. A consistently higher margin than peers in the same market means either superior efficiency or integration (like captive raw materials). For example, NMDC being a low-cost iron ore miner maintained profits even when ore prices fell sharply, due to its low cost of extraction.

Price-to-Book Ratio (P/B) and Cyclically Adjusted P/E: Traditional P/E can be misleading here because earnings swing wildly. Many analysts look at P/B. In downturns, metal stocks might trade below book value (P/B < 1) – partly because book value might get written down if assets are impaired. In booms, they trade above book. If a metal stock is at a low P/B like 0.5, it could be value if it survives till the next up-cycle – or a value trap if bankruptcy looms. So combine P/B view with debt assessment (a low P/B + high debt = beware). Another approach: look at average earnings over a cycle (say 5-year avg) and apply a multiple. This smooths out the feast-and-famine nature. Not exactly a ratio, but a method to avoid being overly optimistic in booms or pessimistic in busts.

Why they matter: Metals are highly sensitive to global conditions – prices can halve or double in a span of a year. So the companies need to be financially prepared. Debt/Eq tells you who can ride out storms. Cost per unit (or margin) tells you who stays profitable longest as prices drop. A company with an EBITDA margin of 5% at cycle peak might go into losses at slight price declines – thin ice! Whereas one with 30% margin has buffer.

Good vs Bad: In good times (say when steel prices are record high, like in 2021), even weaker companies show fat profits and low P/Es (some traded at 3-5x earnings). Don’t be fooled – that’s usually top of cycle. Instead, check if they used that time to reduce debt and interest burden. A good sign is when you see debt/equity dropping and interest coverage rising during boom. That increases odds of surviving the bust. Bad sign: if a company, flush with boom profits, splurges on ambitious expansion or dividends but keeps high debt – when downturn comes, trouble.

A healthy metal/mining company might have D/E < 1, interest coverage > 5x in mid-cycle, and be among lowest cost quartile globally. For instance, Hindalco after acquiring Novelis had high debt, but managed it well when aluminum cycle turned, by improving efficiency. Struggling ones might show D/E 2+, interest coverage barely 1–2x (meaning most of operating profit goes to interest – unsustainable in any downturn).

One more quick metric: Inventory turnover. Some metal companies accumulate inventory if they overproduce during weak demand (because it’s hard to shut blast furnaces). If inventory days spike, it means they are unable to sell at current prices – a bad omen. Ideally, inventory should move fast when demand is good. In summary, balance sheet strength and cost efficiency are your north stars in metals. Value investors sometimes buy these in gloom times (low P/B) and sell in boom, but that’s a strategy requiring steel nerves (pun intended) and careful timing. As a beginner, maybe stick to diversified or relatively stable players (or consider metal ETFs to play the cycle).

And keep in mind the saying: “In a commodity business, the last man standing wins.” The ratios above help you identify who’s likely to be that last man standing when the music stops.

Oil & Gas (Energy) ⛽🛢️

Oil & Gas in India includes upstream companies (like ONGC, Oil India – who extract oil/gas), downstream refiners/marketers (IOC, BPCL, Reliance – refining crude into petrol, diesel, etc.), and gas utilities (GAIL, etc.). It’s a mix of government influence (fuel price controls at times) and global commodity swings. Key metrics:

Gross Refining Margin (GRM) [for refiners]: This is the crack spread – basically profit per barrel of crude refined. It’s measured in $ per barrel. For example, a GRM of $10 means for each barrel of crude, the refinery’s output (petrol, diesel, etc.) sold at prices $10 higher than the crude cost. Higher GRM = more profit. GRMs for Indian refiners vary: in good times, double-digit $/bbl (like $9–12) is great; in weak conditions, it can be low single digits or even negative (if product prices crash). Refiners like IOCL or Reliance report GRM every quarter. It’s their equivalent of gross margin. A high GRM quarter can supercharge profit – e.g., when diesel/ATF prices shot up in 2022, refiners made record profits. Watch out: PSU refiners sometimes had negative margins when they sold fuel below cost (price control era). A consistent healthy GRM (and how it compares to the Singapore benchmark GRM) shows competitive strength. Reliance, for instance, often posts GRMs a few dollars above the benchmark, indicating its complex refineries are more efficient.

Debt Levels (Debt/Equity or Net Debt/EBITDA): Energy projects are capital-intensive (drilling rigs, refineries, pipelines). Many oil companies carry significant debt. The safer ones manage debt in proportion to cash flows. A debt-to-equity ratio below 1 is generally comfortable in this sector. We can quote some: BPCL ~0.6, IOC ~0.9 D/E[32], which is okay, but HPCL was ~1.2[33] (more leveraged). ONGC being upstream had very low D/E ~0.1. Also use Net Debt/EBITDA: if it’s say 1-2x, that’s fine; if >3x, a bit risky if cycle turns. For example, global norm for integrated oil is to keep net debt/EBITDA < 2 in mid-cycle. High debt in a down oil price scenario can force companies to cut investment or, in worst cases, default. So check interest coverage too. Many PSU oil companies have decent interest cover, but if you see that dropping (due to controlled prices or subsidy burden), caution.

Dividend Yield: Oil & gas PSUs in India are known for rich dividends (the government likes the cash!). For investors, dividend yield is a tangible return. IOC, ONGC, BPCL often sport dividend yields of 5–7% or more. In fact, IOC at one point had ~9% yield – mouth-watering if sustainable. Of course, these dividends can fluctuate with profits (ONGC’s dividend depends on oil prices, etc.). But generally, they pay out a good chunk. A high yield can be a comfort that you get paid to wait, but ensure it’s covered by earnings (payout ratio not consistently >100%). If oil prices slump and earnings dip, expect dividends to trim. Private companies like Reliance give much smaller yields (they reinvest more). So yield is a factor mainly for PSU energy companies and a key reason many people hold them. It’s like these companies are the “fixed deposits” of the stock world – with yields often beating FDs (though with stock price risk).

Why they matter: GRM directly drives profitability for refiners – one extra dollar on GRM can mean thousands of crores in annual profit for big refiners. Debt is particularly critical because the sector’s fortunes swing with oil/gas prices and government policy. A company with low debt can survive longer through low price environments and also invest when others can’t. Dividend yield matters because energy is cyclical and somewhat low-growth domestically (except gas usage rising), so a chunk of return comes from dividends. It also signals management/shareholder (government) stance – high regular dividends mean minority investors share the wealth, not just the majority owner.

Good vs Bad:Good scenario: A company like ONGC – traditionally debt-free or low debt, decent operating margins, and when