LIC Policy Maturity in 2025: What Your Dad Is Secretly Waiting For

🟢 At a Glance:

Millions of LIC endowment policies bought in the early 2000s are maturing in 2025. And every Indian dad who once said “Stock market is gambling” is now refreshing his SMS inbox for that one magic payout. But is it really the jackpot they were promised?

📜 The Great LIC Dream: A Flashback

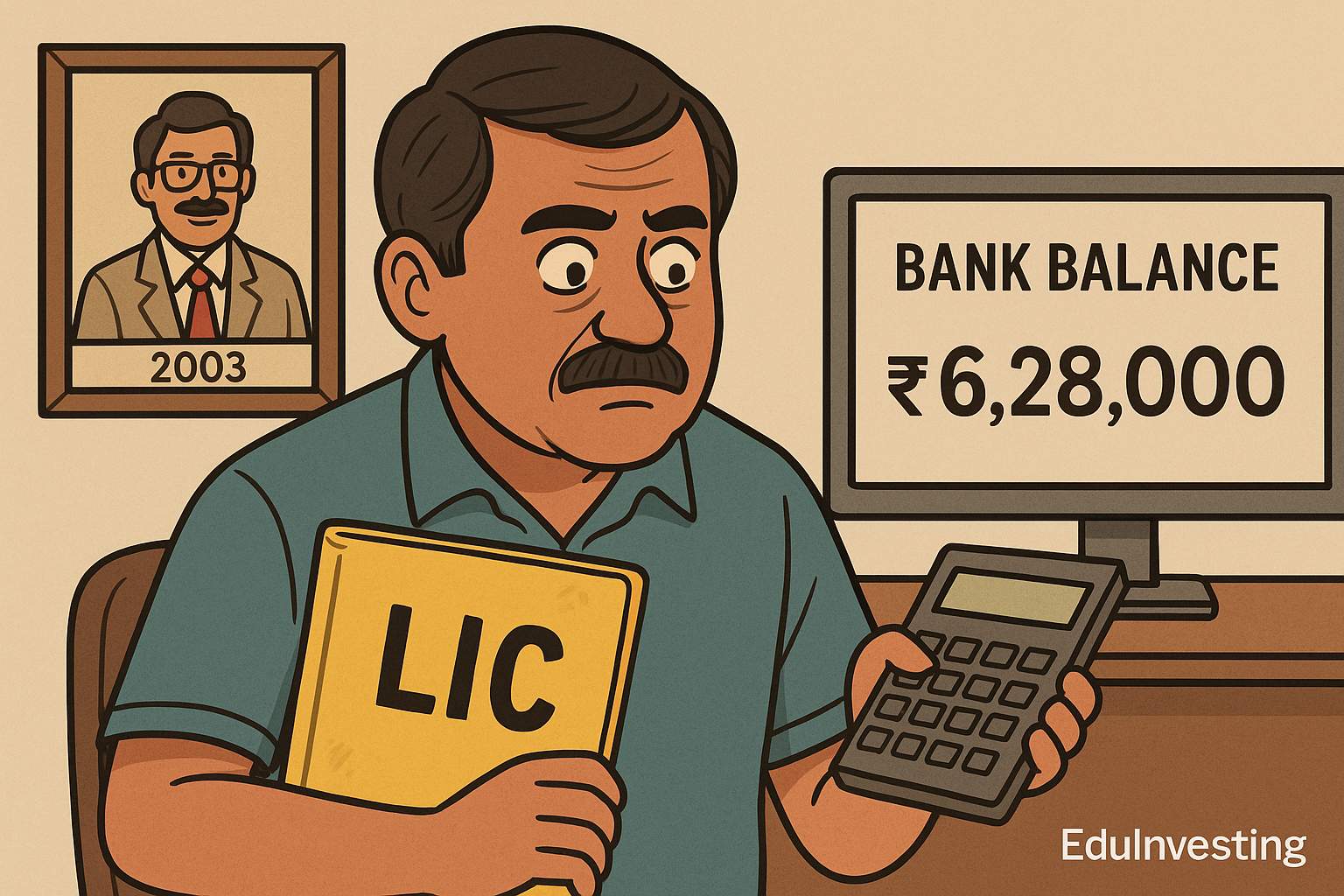

Remember when the LIC agent came home in the early 2000s?

He had a calculator, a smile, and a plan that made your dad believe he’d be a crorepati by 2025.

The plan? Pay Rs. 5,000 quarterly for 20 years, and get Rs. 10 lakh on maturity.

The reality? Your dad paid Rs. 4 lakh in premiums and might receive just Rs. 6.2 lakh after 20 years.

Because:

It wasn’t an investment. It was a “savings with life cover” — the most boring product ever made to look exciting.