1. At a Glance

Cryogenic OGS Ltd (COGSL) isn’t into “chilling” despite the name — it makes serious industrial skids, filters, dosing systems, and metering kits that keep oil, gas, and chemical plants from blowing up or leaking your future dividends. Founded in 1997, it took 28 years to finally list on the BSE SME (July 2025 IPO). FY25 sales clocked ₹32.9 Cr, profits ₹6.1 Cr, with eye-watering ROCE at 32% and ROE at 23.5%. Clean balance sheet (zero debt), fat margins (24% OPM), and Gujarat-heavy sales (47% of revenue). For once, here’s a SME that looks more like a disciplined engineer than a Bollywood scam plot.

2. Introduction

Imagine a factory in Vadodara where instead of making Farsan, they fabricate pressure reduction skids and chemical dosing panels. Cryogenic OGS isn’t the kind of company you explain to your mother over chai. But if you tell her, “Beta, ye woh log hain jo petrol, gas aur chemicals ko pipe mein theek se daal dete hain,” she’ll nod approvingly.

The business is boring (filtration, metering, pressure reduction) — but boring is good when your clients are oil & gas giants who don’t want surprises in their pipelines. Their clientele includes domestic majors via tenders, and they’ve even tied up with KMC Oil & Gas (Abu Dhabi) to sniff around GCC contracts.

The IPO story is spicy — promoters still own 73.5%, FIIs 3.3%, DIIs 9.2%, and public only 14%. This isn’t your overhyped SME circus with promoters cashing out. Margins are fat, debt is zero, auditors haven’t fled (yet), and order book comes via tenders + direct client requests.

So, is this a hidden SME gem or just another “one-customer wonder” (remember, top 5 clients = 70% sales)? Let’s go deeper.

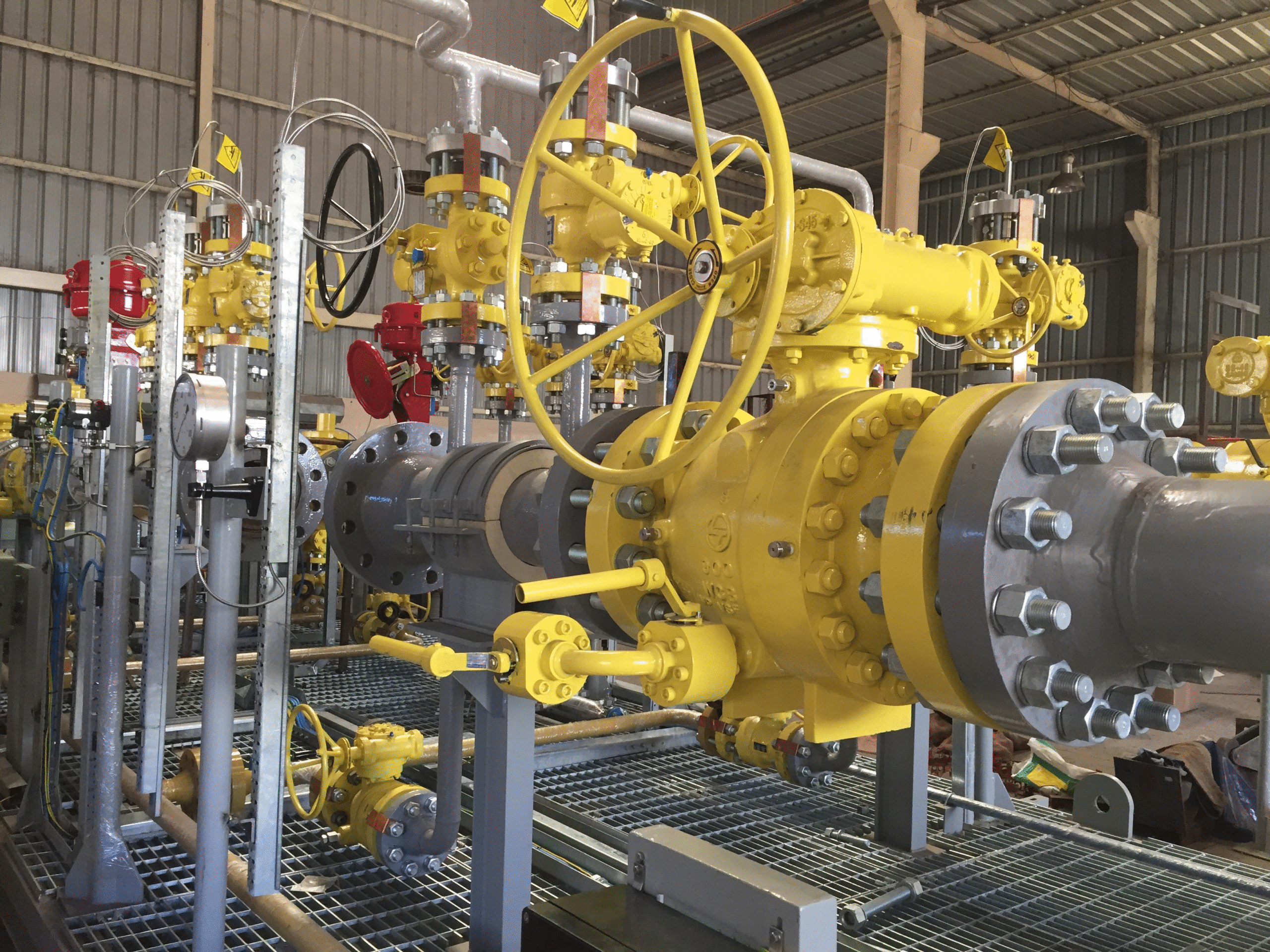

3. Business Model (WTF Do They Even Do?)

Cryogenic OGS builds industrial skids and equipment — not the gym type, but the ones that sit quietly in oil/gas terminals, ensuring flow, blending, and metering don’t go wrong.

- Products: chemical dosing skids, additive injection panels, basket strainers, gas metering skids, vapour eliminators, truck loading skids.

- Industries: Oil & gas, chemicals, fluid handling.

- Clients: Primarily PSU oil majors + petrochemical firms (via tenders).

- Geography: 99% India, with GCC as the new growth frontier.

- Process: Tenders (93 submitted in FY24 for