🟢 At a Glance:

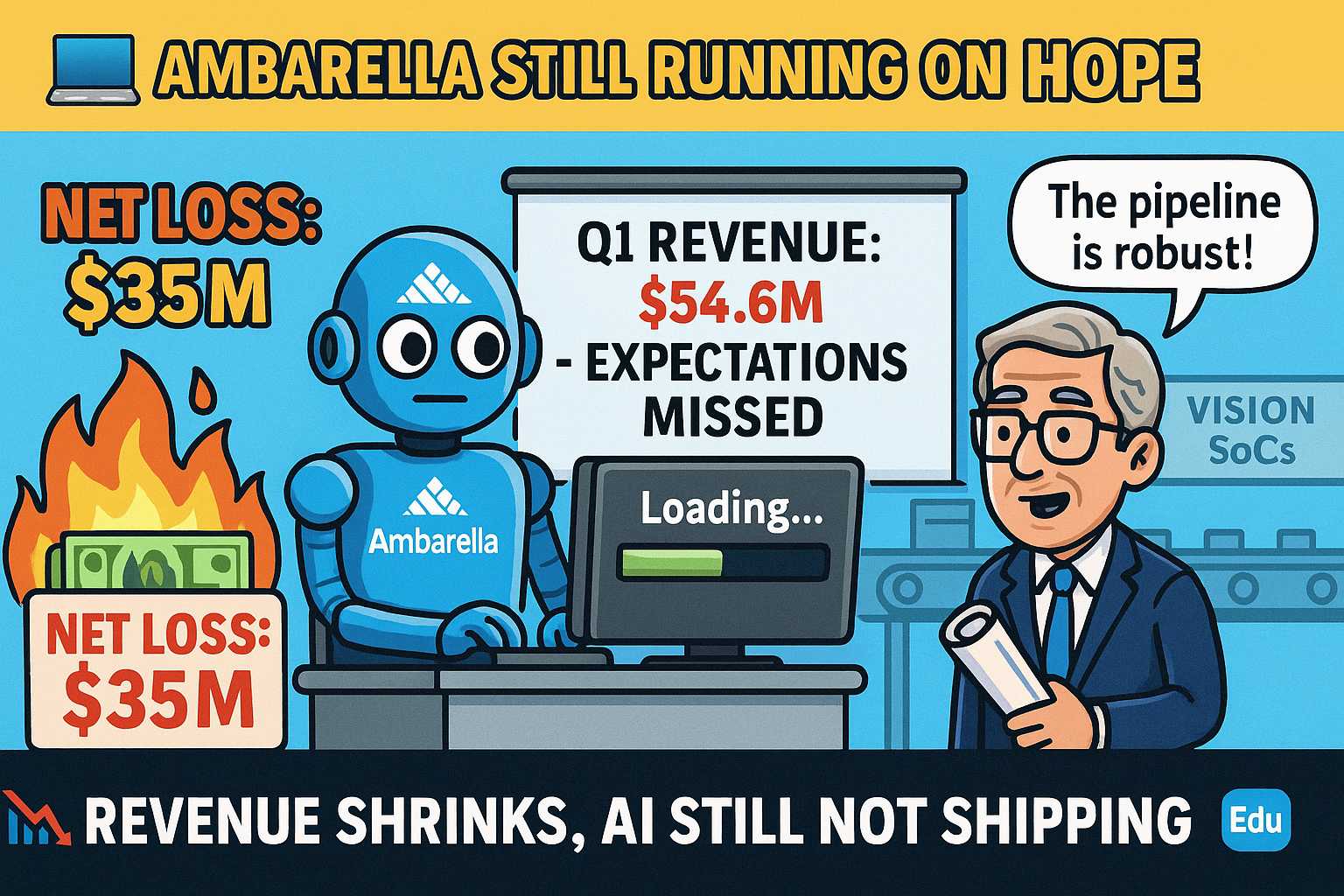

- 💰 Revenue: $54.6 million

- 🧨 Net Loss: $(35.2) million

- 💸 EPS: $(0.85) per share (Non-GAAP: $(0.46))

- 🏭 Gross Margin (GAAP): 60.6%

- 🔮 Q2 Revenue Guidance: $54–$58 million (flat as last week’s soda)

TL;DR: They burned cash, missed analyst revenue expectations, and still talked about AI like it’s saving them next quarter.

📉 Financial Breakdown

| Metric | Q1 FY25 | Q1 FY24 | YoY Change |

|---|

| Revenue | $54.6M | $62.1M | ▼ 12% |

| GAAP Net Loss | $(35.2)M | $(35.3)M | ≈ Flat |

| Non-GAAP Net Loss | $(18.9)M | $(22.3)M | 🟢 Improved |

| GAAP EPS | $(0.85) | $(0.90) | Slightly Better |

| Gross Margin | 60.6% | 62.0% | ▼ |

🔍 What Went Wrong?

- Revenue fell short of the Street’s expectations. Again.

- Still deeply loss-making — bleeding ~$35M on ~$55M sales. That’s a 🔥 burn rate.

- Automotive SoC revenue slowed due to macro weakness and slower CV deployments.

- Inventory remains high as they clear older parts.

🤖 But AI, Right?

Ambarella wants you to believe they are not just another fabless semi story.

“We continue to believe Ambarella is