When 2023 ended, the SME IPO market in India looked like a gold rush. Every other week, a new “game-changing” small-cap company hit the bourses with a big story, glossy brochure, and promoters smiling like they’d already rung the bell at the unicorn club. Two years later, half of that batch is gasping for breath, and the other half is quietly praying not to be noticed.

[nifty_ticker]

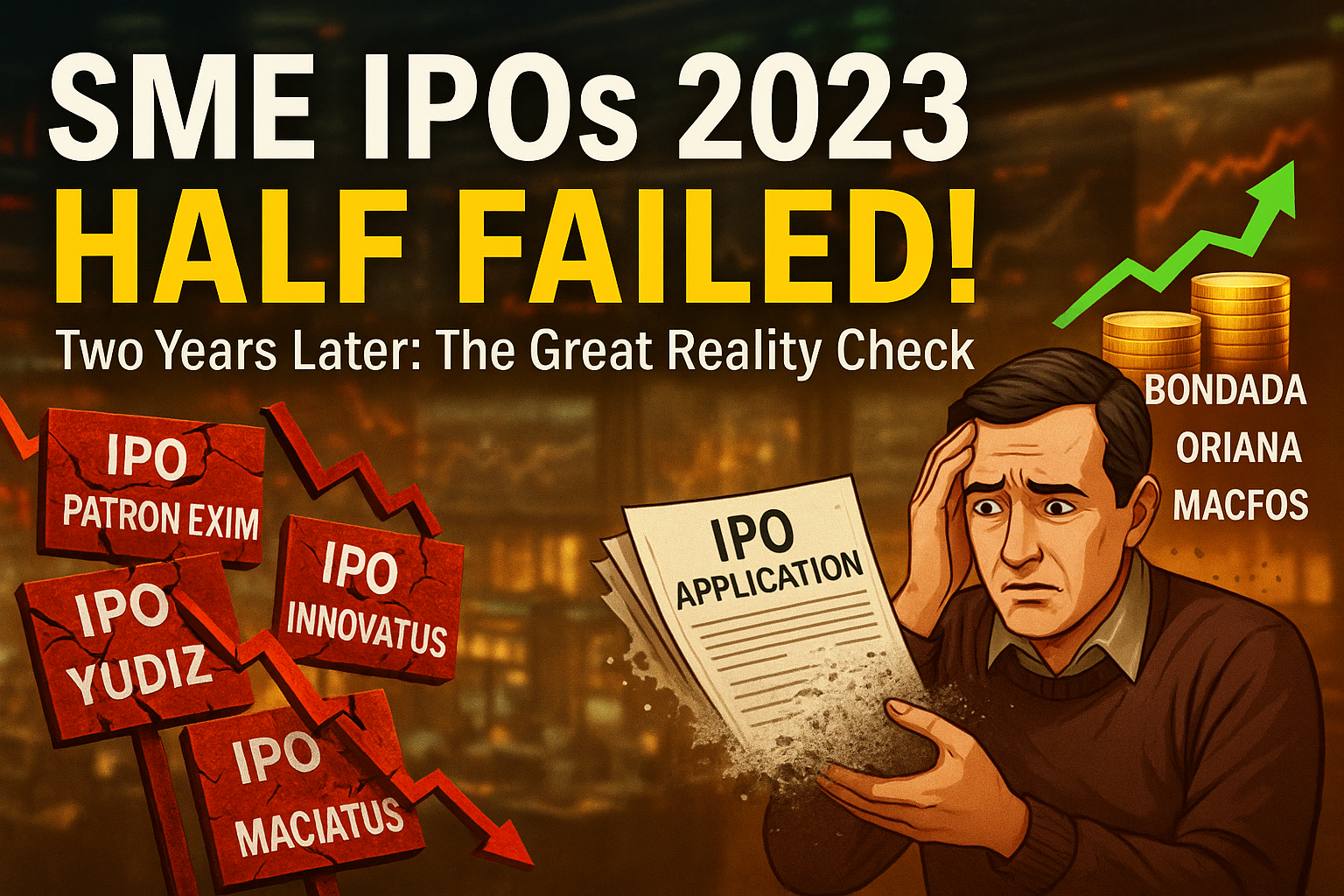

In calendar year 2023, 178 SME IPOs listed across India’s exchanges. Two years down the line, about 88 stocks trade below their listing price, and 60 have crashed below their IPO issue price. Out of those, 41 are down more than 30% from IPO price — a portfolio that can only be described as a bloodbath disguised as opportunity.

That’s not normal business risk. That’s mass design failure. And if you ask market veterans, many of these weren’t victims of bad luck — they were born sick, marketed healthy, and dumped on retail investors like overripe fruit.

How to Build a Scam in 10 Easy Steps

It’s become a predictable playbook. Take a struggling local business — a small textile exporter, an IT reseller, a niche logistics operator. Wrap it in digital buzzwords: “AI-driven”, “next-gen”, “cloud-enabled”. File for an SME IPO with a few crores in “working capital requirements” and “general corporate purposes”. Price it attractively enough to fill the issue. Pocket the IPO funds. Offload promoter stake. Disappear.

If that sounds cynical, take a look at the scoreboard.

Patron Exim fell 85%. The promoters not only pocketed the IPO proceeds but dumped 51% of their stake — down from 71% to 20%. That’s not entrepreneurship; that’s a speedrun in liquidity extraction.

Cellpoint dropped 82%. A razor-thin-margin phone retailer with no moat — exactly the kind of business that thrives only until the next iPhone launch.

Yudiz Solutions, Micropro, and Tridhya Tech — all small IT firms — proved that “software as a service” often means “service to promoters.” Each is down 60–80%.

Graphis Ads, Innovatus Digital, and Electro Force take it further: IPOs where the business never really existed beyond the pitch deck. Innovatus even had its office locked, trading suspended, and the smell of “IPO fund diversion” written all over its filings.

By the time the music stopped, several promoters had reduced their stake dramatically, others vanished into the mist, and a few were last seen explaining to auditors that “fund utilization” was a matter of interpretation.

The Sickness Was Pre-Existing

This isn’t a case of good companies gone bad. It’s a parade of dying businesses resurrected temporarily by IPO enthusiasm. Many were bleeding long before listing — low margins, poor cash flow, irrelevant products, or no market differentiation. The IPO merely extended their hospital stay.

Take Sahaj Fashions, Aatma Hospitals, or Swasthik Plascon. These firms raised crores, promised growth, and delivered nothing. Aatma, a hospital, never recovered; the company