Kesoram Industries Limited Q3 FY26 – ₹6.02 Cr PAT after years of chaos, ₹5,765 Cr ‘Other Income’ plot twist, Debt down to ₹199 Cr: Resurrection or Accounting Black Magic?

1. At a Glance – Blink and You’ll Miss the Plot

Kesoram Industries is that legendary Bollywood side character who disappears for 15 years and suddenly shows up with a glow-up, a mysterious inheritance, and rumours swirling in the mohalla. As of January 16, 2026, the market cap stands at ₹324 crore with the stock chilling at ₹10.4, up nearly 98% in just three months. Yes, you read that right. This is the same company that spent years bleeding cash, scaring lenders, and testing investor patience like a delayed Indian Railways train.

The latest quarter (Dec 2025) delivered a reported PAT of ₹6.02 crore on sales of ₹64.79 crore. Operating margins are still negative (because habits die hard), but net profit turned positive thanks to the mother of all “Other Income” entries. Debt has collapsed to ₹199 crore from a multi-thousand-crore nightmare, book value is ₹11.1, and the stock trades at ~0.94x P/B. ROCE is still negative, ROE is mathematically absurd, and P/E looks meaningless unless you understand the demerger gymnastics. Curious already? Good. Because this story has more twists than a daily soap at 9 PM.

2. Introduction – A Birla, But Not the Easy Kind

Kesoram Industries belongs to the B. K. Birla group, which immediately gives it pedigree, legacy, and the emotional weight of “yeh toh Birla hai.” But pedigree doesn’t pay interest, and legacy doesn’t service debt. For most of the last decade, Kesoram was the cautionary tale told to fresh MBA grads: “Strong brand, weak balance sheet, proceed at your own risk.”

