A 1960-born Taparia Group company that makes magnetic assemblies, shunts, cores, and current-sensing products for industries from EVs to defense. Market cap ₹944 Cr, sales ₹198 Cr, PAT ₹17 Cr, margins decent at 15%. But stock trades at 56x earnings — clearly, markets think these magnets have supernatural powers.

2. Introduction

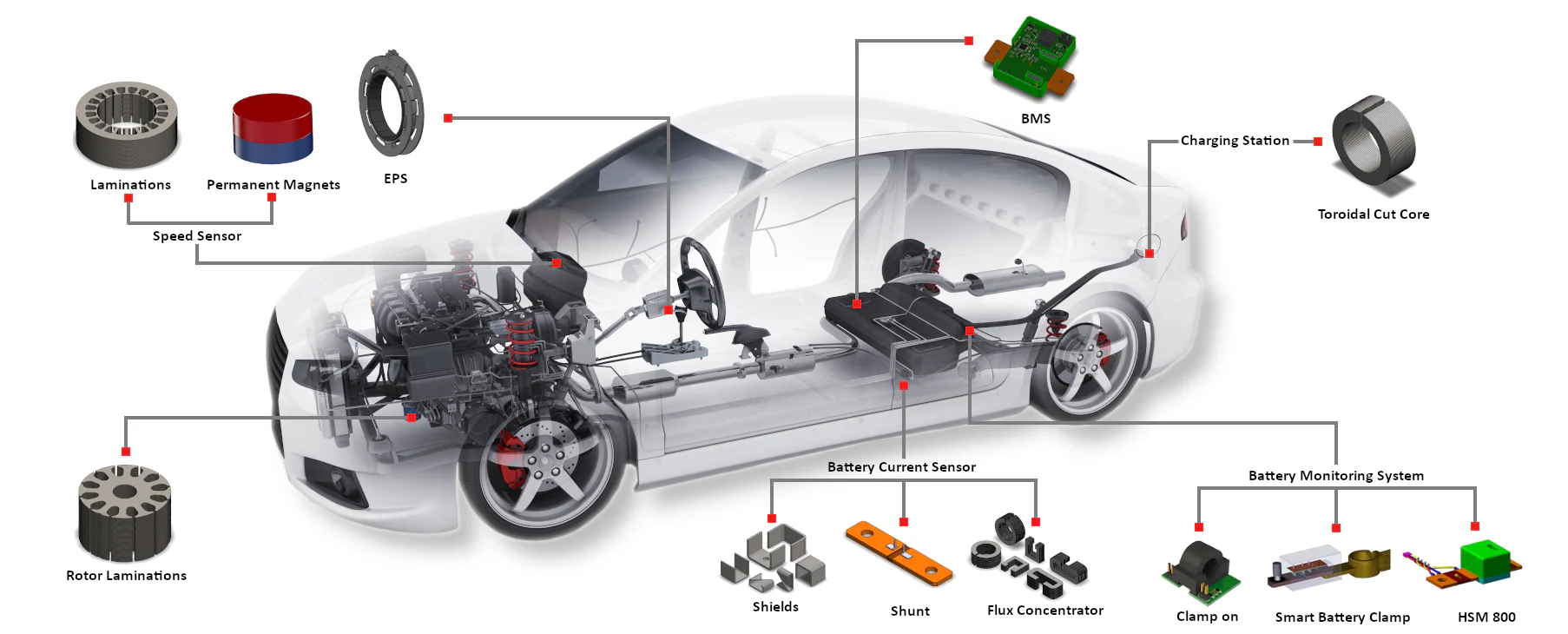

Permanent Magnets Ltd (PML) isn’t your neighbourhood “magnet-on-the-fridge” story. It’s a serious niche engineering company — making custom electrical/magnetic components for industries like power meters, EVs, telecom, defense, even ISRO-level space research. If a current needs to be sensed, a field needs to be shielded, or iron filings need to be pulled out — PML is somewhere in the supply chain.

But here’s the twist: despite the fancy end-user industries (EVs, space, defense), the company is still tiny — ₹200 Cr sales. That’s like claiming to be the backbone of India’s EV revolution while having the turnover of a mid-sized steel re-roller. Investors, though, are treating it like Tesla’s cousin — stock is up 45% in 6 months.

3. Business Model (WTF Do They Even Do?)

PML runs 3 factories in Mira Road, Mumbai, producing 350+ SKUs. Their business divisions:

Magnetic Assemblies: Separators, filters, lifters — pulling iron out of places where it shouldn’t be.

Shunts & Brass Terminals: Core product — precision parts for current measurement in meters, inverters, and EV batteries. Basically, every “smart” device needs a dumb but precise shunt.

Magnetic Cores & Shields: Using exotic metals like Mu-Metal to block magnetic interference — used in defense/aerospace.

Magnets for Meters: Old-school but still relevant — Alnico cast magnets, assemblies.

Revenue mix (FY23): 77% Engineering & Current Sensing, 13% Cast Magnets, rest from sundry ops/other income. Geography: Asia 60%, Europe 24%, Americas 15%.

So, business is diversified but still highly concentrated: top 5 clients = 44% sales. If one customer sneezes, PML catches pneumonia.

4. Financials Overview

Q1 FY26 (₹ Cr)

Metric

Jun’25

YoY (Jun’24)

QoQ (Mar’25)

YoY %

QoQ %

Revenue

53.2

54.3

45.3

-2.1%

+17%

EBITDA

11.1

8.7

5.3

+28%

+110%

PAT

7.3

5.8

2.6

+26%

+177%

EPS (₹)

8.5

6.7

3.1

+27%

+174%

Commentary: Strong recovery QoQ, margins back to 20%. But growth YoY is flat — meaning it’s a cyclical/order-driven business, not a smooth FMCG-like compounding machine.

5. Valuation (Fair Value RANGE only)

P/E Method: EPS FY25 = ₹19.4. CMP ₹1,098 → P/E = 56.5x. Industry ~40x. FV at 30–40x