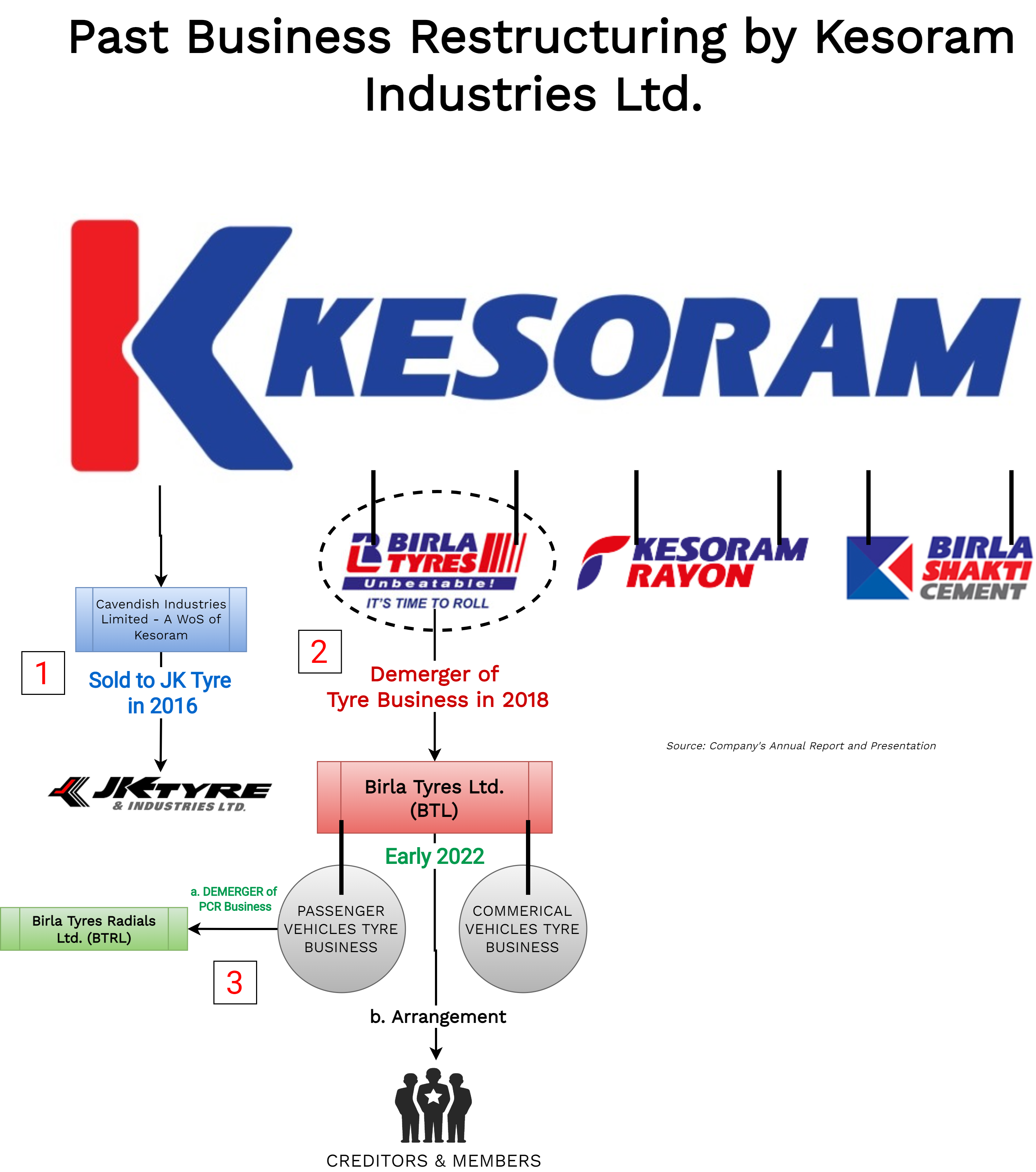

The company historically operated across cement, rayon, and chemicals, with cement doing the heavy lifting. Unfortunately, it was also doing the heavy borrowing. High-cost debt, weak cement cycles, and operational inefficiencies turned the company into a balance-sheet horror show. Equity got diluted, reserves went negative, and investors learned the true meaning of patience.

Then came the nuclear button: demerger of the cement business into UltraTech Cement. This wasn’t just strategic; it was existential. Post demerger, Kesoram is no longer the bulky cement behemoth with crushing leverage. It’s a much leaner entity, largely focused on rayon and chemicals, with debt dramatically reduced and financial statements that finally breathe.

So, is this a turnaround? Or just a one-time accounting miracle dressed up as revival? Let’s put on our funny-detective hat and dig.

3. Business Model – WTF Do They Even Do Now?

Earlier, explaining Kesoram’s business was easy: “cement plus rayon, both stressed, both capital-intensive.” Now it’s more nuanced, and frankly, more confusing for casual observers.

Cement (Demerged, Gone, Tata Bye-Bye)

Cement used to contribute 94% of revenue in FY24. Brands like Birla Shakti Cement and Birla Shakti ConQUerete had decent recall in southern and western India. Manufacturing capacity was 10.75 million tonnes across Karnataka and Andhra Pradesh, with a packing unit in Maharashtra. Sounds solid, right? Except it was drowning in debt.

The board finally said “enough” and demerged the cement business into UltraTech Cement. Shareholders received 1 UltraTech share for every 52 Kesoram shares held. This single move nuked leverage, cleaned the balance sheet, and fundamentally altered Kesoram’s future.

Rayon & Chemicals – The New Avatar

Post demerger, Kesoram is primarily a rayon and chemicals company operating under “Kesoram Rayon” in West Bengal. Capacities include 6,830 MTPA of rayon yarn and 3,600 MTPA of transparent paper (Kesophane). Products are exported to a bizarrely diverse set of countries—from Algeria and Greece to the USA and Thailand.

Rayon is not sexy. It doesn’t trend on Twitter. But it has niche demand, export optionality, and if managed well, steady cash flows. The company’s future now hinges on whether it can run this business like a disciplined manufacturer instead of a debt-fuelled empire builder.

Would you trust a reformed sinner with your capital? Or do you want proof of sustained good behaviour

One Response

situation after frontier acquisition.. please guide